Rolex Rings Mar 2026: The ₹101 Crore Extinguisher and the Free-Carried Public Shareholder

Section 1 — At a Glance

A clean break from historical baggage is often the ultimate catalyst for an asset-heavy manufacturer, and Rolex Rings Ltd has finally cut the cord. During the financial year ended March 31, 2026, the company posted a stable headline revenue of ₹1,143.50 crore, marginally down from ₹1,154.80 crore in the previous fiscal year. However, the true story lies beneath the top-line stagnation. Rolex Rings completely liquidated its legacy liabilities by paying a massive ₹101.00 crore to consortium lenders as a final settlement for its Right of Recompense (RoR) obligation. This effectively closes the book on its 2013 Corporate Debt Restructuring (CDR) era.

While net profit took an optical hit—falling to ₹141.10 crore due to the final unprovided ₹49.19 crore of the RoR package being dragged through the P&L as an exceptional item—the operational machine remained highly robust. Adjusted profit after tax (excluding exceptional items) stood flat at ₹192.70 crore.

Investors are heavily focused on two key developments. First, a major capital allocation shift is underway, highlighted by an announced ₹180.00 crore equity buyback where the promoter group has opted out entirely. This creates a high-conviction wealth transfer directly to public shareholders. Second, a structural geographic rebalancing is taking place. Aggressive growth in Europe (+25% YoY) has effectively neutralized a severe, tariff-induced 30% drop in US export volumes.

Worry remains centered on a massive working capital expansion. The company’s cash conversion cycle stretched to 164 days, and overall working capital days surged to 213 days. This expansion was driven by prolonged transit times and intentional inventory build-ups designed to insulate international Tier-1 clients from global shipping bottlenecks. True balance sheet strength is realized when operational cash flows can comfortably fund both capital expenditure and shareholder rewards without relying on external debt. Rolex Rings has achieved exactly that, crossing the finish line into a debt-free, cash-positive chapter.

Section 2 — Introduction

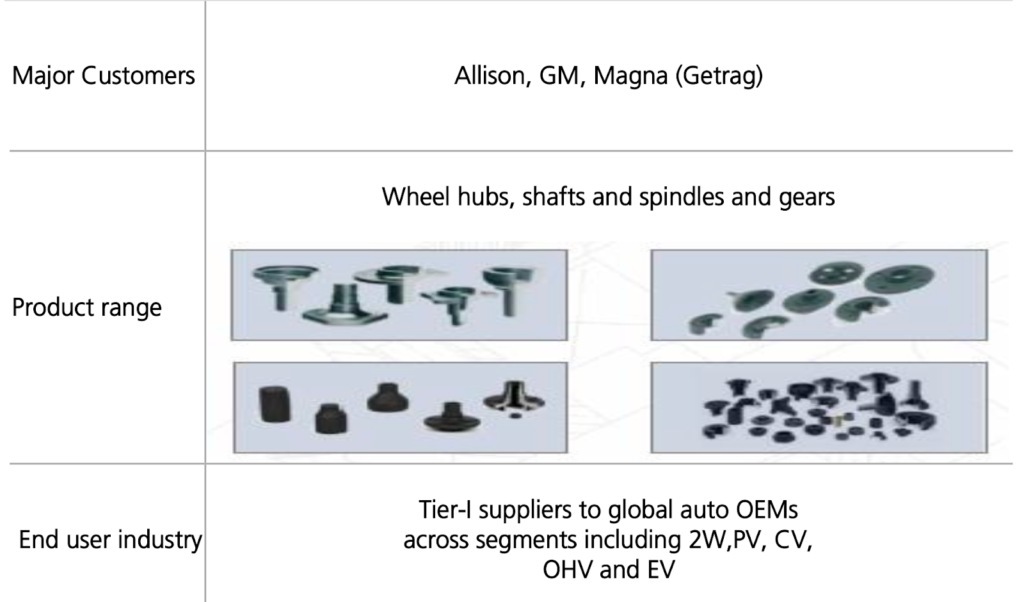

Rolex Rings Ltd, based in the manufacturing hub of Rajkot, Gujarat, has evolved from a small partnership firm established in 1980 into one of India’s top five forging powerhouses. The company operates as a critical tier-2 supplier, hot-rolling and machining high-precision bearing rings and complex automotive components for global tier-1 automotive giants and industrial heavyweights.

This deep analytical deep-dive is triggered by two defining corporate events in early 2026: the complete structural clearance of its past financial liabilities and an unprecedented capital return initiative. Having exited active corporate debt restructuring in 2022, the final settlement of the Right of Recompense in March 2026 marks the absolute financial liberation of the firm. With a clean financial slate, management immediately flipped the capital allocation switch, announcing a major ₹180.00 crore buyback at ₹180.00 per share. This structural transformation occurs at a critical juncture when global automotive supply chains are actively executing “China+1” sourcing strategies, positioning precision players like Rolex Rings directly in the crosshairs of long-term institutional interest.

Section 3 — Business Model: WTF Do They Even Do?

For the uninitiated investor, Rolex Rings does not make luxury timepieces; it pounds raw steel bars into round, highly engineered, microscopic-tolerance chunks of metal that prevent your car wheels from flying off at 120 km/h.

The company transforms engineering drawings into high-speed hot forgings and intensively machined components through three automated manufacturing facilities in Rajkot. Its product suite is cleanly split into two structural components: Bearing Rings, which account for 45% of FY26 revenue, and Automotive Components, which make up 47%. The bearing ring portfolio spans inner and outer tracks for tapered, cylindrical, and deep-groove ball bearings utilized across passenger vehicles, railway coaches, and massive wind turbines. The automotive segment produces high-value, fully machined gear blanks, ring gears, transmission parts, and wheel hubs across the entire weight spectrum from light two-wheelers to heavy commercial vehicles.

Value addition is the primary metric here. Rolex Rings is not a dumb blacksmith; approximately 85% of its total revenue is derived from fully machined components rather than raw forgings, allowing it to capture superior margins and build a defensible competitive moat with global clients like SKF, Schaeffler, and Ford.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

The quarterly and annual operational performance reveals the sheer impact of the US tariff shock and the subsequent visual distortion on the bottom line.

Quarterly and Annual Performance Trend

The locked filing frequency for Rolex Rings Ltd is QUARTERLY.

Metric

Latest Quarter (Mar 2026)

YoY % Change (vs Mar 2025)

QoQ % Change (vs Dec 2025)

Revenue from Operations

₹305.69

+7.68%

+11.22%

EBITDA / Operating Profit

₹56.24

+7.70%

-2.38%

Net Profit (PAT)

-₹0.15

-100.27%

-100.31%

Earnings Per Share (EPS)

-₹0.01

-100.50%

-100.57%

Note: The calculated quarterly EBITDA shown above excludes other income, matching raw operating metrics. Net profit and EPS dropped precipitously into negative territory exclusively due to the lump-sum unprovided RoR compensation charge booked in Q4 FY26.

The core takeaway is that raw demand remained resilient. Quarterly revenue expanded sequentially by 11.22% to ₹305.69 crore, driven by a sharp acceleration in domestic auto component orders and steady shipments to Europe. Gross margins hit an exceptional 54.7% in Q4 FY26 due to raw material pass-through clauses and a higher mix of machined automotive parts. However, other expenses surged to ₹92.30 crore during the quarter. This spike was caused by two distinct non-structural items: a ₹22.00 crore upfront US customs duty payment (of which 50% is contractually receivable from clients in subsequent quarters) and ₹6.00 crore in legal fees connected to the final lender settlement. When operational margins expand while headline net profits compress under the weight of one-time outlays, earnings quality is structurally improving beneath the surface noise.

Did Management Walk the Talk?

Reviewing the older guidance against actual delivery reveals a management team executing an agile defense. In late 2025, when the US tariff regime threw import duties up to a punishing peak of 53% for auto components under Section 232, management warned of a substantial revenue slowdown in North America.

The numbers validate this: annualized US exports fell by roughly 30%. However, management promised to protect the 20%+ EBITDA floor by shifting raw material procurement from expensive overseas steel to domestic processes and re-nominating capacity to European platforms. They delivered precisely on this posture, holding FY26 raw