1. At a Glance

Heritage Foods is currently navigating a high-stakes environment where the raw material is becoming more expensive than the brand itself. The company delivered a Revenue of ₹45,260 million for FY26, a growth of 9.5% YoY, yet this topline expansion masks a severe squeeze on the bottom line. The “unusual industry supply environment” is not just a buzzword; it is a financial drain. Procurement prices for milk have surged to ₹46.67/L in Q4 FY26, an 8% YoY increase, which is cannibalizing margins.

The most glaring red flag is the Profit After Tax (PAT) contraction. In Q4 FY26, PAT plummeted to ₹239 million, a staggering 37.3% drop from the same quarter last year. This isn’t just a minor fluctuation; it is a warning sign that the company’s ability to pass on costs to consumers is lagging behind the blistering pace of inflation in the dairy shed. While the company boasts a wide footprint across 19 states, its dependence on the southern belt remains a concentration risk that leaves it vulnerable to regional climate shocks.

Investors are watching the Value-Added Products (VAP) segment, which now contributes 35.5% to revenue. Management is betting the farm—literally—on a new ₹220 crore greenfield ice cream facility in Shamirpet. The goal is to scale the ice cream business 5x, but the immediate reality is a 19.5% YoY decline in EBITDA for the full year FY26. The company is trading a certain degree of current profitability for the hope of future premiumization.

The debt levels are also creeping up. Borrowings have ballooned to ₹361 crore, nearly tripling from FY24 levels. While the debt-to-equity ratio remains manageable at 0.33, the rapid pace of debt-funded capex in a high-interest-rate environment requires a level of operational precision that the current margins are struggling to support. The market is witnessing a giant trying to pivot its weight while the ground beneath it—the milk supply—is shifting rapidly.

2. Introduction

Heritage Foods Ltd, established in 1992, is a veteran in the Indian dairy landscape, predominantly known for its stronghold in South India. Founded by Mr. Nara Chandra Babu Naidu, the company has evolved from a regional milk supplier into a diversified FMCG player dealing in milk, value-added products, cattle feed, and renewable energy.

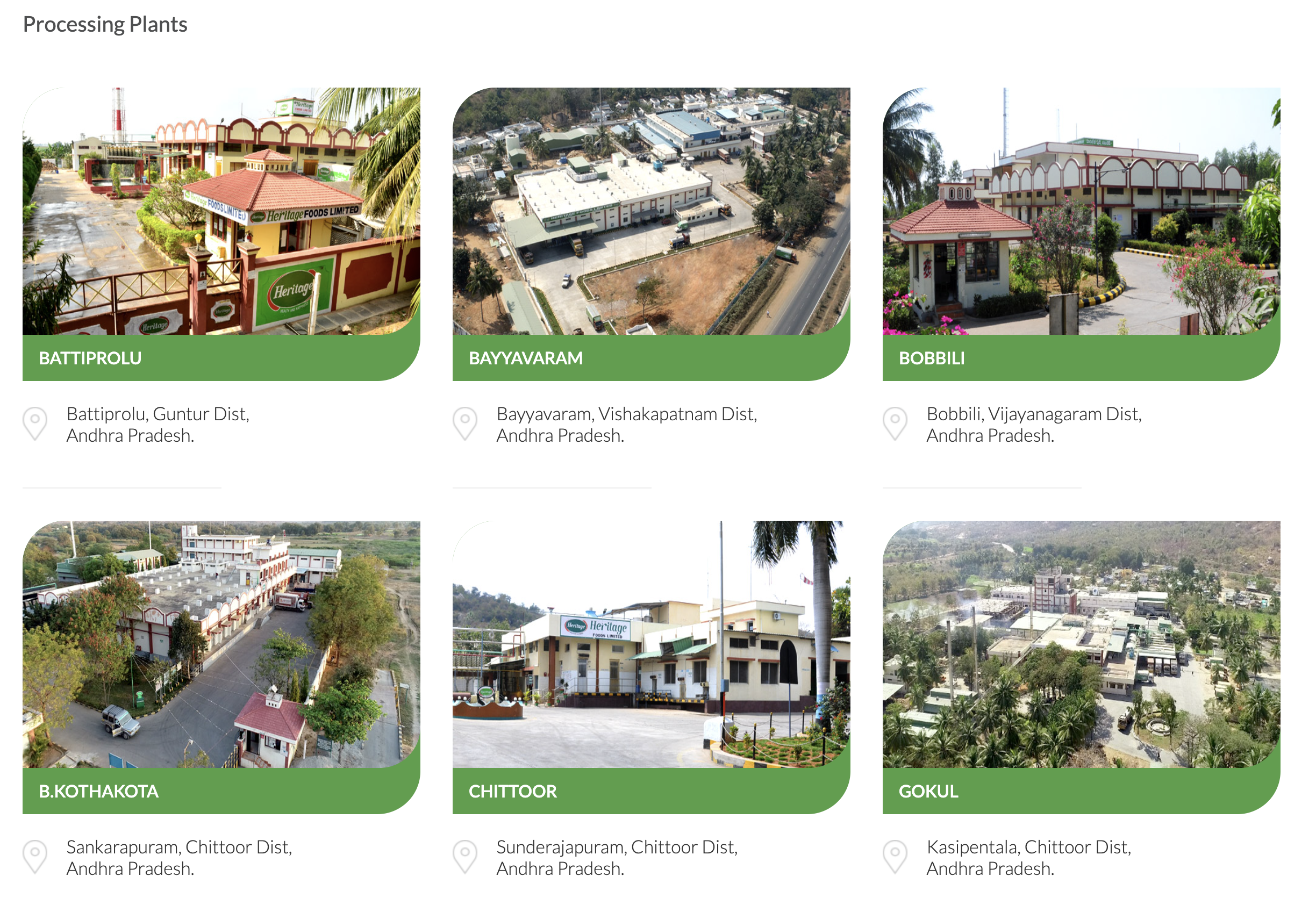

The company operates a complex “farm-to-table” engine, procuring nearly 1.7 million liters of milk per day (LLPD) from a network of over 300,000 farmers. This procurement machine feeds 18 processing plants with a total capacity of 2.83 MLPD.

However, the “Heritage” brand is currently being tested by a “double whammy” of climate impact and global commodity shifts. Excess rainfall and a weak flush season have hampered farm productivity, while high global prices for butter led to domestic shortages. This forced Heritage to buy bulk fat at elevated prices, hitting the very margins they seek to protect.

The business is now at a crossroads. It is aggressively pushing into Premiumization—launching organic milk, probiotic buttermilk, and high-protein paneer. The acquisition of a 51% stake in “Get-A-Way” (Peanutbutter and Jelly) signals a desperate or perhaps strategic need to find growth outside the commoditized liquid milk market.

3. Business Model – WTF Do They Even Do?

At its simplest, Heritage Foods is a massive middleman that buys milk from cows and sells it to humans, taking a cut in between. But they’ve realized that selling plain white milk is a low-margin race to the bottom.

The revenue mix