LG Electronics India Q4 FY26: A ₹1,685 Crore Reality Check Hidden Behind the Air Conditioned Swagger

Section 1 — At a Glance

LG Electronics India Limited concluded its fiscal year 2026 with an intensive paradox of volume dominance and structural margin vulnerability. The consumer durable major printed its highest-ever quarterly revenue from operations during Q4 FY26 at ₹8,054 crore, marking an 8.12% year-on-year expansion against the ₹7,448 crore achieved in the corresponding previous quarter. However, this top-line acceleration failed to translate into proportional bottom-line performance. Net profit for the final quarter contracted by 8.19% year-on-year to ₹693 crore, compared to ₹755 crore in Q4 FY25, severely squeezed by currency fluctuations, intensifying promotional investments, and heightened compliance expenditures.

On a full-year basis, FY26 revenue arrived virtually flat at ₹24,605 crore, a minor 0.98% tick upward from FY25’s ₹24,367 crore. Full-year profit after tax experienced a deep retrenchment, dropping 23.51% from ₹2,203 crore in FY25 to ₹1,685 crore in FY26. While the company maintained clear operational leadership across core offline categories—retaining massive value market shares including 51.4% in microwaves and 33.5% in washing machines —the fundamental quality of earnings weakened. Return ratios felt the compression; Return on Equity plummeted from a pristine 43% down to 25% within twelve months.

High capital efficiency is rarely an ironclad guarantee; it is a variable that can easily look compromised when vast amounts of cash sit idle on the balance sheet while core profitability shrinks.

Investors must now balance the long-term potential of the company’s massive structural capex against immediate multi-front tax disputes and persistent raw material input volatility.

Section 2 — Introduction

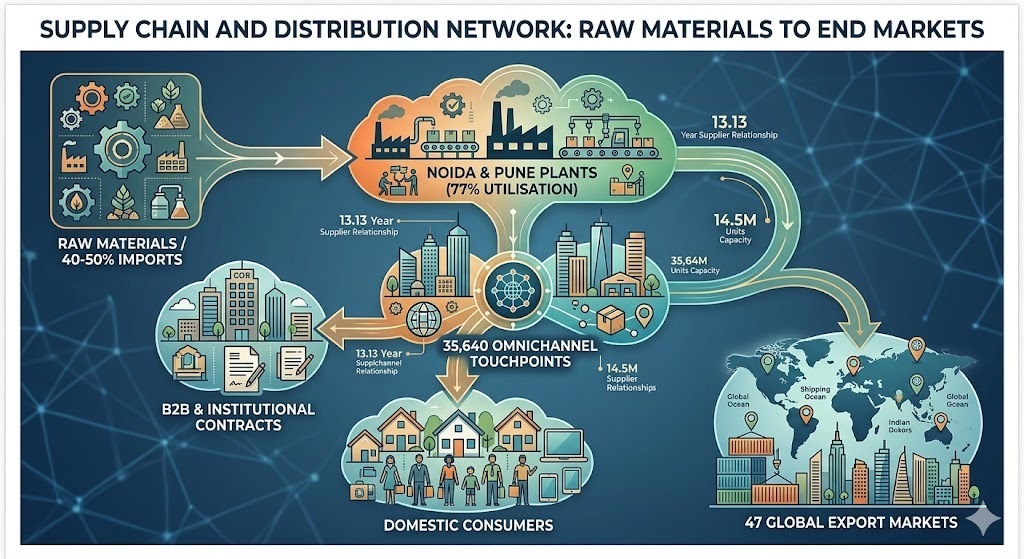

LG Electronics India entered the public consciousness with its mega ₹11,607 crore listing in October 2025 , giving domestic investors a direct vehicle into the Korean parent’s crown jewel. Established in 1997, the company has grown from a foreign brand trying to decipher Indian consumer habits into a household appliance behemoth operating out of highly scaled plants in Greater Noida and Pune.

The corporate narrative for FY26 has been defined by a split identity. On one hand, management is running a victory lap after crossing the milestone of selling over 1 million room air conditioners in a single quarter. On the other hand, the financial statements tell the tale of a corporate heavyweight taking heavy punches from a depreciating Rupee and escalating raw material costs. To correct course, the company is committing capital toward structural expansion, building out a highly anticipated third manufacturing hub in Andhra Pradesh to shift its center of gravity closer to southern demand and aggressively target export lanes.

Section 3 — Business Model: WTF Do They Even Do?

If you have stepped into an Indian home in the last two decades, you have likely stared directly at LG’s business model. They are the ultimate offline channel bullies, holding defensive fortresses across your living room and kitchen. They break their operational universe into two segments: Home Appliances & Air Solutions (H&A)—which brings in roughly 74% of full-year revenue through refrigerators, washing machines, and ACs—and Home Entertainment (HE), which accounts for the remaining chunk via televisions and media devices.

The company operates like an industrial orchestra, turning out 14.5 million products annually across 19 production lines. They don’t just sell appliances; they maintain a retail web of over 35,640 touchpoints and an army of 13,368 engineers tasked with handling a stunning 9 million service claims annually. It’s a beautifully complex logistics machine that relies on selling high-volume boxes to mass-premium buyers, while quietly trying to upsell premium products to insulate itself from commodity price spikes.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY Change (%)

QoQ Change (%)

Revenue

₹8,054

+8.12%

+95.77%

EBITDA / Operating Profit

₹945

-9.83%

+382.14%

PAT

₹693

-8.19%

+670.00%

Reported EPS

₹10.21

-8.18%

+673.48%

The financial trajectory of Q4 highlights the extreme seasonality embedded within this business. The quarter-on-quarter jump looks like a vertical line, with revenues nearly doubling from ₹4,114 crore in Q3 to ₹8,054 crore in Q4 as corporate dealers packed inventories ahead of peak summer.

During the latest earnings call, the CFO noted that while sequential operating leverage saw EBITDA margins rebound by 700 basis points over Q3, the year-on-year drop of 250 basis points was an unforced structural erosion. Management clarified that they intentionally deployed a 1.1% margin hit into channel partner promotions to clear older inventory post-BEE star rating transitions. Furthermore, a 5.6% year-on-year drop in the value of the Rupee chipped away an additional 1.0% from operational margins, proving that even market leaders are at the mercy of global currency markets.

Section 5 — Valuation Discussion

To map out where LG Electronics India sits in the current valuation matrix, we must analyze its trailing performance against the historical premium demanded by listed durables peers. Given that the latest period reported is Q4, the full-year FY26 basic EPS of ₹24.82 acts as our