Rama Phosphates Ltd Mar 2026 : Earnings Skyrocket 285% as Turnaround Locks in ₹52.71 Crore Net Profit

Section 1 — At a Glance

Rama Phosphates Ltd has closed fiscal year 2026 on an exceptionally strong note, logging an aggregate revenue from operations of ₹893.04 crore, representing a robust 20.09% expansion over the previous fiscal’s top line of ₹743.69 crore. The financial recovery is highlighted by a sharp surge in Net Profit, which jumped 285.31% to ₹52.71 crore from ₹13.68 crore in fiscal year 2025. Operating profit performance was equally impressive, with EBITDA leaping from ₹44.87 crore to ₹87.00 crore, driving operating margins back to a healthy 9.74% from a compressed 6.03% in the prior year.

This material acceleration in earnings is primarily supported by stable volume allocations, such as a major 1 lakh metric tonne Single Super Phosphate contract renewal with Hindustan Urvarak & Rasayan Limited, alongside strong market traction for newly rolled out fortified products. However, the investment community remains cautious about extreme raw material input volatility, as international sulphur prices hit historic highs during the year, accompanied by sharp currency fluctuations that tested margins. Additionally, working capital asset intensity saw a notable build-up, with trade receivables ballooning significantly towards the end of the year.

True corporate health is not measured during seasons of stable input prices, but by management’s structural ability to absorb extreme supply-chain shocks.

As the company progresses with its next phase of capital expansion at its Dhule greenfield plant, investors are watching closely to see whether its asset utilization can keep pace with its expanding infrastructure.

Section 2 — Introduction

Rama Phosphates Ltd, established in 1982, has evolved into a notable multi-state agricultural solution provider. Operating across a deeply cyclical and highly regulated fertilizer landscape, the company has rebuilt its financial foundation after historical structural adjustments.

The publication of these fiscal year 2026 earnings marks a critical pivot from localized capacity constraints to pan-India volume goals. With key operational setups running across Maharashtra, Madhya Pradesh, Rajasthan, and Karnataka, the corporate emphasis is moving towards high-margin specialty chemicals and forward-integrated crop nutrition blends. This report evaluates if the company’s asset turn can support its ambitious manufacturing footprint.

Section 3 — Business Model: WTF Do They Even Do?

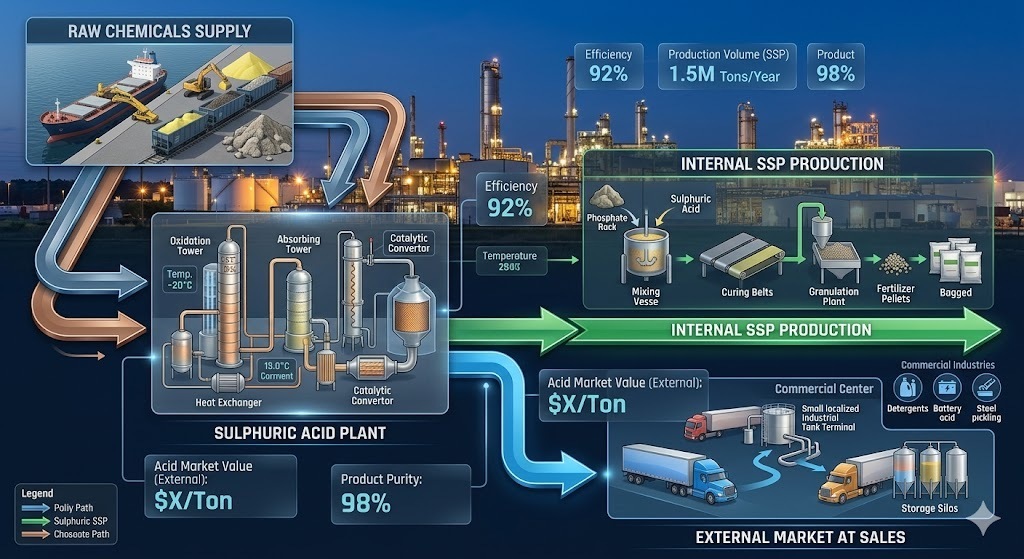

Rama Phosphates works as a hybrid player balancing agricultural nutrition and base chemicals. The primary engine is the Fertilizer vertical, generating approximately 72% of product revenues via Single Super Phosphate (SSP) in powder and granulated formats. This segment is further enhanced with fortified lines like zincated, boronated, and magnesium-treated variants under the prominent “Girnar” and “Suryaphool” brand names.

The second engine is the Chemicals division, utilizing core output blocks of Sulphuric Acid (98% concentration), Oleum, and Linear Alkyl Benzene Sulphonic Acid (LABSA)