Igarashi Motors FY26: A 99x P/E Motor Spinning on a 4% ROCE Battery

Section 1 — At a Glance

The capital markets frequently present paradoxes where valuation multiples appear uncoupled from underlying return metrics. Igarashi Motors India Limited (IMIL) finishes the financial year 2026 with its equity trading at a Price-to-Earnings (P/E) multiple of 99.2x. This premier valuation is applied to an auto-component manufacturer that generated a Return on Capital Employed (ROCE) of 4.48% and a Return on Equity (ROE) of 2.61% over the same twelve-month period. Total revenue from operations edged up incrementally to ₹865.92 crore, representing a muted annual top-line expansion. Concurrently, full-year net profit contracted to ₹12.15 crore, down from the ₹24.17 crore recorded in the preceding year.

This material deceleration in profitability is attributed to an ongoing transformation in the core business mix. The entity is actively transitioning from its traditional, high-margin automotive DC actuator motors into domestic Brushless DC (BLDC) motor solutions aimed at consumer appliances. While this strategic pivot successfully broadens the Total Addressable Market (TAM) and reduces reliance on structural internal combustion engine (ICE) cycles, it exposes the consolidated income statement to severe margin compression. Furthermore, prolonged global customer validation cycles and structural headwinds in international shipping have created an operational bottleneck. Capital efficiency remains a critical vulnerability, as persistent investments in fixed assets and capital work-in-progress have expanded the balance sheet base without yielding a commensurate near-term cash return.

Financial Wisdom Drop: A premium valuation multiple can comfortably discount future earnings potential, but it leaves zero margin for execution delays when capital efficiency metrics sit below the risk-free rate of return.

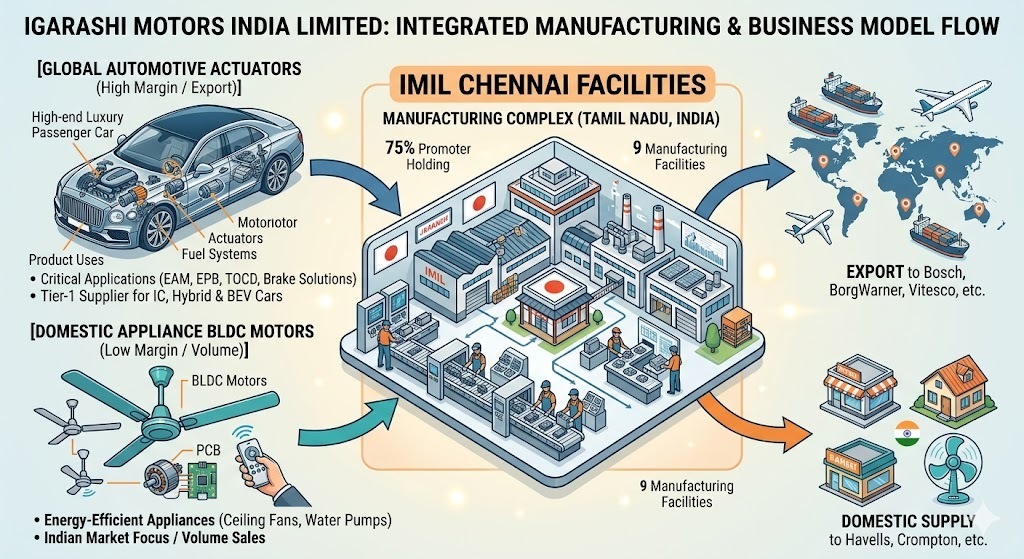

Section 2 — Introduction

Igarashi Motors India Limited (IMIL) functions as a specialized engineering entity focusing on permanent magnet micro DC motors and sub-assemblies. Established in 1992 as a tripartite joint venture involving Crompton Greaves, Igarashi Electric Works Japan, and International Components Corporation USA, the capital architecture has since consolidated under the control of the Japanese promoter group. Operating out of its manufacturing facilities in Chennai, Tamil Nadu, the corporate strategy has historically relied on global automotive supply chains, positioning IMIL as a core component provider for automated sub-systems such as electronic throttle control, exhaust gas recirculation, and electronic parking brakes.

Section 3 — Business Model: WTF Do They Even Do?

IMIL builds the miniature electric motors that quietly automate modern life. If you have ever adjusted a powered car seat or felt an electronic throttle valve click open, you have interacted with their core product portfolio. The enterprise acts as a Tier-2 and Tier-3 supplier to automotive heavyweights like Bosch, BorgWarner, and Continental, who embed these micro-motors into comprehensive sub-assemblies before shipping them to global automotive OEMs.

For decades, this was a steady, high-precision export game. However, recognizing the structural risk of being bound exclusively to passenger car cycles, management decided to enter the domestic consumer appliance market. They created a dedicated division to manufacture BLDC motor solutions for ceiling and pedestal fans, aiming to ride the wave of government-mandated energy efficiency standards.

The resulting operational architecture means IMIL is simultaneously running a sophisticated, high-barrier automotive component export engine and a localized, price-sensitive consumer durable electronics assembly shop.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY Change (%)

QoQ Change (%)

Revenue from Operations

₹225.97

+10.44%

+4.57%

EBITDA / Operating Profit

₹19.27

-14.13%

-5.54%

Profit After Tax (PAT)

₹1.59

-68.20%

-54.57%

Earnings Per Share (EPS)

₹0.51

-68.71%

-54.05%

The final three months of the fiscal year highlight the structural pressures building within the operational framework. While top-line revenue moved up to ₹225.97 crore, operating profitability moved in the exact opposite direction. EBITDA for the quarter declined to ₹19.27 crore, with the compression turning severe at the net profit level—collapsing by 68.20% year-on-year to just ₹1.59 crore.

Financial Wisdom Drop: Top-line growth without accompanying operational leverage is simply a vanity metric;