Hatsun Agro Q4 FY26: The ₹9,959 Crore Dairy Juggernaut and the WhatsApp Financial Leak Drama

Section 1 — At a Glance

Hatsun Agro Product Limited concluded its fiscal year 2026 by reporting a headline revenue from operations of ₹9,959.22 crore, registering an impressive growth of 14.48% compared to the ₹8,699.76 crore delivered in fiscal 2025. The bottom line also demonstrated powerful momentum, with reported profit after tax (PAT) climbing 27.76% to ₹356.20 crore from ₹278.81 crore in the previous fiscal year. This performance was underpinned by an expanding operational footprint, geographical diversification across multiple Indian states, and the successful integration of its newly acquired subsidiary, Milk Mantra Dairy.

However, this solid corporate trajectory was juxtaposed against a highly unusual governance mishap during the third quarter of the fiscal year. In January 2026, a key managerial person accidentally uploaded a draft of the unreviewed quarterly financial performance onto WhatsApp. While the company moved quickly to freeze trading windows and remediate the systemic information leak, the incident injected a dose of corporate drama into an otherwise predictable consumer staple story. Meanwhile, macro tailwinds via expected goods and services tax (GST) structural overhauls are positioning the ice cream and value-added dairy segments for aggressive volume elasticities. Investors are weighing the efficiency gains from a largely concluded capital expenditure cycle against the near-term marketing outlays required to seed nascent geographical territories outside the home state of Tamil Nadu.

Real corporate value cannot be manufactured by cosmetic branding; it is earned when operational cost efficiency satisfies an inelastic consumer habit.

The subsequent segments analyze whether this private dairy champion can turn high volume into sustainable premium equity or if it remains vulnerable to the fundamental volatilities of farmgate economics.

Section 2 — Introduction

Hatsun Agro Product Limited stands as the largest private-sector dairy operator in India. Originating over five decades ago as a modest ice cream enterprise under the “Arun” banner, the corporate entity has institutionalized cold-chain logistics across South India and is aggressively penetrating Central and Eastern markets. The company has evolved from a single-state milk delivery system into a diversified multi-brand consumer staple house.

This analysis is prompted by the publication of Hatsun’s audited full-year financial results for fiscal year 2026. This period marks a major milestone as the company approaches the coveted ₹10,000 crore top-line benchmark and shifts its operational philosophy from heavy capital build-out to capacity utilization and regional market cultivation. With credit rating upgrades confirming its improved balance sheet liquidity, the corporate narrative is transitioning from an aggressive, asset-heavy regional explorer into a consolidated national consumer giant.

Section 3 — Business Model: WTF Do They Even Do?

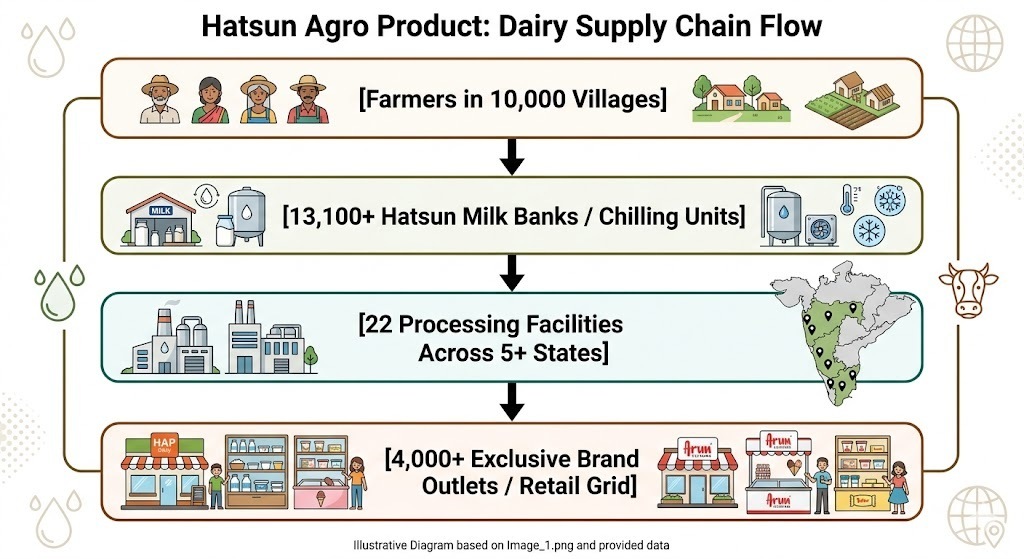

At its core, Hatsun operates a massive, daily direct-to-consumer and direct-to-farm supply network. It handles over 4 million liters of milk daily by managing relationships with approximately 400,000 to 500,000 dairy farmers distributed across 10,000 villages. The infrastructure relies on a proprietary grid of over 13,100 Hatsun Milk Banks and active bulk coolers that test, chill, and lock raw material quality right at the point of origin.

On the front end, Hatsun bypasses conventional wholesale dependencies by routing product lines through more than 4,000 exclusive retail touchpoints, primarily operating under the HAP Daily and premium Ibaco store concepts. Its consumer portfolio spans basic liquid pouches (Arokya), mass-market frozen treats (Arun Icecreams), premium artisanal desserts (Ibaco), and value-added culinary essentials like ghee, paneer, and curd. Rather than positioning itself as a standard agricultural processor, management treats its distribution network and consumer brand memory as its primary economic moat.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Performance Trend

The table below demonstrates Hatsun’s operating metrics for the concluding quarter and full fiscal year ending March 31, 2026.

Metric

Latest Quarter (Q4 FY26)

YoY (vs Q4 FY25)

QoQ (vs Q3 FY26)

Full Year FY26

Full Year FY25

YoY Annual

Revenue from Operations

₹2,577.63

17.01%

9.05%

₹9,959.22

₹8,699.76

14.48%

EBITDA

₹238.34

22.95%

-0.19%

₹1,190.34

₹1,029.67

15.60%

PAT

₹50.89

18.32%

-15.99%

₹356.20

₹278.81

27.76%

Reported EPS (₹)

₹2.28

18.13%

-16.18%

₹15.99

₹12.51

27.82%

Note: Q4 FY26 and Q4 FY25 revenue and expense metrics match the audited financial ledger balancing figures. Annual EBITDA calculated as PBT + Interest + Depreciation (FY26 EBITDA = 470.46 + 146.30 + 573.58 = 1,190.34; FY25 EBITDA = 377.30 + 181.89 + 470.48 = 1,029.67).

Financial Performance Commentary

Hatsun’s top-line acceleration reflects continuous volume growth in its home territories and a wider footprint in Maharashtra and Odisha. While annual net profit surged 27.76%, sequential quarterly profit fell 15.99%, highlighting the inherent seasonal fluctuations