ITC Hotels Ltd: Is Luxury Hospitality the New Multibagger Suite?

1. At a Glance

India’s third-largest hotel chain—recently spun off from ITC—now wants its own corner suite on the bourses. High margins, low debt, and Marriott tie-ups galore. But can valuations justify the pillow talk?

2. Introduction with Hook

Imagine a 5-star hotel with gold-plated faucets, endless buffets, and shareholder-friendly foot massages. Now imagine it demerging and listing solo. That’s ITC Hotels Ltd, a company where linen sheets meet balance sheet dreams.

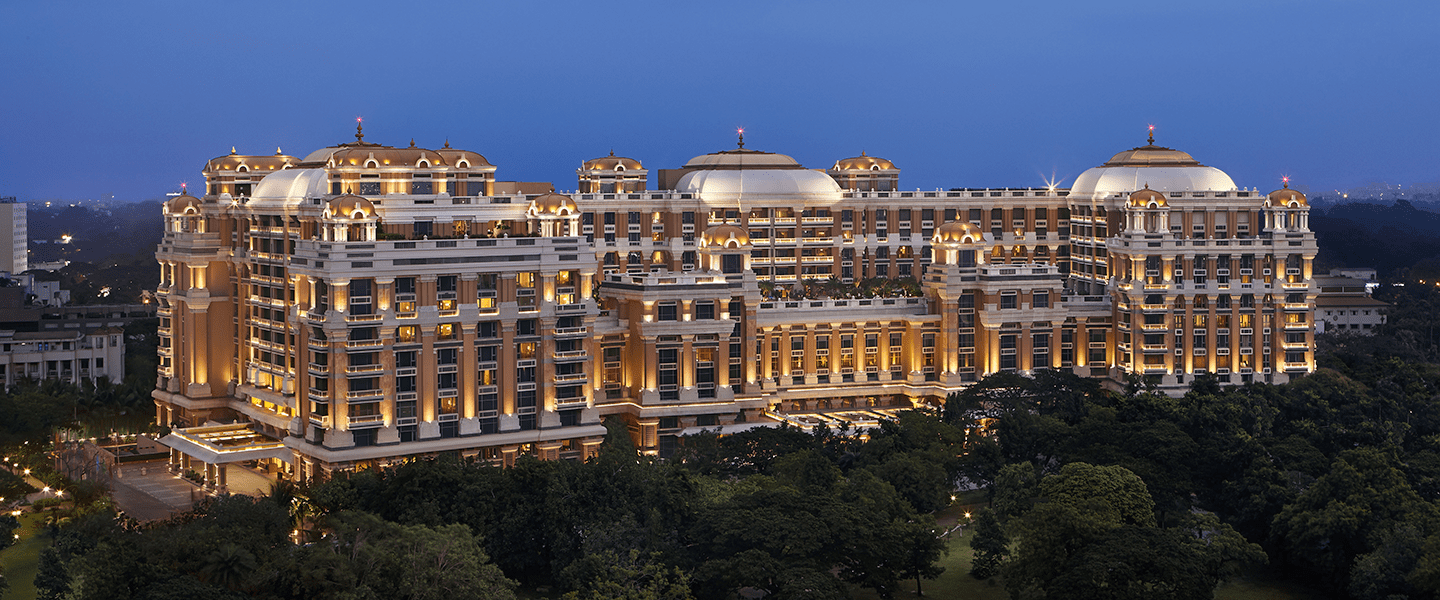

100+ hotels under 6 brands, including Welcomhotel & Fortune

FY25 Net Profit: ₹638 Cr on ₹3,560 Cr in revenue

Operating margin? 34%—they’re printing profits faster than housekeeping folds towels

3. Business Model (WTF Do They Even Do?)

ITC Hotels is in the business of premium hospitality. But this isn’t just about rooms and spas. It’s about:

Owning & Managing Hotels under brands like ITC, Fortune, and WelcomHotel

Franchising with Marriott through The Luxury Collection

Target Segments: Luxury, premium, mid-market

Strategic Capex: ₹328 Cr approved for a plush hotel in Visakhapatnam (2029 target)

Their guests get turndown service. Investors get high OPMs and zero-debt dreams.

4. Financials Overview

Metric

FY25

Revenue

₹3,560 Cr

EBITDA (Operating Profit)

₹1,211 Cr

Net Profit

₹638 Cr

EBITDA Margin

34%

EPS

₹3.05

Interest Cost

₹7 Cr

Debt

₹73 Cr

Net Cash

Positive

Key Observations:

Operating margins at 34% are chef’s kiss

Debt levels are minimal post-demerger

Huge cash outflows for capex (Visakhapatnam Hotel) = growth