Gujarat Fluorochemicals Mar 2026: The ₹6,000 Cr EV Bet Meets a 69x P/E Reality

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

Section 1 — At a Glance

The headline numbers for Gujarat Fluorochemicals Limited (GFL) reflect a business caught in a massive, capital-intensive transition. For FY26, the company reported consolidated revenue of ₹4,996 crore and an EBITDA of ₹1,290 crore. Net profit landed at ₹574 crore, translating to an EPS of ₹52.25.

Beneath these top-line figures lies an aggressive pivot. Management is channeling roughly ₹6,000 crore into GFCL EV, its battery materials subsidiary, targeting the electric vehicle and energy storage system ecosystems. This has pushed borrowings to ₹2,290 crore. Growth requires capital, but heavy capex cycles often test investor patience before they deliver returns.

In Q4 FY26, consolidated revenue stood at ₹1,369 crore, a respectable 11.7% increase year-on-year. However, PAT contracted sharply by 42.9% to ₹109 crore in the same period, signaling margin compression amidst scaling costs. The market is currently pricing this transition at roughly 69 times trailing earnings, demanding flawless execution. When you price a stock for perfection, even a slight delay in commercialization becomes a valuation risk.

Will the integrated battery materials platform deliver the promised 25% EBITDA margins, or will the weight of the expansion drag down the legacy fluoropolymers business? The coming quarters will decide.

Section 2 — Introduction

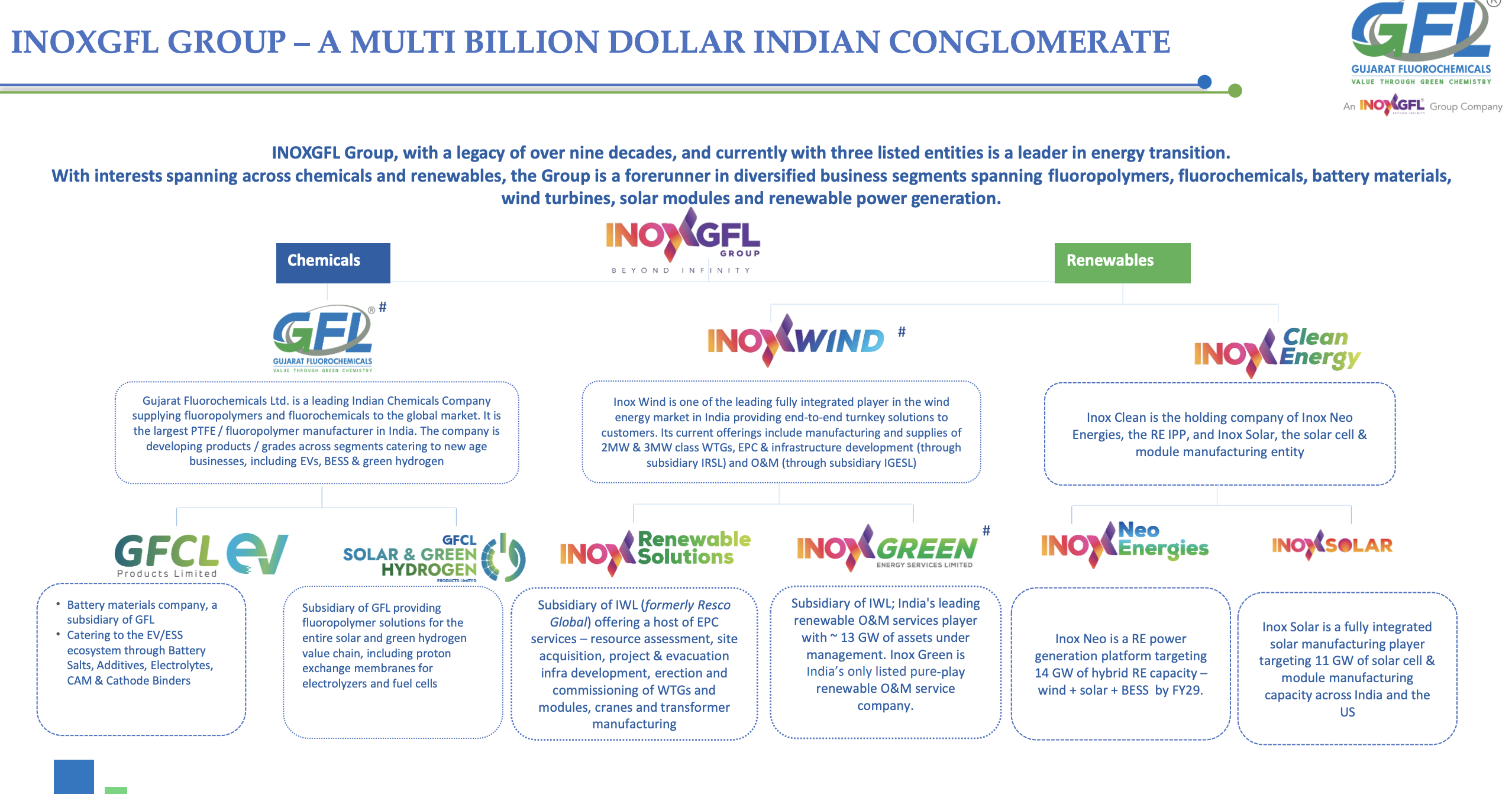

Gujarat Fluorochemicals started as a standard chemical manufacturer and has evolved into a proxy for global megatrends. Spun out of GFL Ltd in 2018, it is the cornerstone of the INOXGFL Group’s chemical ambitions.

Historically, the company built its fortune on PTFE (the stuff that makes your pans non-stick) and refrigerants. Now, they are navigating a multi-billion-dollar shift to supply the exact chemicals needed for EV batteries, solar panels, and semiconductor fabs. It’s a classic story of an old-economy manufacturer putting on a new-economy tech jacket, and the market is watching closely to see if the zipper holds.

Section 3 — Business Model: WTF Do They Even Do?

If you read the annual report, GFL is a “leading producer of Fluoro-polymers, Fluoro-specialities, Chemicals and Refrigerants.” In plain English, they make the invisible materials that prevent modern technology from melting, sticking, or catching fire.

Their legacy business revolves around bulk chemicals like caustic soda and refrigerants (R-22 and R-32). But the star of the show is the Fluoropolymers division, which generates over half their revenue. Now, through their subsidiary GFCL EV, they are manufacturing LiPF6 salts, LFP Cathode Active Materials (CAM), and binders. It’s a beautifully complicated portfolio. One half of the company is keeping your office air-conditioner cold, while the other half is desperately trying to convince global automakers that an Indian chemical giant can safely power their lithium-ion batteries.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Mar 2026

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

1,369

11.7%

20.5%

EBITDA

307

0.3%

11.6%

PAT

109

-42.9%

6.8%

EPS

9.92

-42.9%

6.8%

A 11.7% revenue jump is the kind of topline growth that management teams frame and put on their desks. But the 42.9% collapse in quarterly PAT is the elephant in the boardroom. Earnings quality is rarely determined by how much you sell, but by how much of it survives the journey to the bottom line.

In the latest concall, management was eager to talk about the future, noting that “all the initial capacities planned under phase one have now been commissioned and contracted for.” They called the EV battery materials segment “an important inflection point.” Inflection points are usually written down somewhere in management presentations. We’ll be watching the