Iris Clothings Q3 FY26 – ₹487mn Revenue, 46% YoY Growth… But Margins Playing Hide & Seek

1. At a Glance – The Kidswear King or Just Another Fancy Tailor?

There are companies that quietly stitch profits… and then there’s Iris Clothings stitching Disney T-shirts while stitching together a 40% growth story. Sounds exciting, right? But wait. Behind this cute baby clothing empire lies a business juggling high working capital cycles (300+ days), declining promoter holding, margin volatility, and aggressive expansion dreams. One quarter it looks like a rocket, next quarter margins vanish faster than socks in a washing machine.

Q3 FY26 came in with 46% YoY revenue growth, which is impressive for a company selling clothes to toddlers who don’t even know what inflation is. But margins? They took a hit because management decided to throw a big party for distributors and outsource some production. Because why not.

Now the big question: Is this a hidden retail brand scaling story, or just another textile company pretending to be a brand?

And more importantly… Are you buying a future Page Industries… or a slightly fancier wholesale garment shop?

2. Introduction – Welcome to the World of Tiny Clothes, Big Ambitions

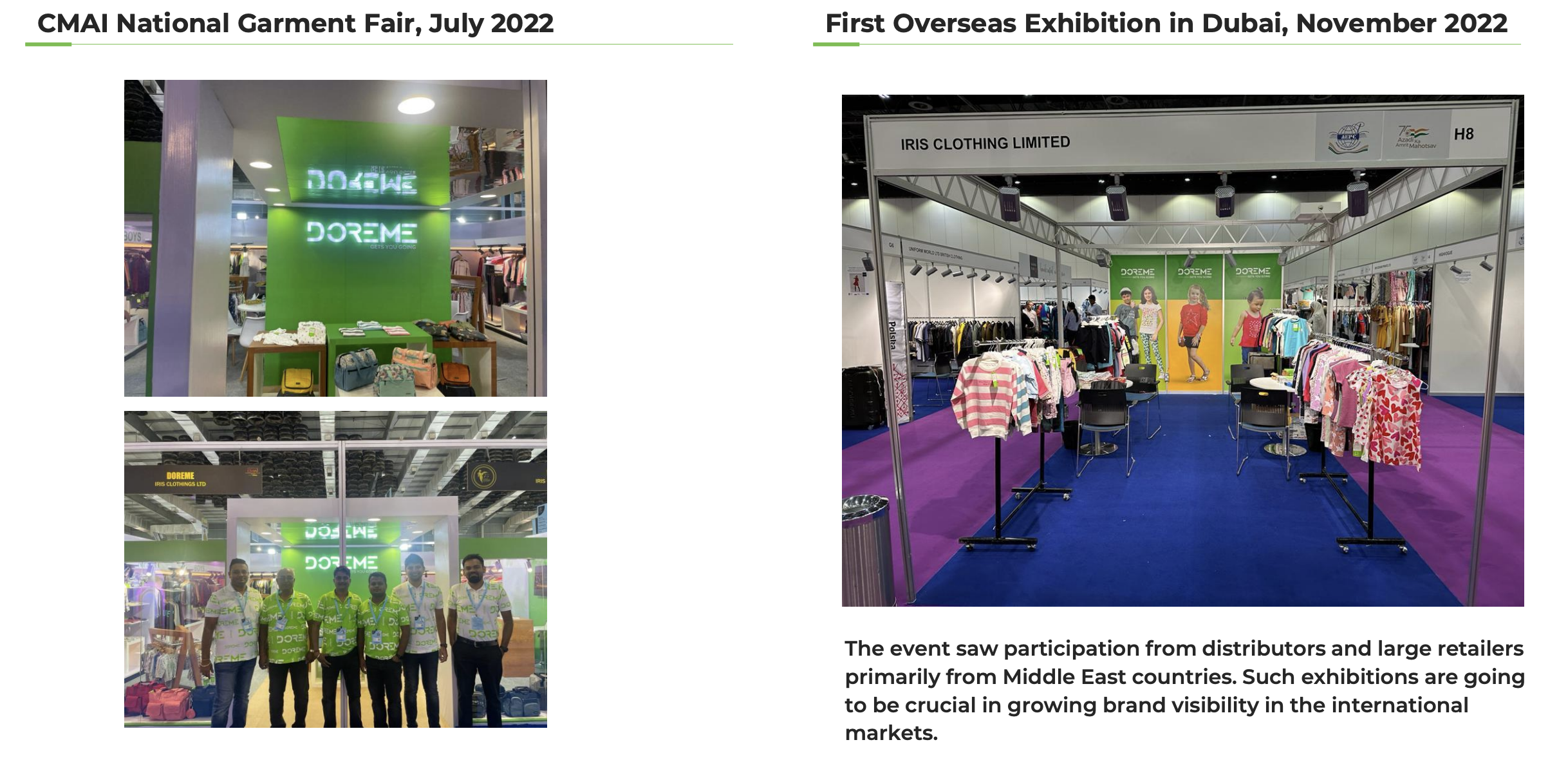

Iris Clothings is not your typical textile company. It doesn’t sell boring fabric rolls to some random exporter. Instead, it sells cute clothes for kids under the “DOREME” brand, targeting everything from infants to teenagers.

From ₹90 budget T-shirts to ₹2,500 premium Disney collections, the company is trying to play across price segments. Basically, if a kid exists… Iris wants to clothe them.

Now here’s the twist.

Most Indian textile companies struggle to build brands. They remain stuck in the B2B supply chain hell. But Iris is attempting something different:

Build a consumer brand (DOREME)

Expand into retail stores (EBOs)

Launch D2C online business

Add premium licensed products (Disney/Marvel)

Sounds ambitious. Almost too ambitious for a ₹596 crore company.

And then management casually drops this bomb in concall: “We are targeting 40–45% growth.”

That’s startup-level growth… in a textile company.

So the real question becomes: Is this ambition backed by execution… or just PowerPoint optimism?

3. Business Model – WTF Do They Even Do?

Let’s simplify this like explaining to your cousin who still thinks stocks are gambling.

Iris does three things:

1. Makes Clothes

They manufacture kidswear in-house across 10 units in Howrah.

Capacity: ~34,000 pieces/day

Target: 40,000 pieces/day

Workforce: ~1,400 employees

2. Sells Through Distributors (Old School Style)

208 distributors across India

Strong B2B wholesale network

This is where most revenue still comes from.

3. Tries to Become a Brand (New Drama)

Exclusive Brand Outlets (EBOs)

Online D2C platform (launched Feb 2026)

Disney licensing for premium products

Basically, Iris is trying to evolve from:

“Garment manufacturer” → “Branded retail company”

Now here’s the catch.

Brand building is expensive.

And management already admitted:

“Margins may take a hit due to D2C investments.”

So you’re not just buying a textile company… You’re buying a brand transition experiment.

4. Financials Overview – Numbers Don’t Lie, But They Do Confuse