Lumax Auto Tech FY26: ₹4,870 Cr & A 65% Profit Surge Into A Crowded Multiple

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1 — At a Glance

FY26 delivered a paradox: record revenue at ₹4,870 Cr (+34% YoY) and record net profit at ₹337 Cr (+47% YoY), yet the company sits at 37.8x earnings while the peer median pays 26.8x.

The margin held steady at 14.5% EBITDA and 6.9% PAT—solid, not stellar. That said, profit growth outpaced revenue growth by 13 percentage points. A clue: M&M and Bajaj still make up 40% of revenue. Concentration risks exist. Meanwhile, the order book at ₹1,450 Cr signals 3+ years of visible work.

Mechatronics revenue jumped 146% YoY to ₹281 Cr. Greenfuel, acquired in FY26, contributed ₹383 Cr—a new leg, not a mature one.

The tension: fast growth in emerging units meets a shrinking multiple ceiling. Watch the next 18 months.

2 — Introduction

Lumax Auto Technologies, part of the DK Jain Group since 1945, has spent 25 years in the public markets. For two decades, it concentrated on automotive lamps, gear shifters, and sheet metal. The last 3–4 years redefined it.

In March 2023, Lumax acquired 75% of IAC India for ₹587 Cr—a 4W interior systems supplier. The move cut the 2W/3W revenue share from 43% in FY22 to 24% by end of FY26, a deliberate shift toward higher-margin passenger vehicle content.

By October 2025, Lumax acquired Greenfuel Energy Solutions (60% stake) to enter CNG and hydrogen systems. Simultaneously, board approvals in May 2026 called for buying the remaining 15.97% of Lumax FAE (oxygen sensors, now 84% owned) and selling the entire 50% stake in Lumax JOPP to the German partner (margin-dilutive, small revenue). These moves frame a portfolio realignment: scale what works, exit what doesn’t.

The SHIFT tech center in Bengaluru (R&D hub for telematics, ADAS, software-defined vehicles) opened in FY26 with ~20 engineers and annual spend of ₹5–7 Cr. The company filed revenue growth guidance of 20% CAGR through FY31 and a target EBITDA margin of 20%.

3 — Business Model: WTF Do They Even Do?

Lumax supplies plastics, metal, electronics, and alternative fuels to OEMs. The portfolio:

Advanced Plastics (53% of FY26 revenue, ₹2,566 Cr): cockpits, headliners, door panels, intake systems, fuel tanks. Think interior surfaces and air management for 4W and 2W. Content per 4W vehicle expanded to ₹75K (from ₹15K five years ago), a 5x leap. Lumax Cornaglia (50% JV with Italy) manufactures air intake systems and urea tanks for VW and Tata.

Structures & Control Systems (17%, ₹816 Cr): gear shifters (60–65% market share in India for AMT), seating structures, shift towers, control housings. Lumax Mannoh (55% subsidiary with Japan) exports automatic shifters. Orders here are ₹170 Cr.

Mechatronics (emerging, ₹281 Cr, +146% YoY): power window switches, telematics control units, antennas, oxygen sensors. Lumax FAE (84% owned) makes oxygen sensors. Lumax Ituran (50% JV with Israel) makes telematics; margin diluted post-acquisition but expected to improve 150 bps in FY27.

Aftermarket (11% of sales, ₹538 Cr, +15% YoY): lamps, accessories, audio, navigation. Over 575 channel partners and 27,500 retail touchpoints. This segment is leverage for OEM downturns.

Alternate Fuels (new, ₹383 Cr via Greenfuel, 60% owned): CNG delivery systems, hydrogen prep. Orders at ₹180 Cr. Positioned as the “alternative mobility” hedge.

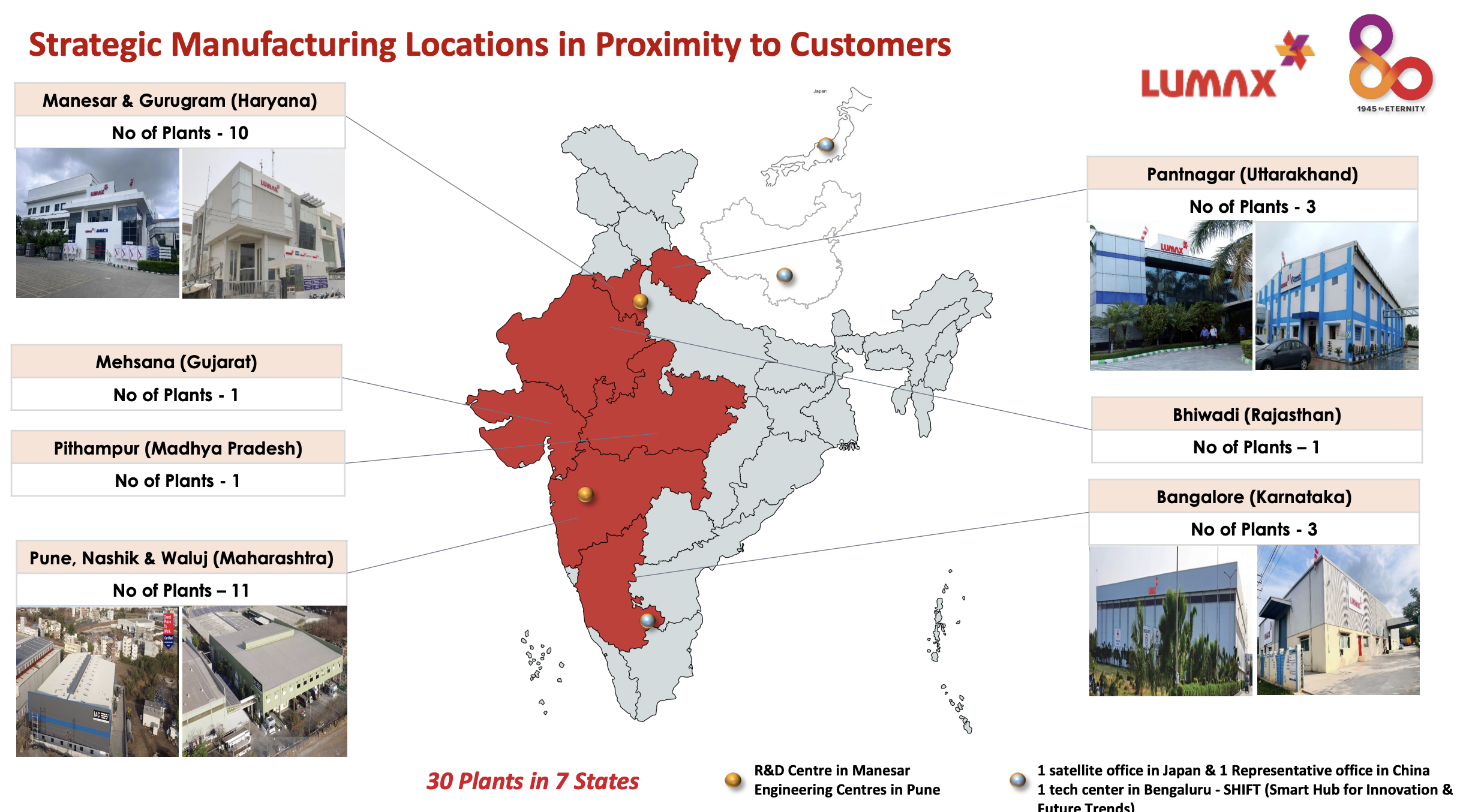

The model works via 30 manufacturing plants across 7 states, JV partnerships with Japan, Germany, Italy, Spain, Israel to localize or co-develop products, and deep OEM relationships (M&M, Bajaj, Maruti, Honda, Tata account for ~60% of revenue). No single geography dominates; all automotive is domestic. Exports are negligible.

Moat: not price (OEMs reset contracts annually), but technical capability, scale, delivery track record, and now—the shift toward electronics, software, and cleaner mobility. A 4W interior kit that talks to the car’s brain is harder to displace than a plastic trim.

4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Q4 FY26

YoY

QoQ

FY26

FY25

YoY

Revenue

1,417

+25%

+12%

4,870

3,637

+34%

EBITDA

208

+26%

+9%

705

516

+37%

EBITDA Margin

14.7%

+10 bps

-30 bps

14.5%

14.2%

+30 bps

PAT (pre-MI)

98

+22%

-10%

337

229

+47%

PAT Margin

6.9%

-10 bps

+50 bps

6.9%

6.3%

+60 bps

EPS

12.93

+50%

+6.6%

40.91

26.08

+57%

Latest Quarter (Q4 FY26): Revenue ₹1,417 Cr (third consecutive record quarter). Operating profit ₹203 Cr, a 14.7% margin. Net profit ₹98 Cr pre-minority interest. Three accounting headwinds: (1) depreciation spiked due to reclassification of Greenfuel intangible asset lives (major impact), (2) tax showed a one-time deferred reversal in Q3 (now normalized to ~26%), (3) minority interest at 10% in Q4 (distorted by the intangible reclassification); full-year FY26 minority interest at 17%, guidance 15–17% going forward. Strip the noise: operating trajectory is clean.

Full Year FY26: Record revenue at ₹4,870 Cr (34% growth). EBITDA ₹705 Cr (14.5% margin, holding steady despite a 53% jump in one-time exceptional items for Labour Code notification). Net profit ₹337 Cr, highest ever. EPS ₹40.91 (full year, not annualized).

Concall Signal: Management attributed outperformance to “robust execution, sustained customer momentum, and disciplined operational focus,” plus