1. At a Glance – Small Cap, Big Drama

Quest Laboratories Ltd is currently sitting at ₹121 with a market cap of ₹198 crore. In the last 3 months, the stock is up 39.1%, but over one year, it’s still down 12%. So yes, this stock has mood swings.

Now the juicy part — Q3 FY26 numbers.

Sales came in at ₹30.61 crore, up 106% YoY. PAT jumped to ₹4.03 crore, up 417% YoY. That’s not growth. That’s a protein shake.

Stock P/E stands at 14. ROE is 24.6%. ROCE is 26.9%. Debt-to-equity is just 0.36. Price-to-book is 2.20.

For an SME pharma company doing ₹126 crore TTM revenue and ₹14.1 crore PAT, these are not ugly numbers.

But here’s the twist — earnings include ₹7.25 crore of other income in TTM.

So the question is simple: Is Quest Laboratories a quietly compounding pharma story… or is it riding a one-time boost wave?

Let’s investigate like a slightly sarcastic detective.

2. Introduction – The Pharma Kid from Pithampur

Quest Laboratories was incorporated in 1998. No dramatic origin story. No Silicon Valley garage. Just good old pharmaceutical manufacturing in Pithampur, Dhar.

This is not a flashy branded pharma giant like Sun Pharma or Cipla. This is the backend workhorse — making formulations across antibiotics, anti-malarials, anti-inflammatories, respiratory meds, diabetes treatments, and more.

They produce:

- Tablets

- Syrups

- Dry syrups

- Ointments

- ORS powders

- External liquids

Over 800+ licensed formulations and 272+ active products.

They operate across OTC, ethical, generic, institutional supplies, contract manufacturing, exports, and PCD business.

Translation: They don’t want to miss any revenue bucket.

They even have a ₹25 crore order book from Myanmar.

Now pause.

An SME pharma company with export orders, new injectable plant plans, capsule section launch, collagen launch, and capex of ₹35 crore over 3 years?

Ambitious much?

Or building something real?

3. Business Model – WTF Do They Even Do?

Okay, imagine you’re a hospital, a government institution, or an export distributor in Myanmar.

You need:

- Antibiotics

- Antimalarials

- Diabetes drugs

- Respiratory meds

- ORS powders

- Generic formulations

Quest manufactures them.

Simple.

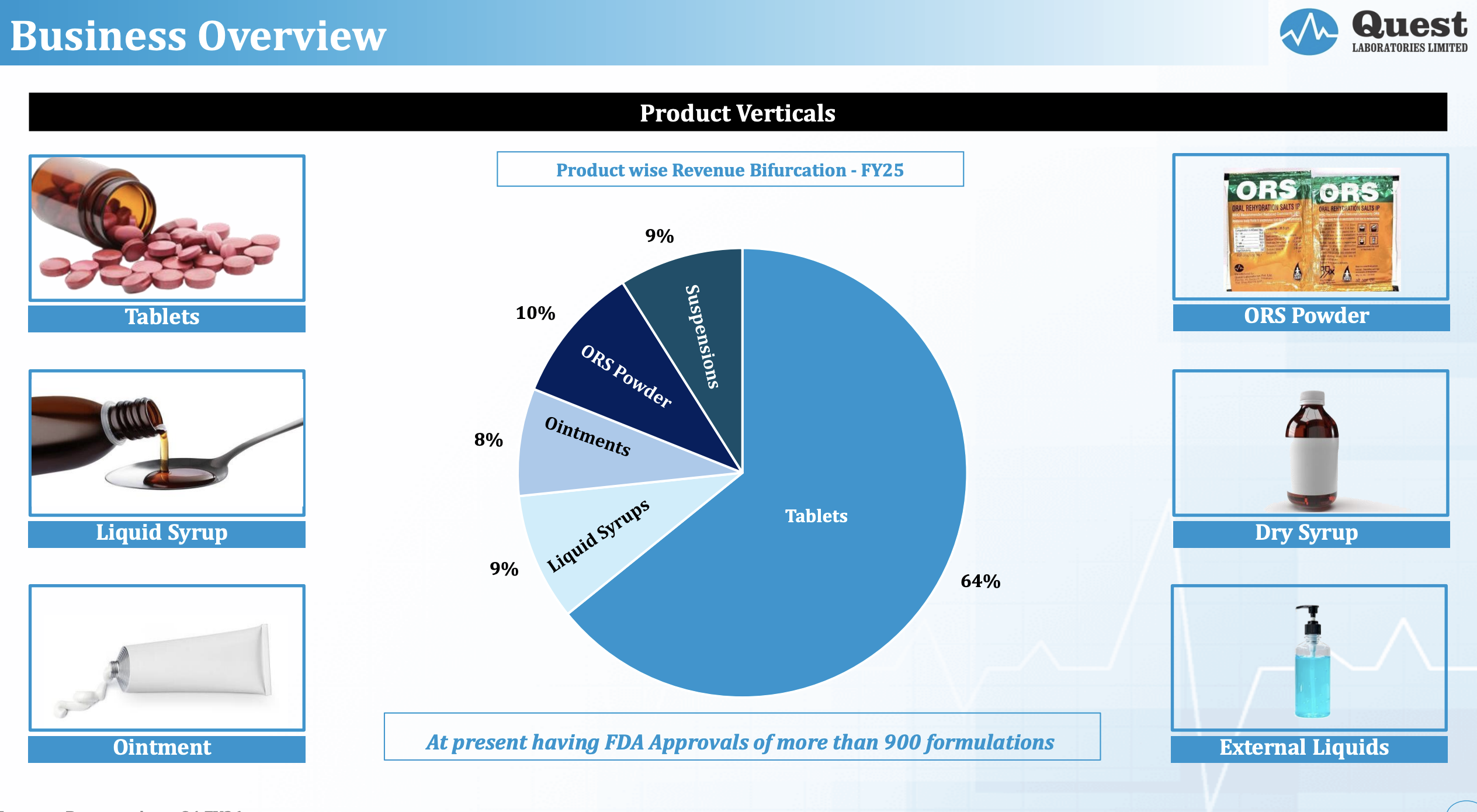

They sell 61% revenue from tablets, 19% from syrups, 10% from ORS, 8% from suspensions, and 2% from ointments (FY24 breakup).

Sectorally:

- 81% revenue from public institutions

- 19% from private enterprises

This means government tenders matter.

And if you understand Indian pharma tenders, you know two things:

- Volume is high.

- Margins are tight.

But they’re now expanding into:

- Capsules (10 lakh per day capacity, ₹10–15 crore expected annual contribution)

- Injectables (2 lakh/day capacity, ₹30 crore expected annual revenue)

- Collagen (launch April 1, 2025)

Injectables are margin-enhancing products. That’s not small news.

Current capacity is already strong:

- 9 million+ tablets per day

- 1 million+ capsules per day (upcoming full scale)

- 30,000+ dry syrups daily

- 2,000+ liters external liquids daily

So they’re not tiny in operations. Just tiny in market cap.

Now the real question:

Can they scale without losing margins?

Let’s check numbers.

4. Financials Overview – Numbers Don’t Lie (Mostly)

Quarterly Results – Figures in ₹ Crores

EPS: