Pattech Fitwell Tube Components Ltd H1 FY26 – ₹35.47 Cr Sales, ₹0.88 Cr PAT, 93× P/E: When Forgings Meet Froth

1. At a Glance – The ‘High P/E, Low Chill’ Snapshot

Pattech Fitwell Tube Components Ltd is that classic SME stock which wakes up one fine morning, looks at itself in the mirror, sees ₹35.47 Cr half-year sales, ₹0.88 Cr net profit, and then confidently trades at a 93× P/E, as if it just cracked nuclear fusion instead of welding flanges. With a market cap of roughly ₹107 Cr, a current price of ₹114, and a three-month return of -1.94%, the stock is clearly undecided whether it wants to be an industrial compounder or a speculative roller coaster.

The latest Half Yearly Results (H1 FY26) show revenue growth of 45.85% YoY in the September 2025 half, but profits politely refused to cooperate, declining 8.33% YoY. Operating margins have slimmed down to 5.24%, ROCE is sitting at 9.67%, and ROE is a sleepy 6.18%. Debt stands at ₹17.36 Cr, promoter holding has dropped sharply from 69.06% to 57.01%, and yet the valuation behaves like margins are expanding, cash flows are gushing, and angels are signing supply contracts.

This is a company with real factories, real steel, and real welding sparks — but also a stock price that seems powered by imagination. Curious already? Good. Because this story has pipes, pressure, and plenty of pressure on expectations.

2. Introduction – A Smallcap Forging Its Own Reality

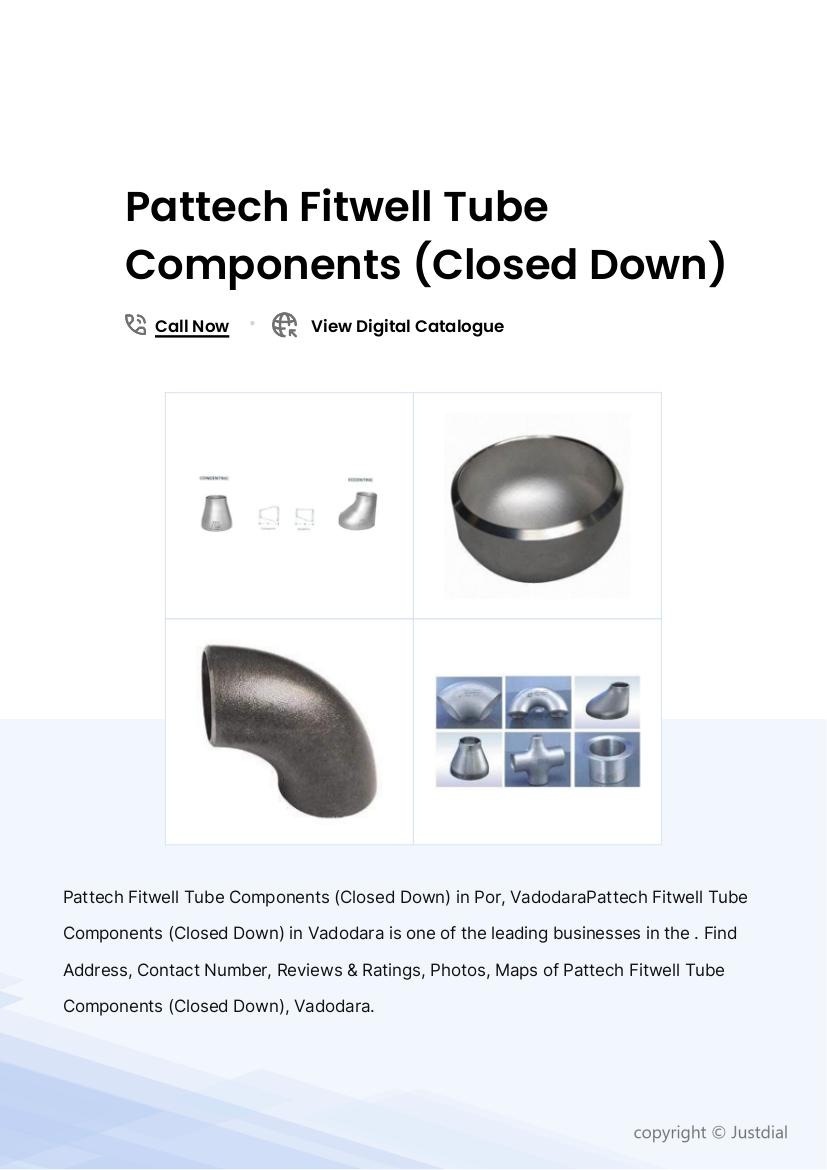

Pattech Fitwell Tube Components Ltd was incorporated in 2012, and on paper, it lives in a boring but essential corner of Indian industry: pipe fittings, flanges, forgings, machined components, and fabrication work. In reality, boring businesses are often the best — provided they make money consistently and don’t pretend to be something they’re not.

Pattech operates in sectors like fertilizers, power, chemicals, pharmaceuticals, oil & gas, desalination, water treatment, shipbuilding, defence, and food processing. Basically, if an industry moves fluids under pressure, Pattech wants to supply the elbows and flanges holding that pressure together. Glamorous? No. Necessary? Absolutely.

But here’s where things get spicy. Despite being a capital-goods-style manufacturer with single-digit margins, modest returns on capital, and negative operating cash flows in recent years, the stock trades at a valuation that would make even premium forging players blush.

Is the market betting on future scale? On operating leverage? On preferential allotment magic dust? Or is this just SME market enthusiasm doing bhangra again?

Before judging, let’s tear open the balance sheet, income statement, and cash flows like a forensic auditor with a sense of humour.

3. Business Model – WTF Do They Even Do?

Imagine a large EPC contractor building a fertilizer plant. Pipes everywhere. High pressure, high temperature, corrosive chemicals, and zero tolerance for failure. That’s where Pattech Fitwell walks in, toolbox in hand.

The company does not invent pipes. It converts semi-finished and raw products into finished industrial components through value-added processes such as forming, bending, drilling, cutting, inspection, polishing, painting, blasting, welding, punching, marking, testing, and packaging. In simple terms: they take metal pieces and make them site-ready for industrial use.

All made in Carbon Steel (CS), Alloy Steel (AS), and Stainless Steel (SS).

The manufacturing facility is located in Gujarat with a capacity of 14,104 MTPA, focused on forged flanges and specialized machined components. Revenue is almost entirely from sale of pipe and tube fittings (99%), with services contributing a negligible 1%.

So no fancy diversification, no unrelated experiments. It’s a focused industrial shopfloor business. The question is simple: can this business justify premium valuation without premium margins?

4. Financials Overview – Growth With a Margin Hangover

Result Type Lock

The latest official heading clearly states “Half Yearly Results”. ➡️ Result Type Locked: HALF-YEARLY ➡️ Annualised EPS = Latest EPS × 2