01 — At a Glance

The Resurrection Play That Nobody Asked For

- 52-Week High / Low₹152 / ₹67.2

- Q3 FY26 Revenue₹150.85 Cr

- Q3 FY26 PAT₹10.74 Cr

- Q3 FY26 EPS₹1.17

- Annualised EPS (Q3×4)₹4.68

- Book Value₹160

- Price to Book0.85x

- Debt / Equity0.02x

- Operating EBITDA (Q3)₹9.11 Cr

- Promoter Holding43.05%

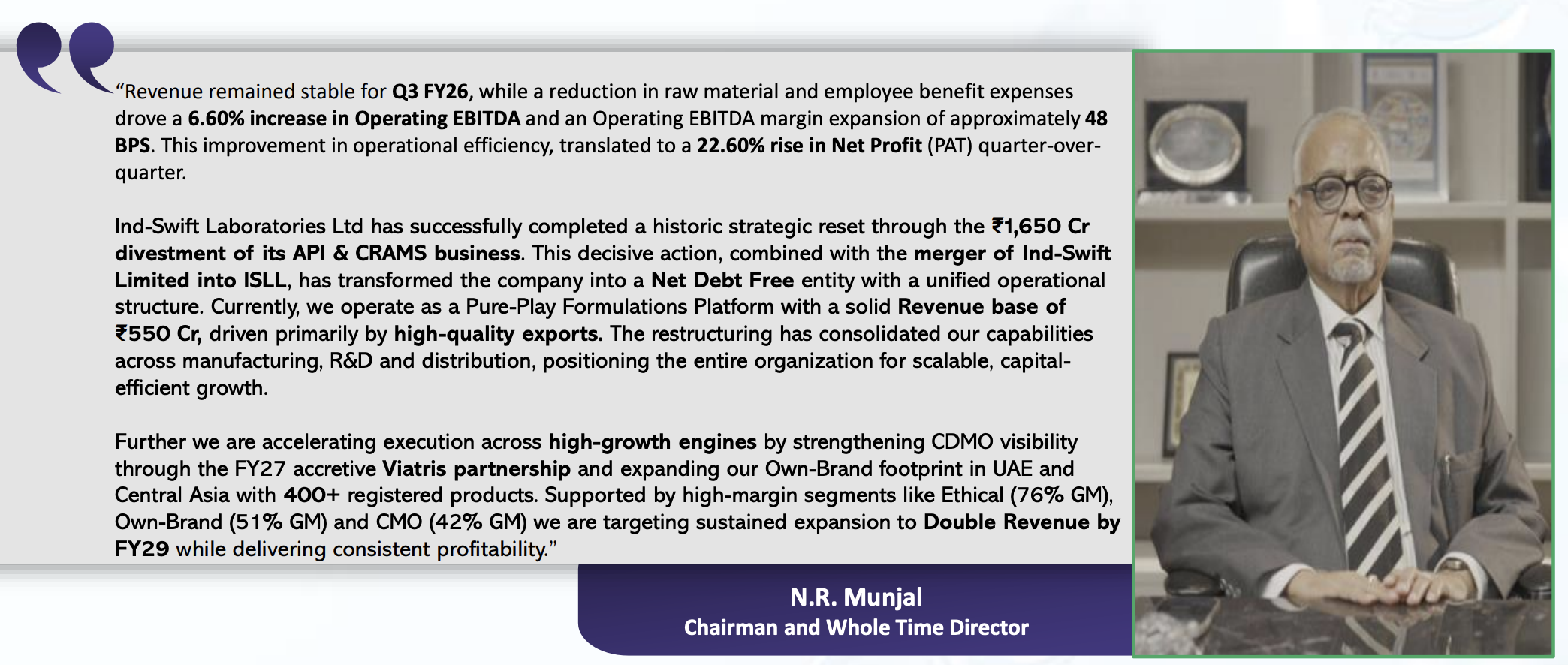

The Plot Twist: Ind-Swift just executed one of pharma’s messiest corporate restructurings — sold a ₹1,650 crore API cash cow, paid off ALL debt, merged with the parent company, and pivoted to formulations in 85+ countries. Q3 revenue ₹150.85 Cr (+17.1% QoQ), PAT ₹10.74 Cr (+22.6% QoQ), Operating EBITDA margins expanding 48 bps. Meanwhile, the stock is trading at 0.85x book value while the management is bragging about doubling revenue to ₹1,200+ Cr by FY29. This is either the trade of the decade or a beautiful trap dressed in Excel presentations.

02 — Introduction

Welcome to Pharma’s Most Confusing Restructuring

Meet Ind-Swift Laboratories. For two decades, they were a traditional API (Active Pharmaceutical Ingredient) company — the unsexy chemical factories that make the raw powder that goes into actual pills. They sold to 30+ countries, had USFDA approvals, made complex molecules like Clarithromycin (antibiotics), and generated steady cash flow.

Then in March 2024, something wild happened. They sold the entire API & CRAMS (Contract Research And Manufacturing Services) business to a PE-backed company called Synthimed Labs for ₹1,650 crores. Paid off all debt. Merged with the parent holding company, Ind-Swift Limited. Fired the old MD. Hired three new Managing Directors. Announced a ₹200+ crore capex plan. And pivoted 100% to Finished Dosage Formulations (FDF) — the actual pills and medicines that go into your body.

Q3 FY26 is the first full quarter after this reset. Revenue at ₹150.85 crores. PAT at ₹10.74 crores. Operating EBITDA margins at 5.95%, up 48 basis points QoQ. Management is promising 20-25% topline CAGR to ₹1,200+ Cr by FY29. And the stock is somehow trading at 0.85x book value despite a net debt-free balance sheet.

This is a classic restructuring story — the kind where boring businesses become interesting, old management gets replaced by hungry visionaries, and spreadsheets start showing 300 bps margin expansion arrows. Either genius. Or very, very dangerous.

Management Quote (Investor Presentation, Feb 2026): “Pure-Play Formulations Platform with solid Revenue base of ₹550 Cr, driven primarily by high-quality exports. Targeting sustained expansion to Double Revenue by FY29 while delivering consistent profitability.”

03 — Business Model: WTF Do They Even Do Now?

From Test Tubes to Tablets (Finally)

Old Ind-Swift: Made raw chemicals. Sold them to big pharma companies. Got paid. Repeat. Simple, boring, profitable.

New Ind-Swift: Makes finished medicines across three operating divisions — (a) Domestic ethical and generics for Indian doctors, (b) Export-oriented contract manufacturing for global pharma giants, and (c) Own-brand direct marketing in UAE, Africa, and Southeast Asia. Basically, they’re trying to become a diversified global pharma company in 36 months.

The three facilities are now split between export-oriented (Derabassi, Punjab — 81,325 sq meters) and domestic (Samba, Jammu — 14,700 sq meters). Derabassi holds UK-MHRA, TGA, Health Canada, and WHO-GMP approvals. Samba is the domestic cash-generation engine with access to 2,400 stockists and 8 C&F networks.

Revenue breakdown from FY25: Europe (53%), South-East Asia (16%), Others (8%), USA (5%), Canada (5%), Middle East (5%), UAE (5%), Africa (3%). Clearly, they’re playing a global game. The Viatris partnership alone is expected to add ₹200-220 Cr incremental revenue starting FY27, with commercial supplies beginning in 2026.

Ethical GM76%Highest Margin

Own-Brand GM51%Greenfield Ops

CMO GM42%Contract Mfg

Expected EBITDA Margin15-18%By FY28-29

Capacity Bomb: Derabassi can produce 9,000 million tablets, 90 million capsules, and 111 million sachets annually. Current utilization is probably 60-70%. Every percentage point of incremental utilization drops straight to the bottom line. This is the operating leverage thesis.

💬 Do you think a ₹1,100 Cr market cap company can actually execute a ₹1,200+ Cr revenue target by FY29 without any acquisitions? Or is this another case of PowerPoint ambition meeting reality?

04 — Financials Overview

Q3 FY26: The Numbers That Matter

Continue reading with a premium membership.