01 — At a Glance

The Comeback Kid Nobody Expected to Succeed

- 52-Week High / Low₹1,955 / ₹1,235

- Q3 FY26 Revenue₹2,918 Cr

- Q3 FY26 PAT₹400 Cr

- Q3 FY26 EPS (₹)17.65

- Annualised EPS (Q3×4)₹70.60

- Book Value₹1,210

- Price to Book1.47x

- Dividend Yield0.00%

- Debt / Equity2.7x

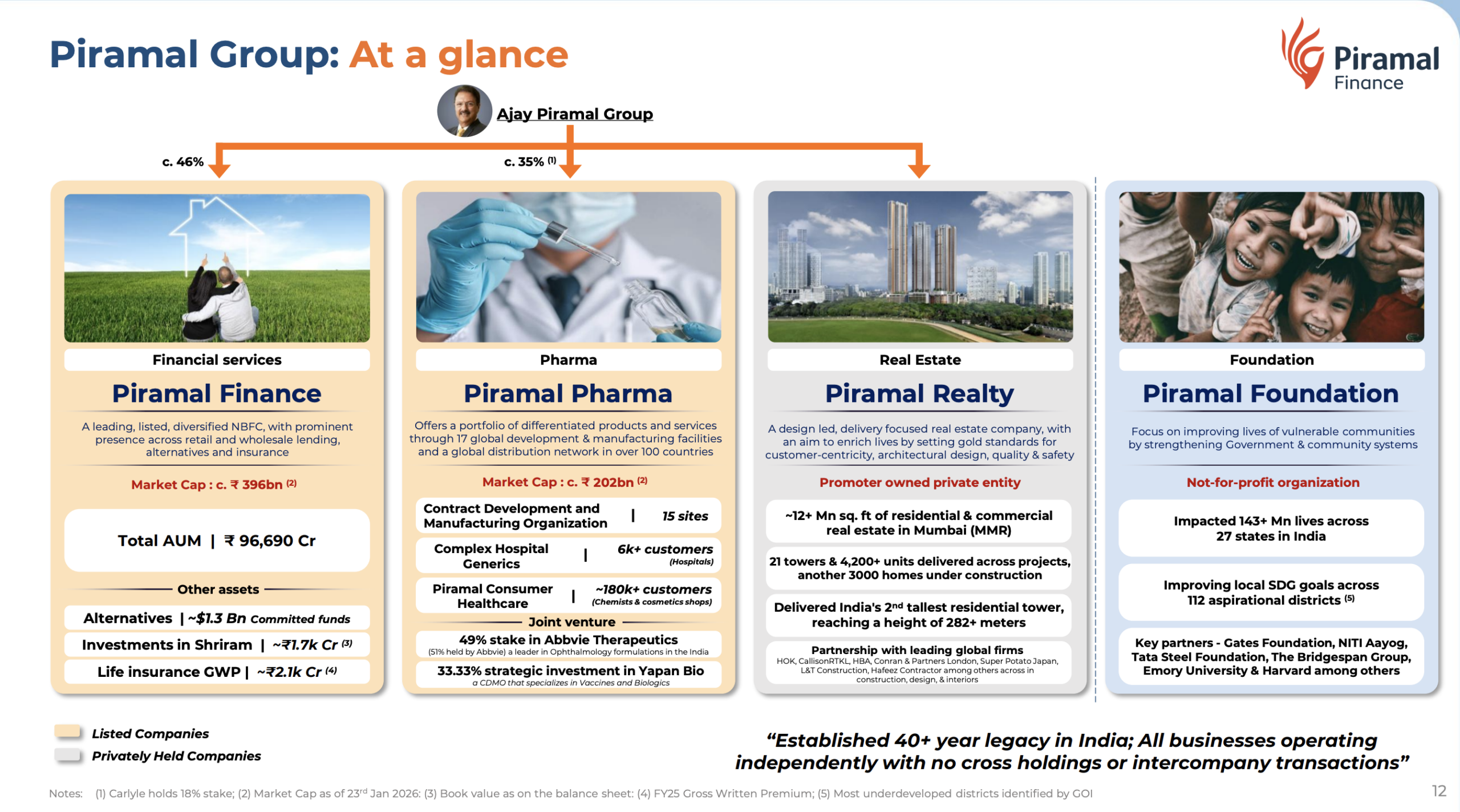

- Total AUM (Dec 2025)₹96,690 Cr

The Setup: Piramal Finance closed Q3 FY26 with ₹96,690 crore in AUM (up 23% YoY), posted consolidated PAT of ₹400 crore (vs ₹39 crore in Q3 FY25, a 940% spike), and achieved an annualised EPS of ₹70.60. The stock returned 21.7% in three months. CRISIL upgraded to AA+/Stable in January 2026. This is not a casual recovery narrative — this is a company that acquired India’s largest housing finance zombie (DHFL), butchered the legacy book with ruthless efficiency, and built a 82% retail-led franchise from the ashes. All while the street was looking elsewhere.

02 — Introduction

From DHFL’s Corpse, A New Lending Monster Emerges

Let’s set the stage: In March 2021, the Piramal Group (pharma-realty conglomerate) acquired Dewan Housing Finance Corporation (DHFL)—a ₹50,000-crore wreck that defaulted on bonds and became the first large Indian NBFC to fail spectacularly. The resolution took years. When Piramal finally took charge, the legacy book was a graveyard of bad loans, stretched real estate exposures, and a staff that didn’t believe in anything anymore.

Fast forward to Q3 FY26 (December 2025). That same company—now branded as Piramal Finance—has 518 retail branches, 5.4 million customer franchise, ₹79,413 crore in retail AUM, and is growing at 34% YoY in the growth businesses. The legacy DHFL monster (₹5,230 crore) now represents just 5% of total AUM, down from 91% in March 2022. If you haven’t noticed this transformation, you’ve been scrolling through memes instead of earnings reports.

The premise is simple: Ajay Piramal (billionaire pharma baron) saw a sinking ship, bought it at a discount, replaced every system, hired bankers from Axis, scaled retail lending at an insane pace, and is now printing profits. Debt-to-equity at 2.7x. Interest coverage at 1.17x (yes, thin). But growth is 23%+ YoY, and the business model is working. This is the NBFC story nobody expected to write in 2026.

The Trend You Missed: Six months ago, everyone was worried about NBFC leverage. Today, everyone is worried about NBFC valuations. Piramal Finance is 40% of the sector median P/E. Either it’s cheap, or it’s expensive at the wrong valuation. Let’s find out.

03 — The Business Model: Lending to India’s Missing Middle Class

Retail Mortgages Are Boring. That’s Why They Work.

Piramal Finance operates a multi-product retail lending platform disguised as a boring housing finance company. Here’s the menu: Housing loans (38.6% of AUM), loans against property LAP (29.4%), used car loans (6.4%), unsecured business loans (7.2%), salaried personal loans (8.8%), digital loans (4.7%), and microfinance (1.1%). Not exactly rocket science. Not exactly competition-proof either. But here’s the kicker—this portfolio is granular, diversified, and mostly secured.

Distribution is the moat. Piramal has 518 branches across 26 states and 429 cities, with 10,500 salespeople on the ground. Each branch in maturity does ₹7.5 crore in monthly disbursements. They’re hiring from Axis Bank’s retail playbook. Data-driven underwriting. Personal discussions (yes, that’s a feature, not a bug). AI-driven credit scoring. 240,000+ personal discussions in 9M FY26. 160,000+ property appraisals in-house. When you’re lending to India’s middle class, relationship and process matter as much as credit scores.

The sweet spot: customers earning ₹30k–₹1 lakh monthly, in Tier-2 and Tier-3 cities, where the branch network is thick and the competition is thin. 82% of customers are outside Tier-1. Median customer age: 38 years. 55% self-employed. Median monthly income: ₹49,000. This is retail lending at scale, unglossified, and profitable if you execute the underwriting like a surgeon.

Retail AUM Share82%Up from 9% in Jun 21

Housing + LAP68%Secured Legacy

Branch Count518Up from 14 in Jun 21

Retail GNPA0.8%Very Tight

Cross-Sell Magic: 25–30% of unsecured disbursements come from cross-sell (existing customers upgrading to personal loans). Cross-sell customers have 77% lower opex vs open market sourcing and 25% lower 90+ DPD. Translation: the customer acquired for a housing loan can be lent to 3–4 more times, cutting your customer acquisition cost per product to nearly zero. This is NBFC leverage in its purest form.

💬 Quick thought experiment: If Piramal can cross-sell to 50% of its 5.4 million retail franchise, that’s 2.7 million customers. At ₹1 lakh ticket size, that’s ₹27,000 crore in unsecured loan opportunity. Do you think they can reach there in 3 years?

04 — Financials: The Turnaround Narrative in Numbers

Q3 FY26: The Quarter That Changed Everything

Continue reading with a premium membership.