1. At a Glance

Jubilant Agri & Consumer Products Ltd (JACPL) is what happens when Pidilite glue, fertiliser bags, and synthetic latex barrels are all stuffed into one corporate suitcase and listed on the stock exchange.

Market cap sits at ₹2,943 Cr, stock price at ₹1,934, down ~26% in six months — because the market clearly went: “Nice business bro, but first prove you’re not just a demerger hangover.”

Latest quarterly numbers?

Sales ₹451 Cr, PAT ₹24.3 Cr, YoY growth ~13–14%.

TTM PAT ₹124 Cr, EPS ₹82.19, ROE 31.5%, ROCE 33.2%.

Debt has slimmed down from ₹163 Cr → ₹41 Cr, promoter holding is a chunky 74.4%, and yet — zero dividend. Because apparently profits are meant for inner peace, not shareholders.

Valuation?

P/E 23x, P/B 7x.

Which means the market believes the glue sticks… but not that permanently.

Curious why a company selling adhesives + fertilisers + polymers is being judged against specialty chemical giants?

Good. Let’s dig.

2. Introduction – The Case of the Newly Freed Subsidiary

Until FY24, JACPL lived in the shadow of Jubilant Industries Ltd, quietly doing the dirty work — selling adhesives, fertilisers, polymers — while the parent hogged the spotlight.

Then came the demerger.

Agri & Consumer Products were carved out via slump sale, dumped into a fresh corporate shell, and voilà — a brand-new listed entity with old assets and new expectations.

Classic Indian market reaction:

- First year: confusion

- Second year: distrust

- Third year: either rerating or permanent exile

JACPL is currently in Year One-and-a-Half, where investors keep asking:

“Is this Pidilite-lite or just fertiliser with extra branding?”

And honestly, that’s a fair question.

Because JACPL is not a pure consumer company.

Not a pure agri play.

Not a pure specialty chemical company either.

It’s a hybrid organism, and hybrids either dominate… or confuse everyone.

So let’s understand what exactly this creature does.

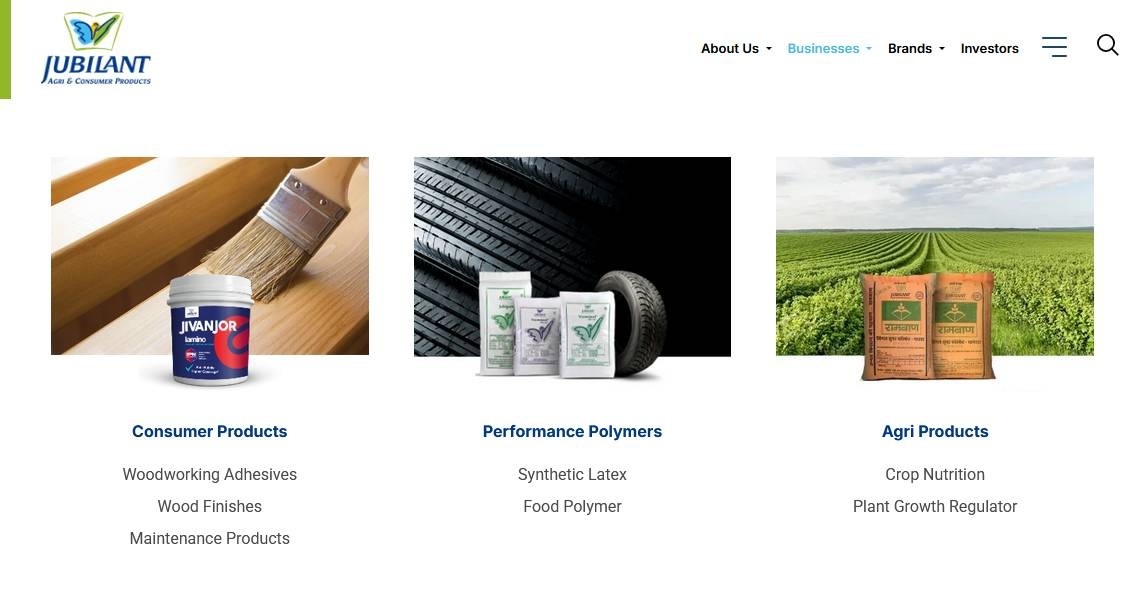

3. Business Model – WTF Do They Even Do?

Imagine explaining JACPL to a sleepy investor on a Mumbai local:

“They sell glue to carpenters, fertiliser to farmers, latex to factories, and polymers to food companies.”

Blank stare.

Let’s simplify.

Three Business Engines

1. Performance Polymers & Chemicals (~70% revenue, 9MFY25)

This is the grown-up, serious sibling.

Products:

- Synthetic latex

- Food polymers

Used in:

- Adhesives

- Packaging

- Food processing

- Industrial applications

This segment brings scale, repeat B2B demand, and relatively stable margins.

2. P&K Fertilisers (~29%)

Single Super Phosphate (SSP) manufacturing.

Low glamour, high volume, policy-linked.

Margins swing with:

- Raw material costs

- Subsidy cycles

- Government mood swings

Not sexy, but pays the bills.

3. Agri Nutrients (~1%)

Tiny today.

Optionality tomorrow.

Consumer Products – The Brand Game

This is where JACPL tries to wear its Pidilite cap.

Brands include: