Gem Aromatics Ltd Mar 2026: The ₹260 Crore Capex Bill with a ₹1 Crore Profit Side-Order

Section 1 — At a Glance

Gem Aromatics Limited entered the public markets in August 2025 with a ₹451 crore IPO flash, but its full-year financial report for March 2026 reveals an acute state of operational transition. The headline data shows consolidated annual revenue declining by 27.3% to ₹366.47 crore, down from ₹503.95 crore in the prior fiscal year. Concurrently, consolidated net profit collapsed by 97.3%, landing at just ₹1.43 crore compared to the ₹53.38 crore recorded in March 2025. This dramatic bottom-line erosion was fundamentally driven by a severe contraction in operating margins alongside a sharp escalation in depreciation charges. Annual depreciation expanded from ₹7.34 crore to ₹22.59 crore following the extensive capitalization of the new production facility in Dahej, Gujarat.

Investor attention remains intensely anchored to the massive capacity expansion under its wholly owned subsidiary, Krystal Ingredients, where approximately ₹260 crore has been capitalized out of a planned ₹270 crore total capex. However, this structural expansion has coincided with intense near-term external headwinds. Geopolitical friction severely disrupted high-margin mint exports to the United States and triggered severe pricing and supply volatility in essential petrochemical inputs like phenol. Consequently, the company’s return on capital employed (ROCE) deteriorated sharply from 19.3% to 3.4%. While the balance sheet reflects a major asset expansion, near-term corporate earnings have effectively stalled under the weight of underutilized infrastructure and global trade dynamics. An asset expansion funded ahead of demand is simply an expensive exercise in adding fixed overhead until utilization returns. The immediate future hinges entirely on whether global supply chains normalize quickly enough to feed these newly built continuous-process chemical lines.

Section 2 — Introduction

Gem Aromatics has spent nearly three decades scaling its footprint as a manufacturer of specialty ingredients, navigating the delicate transition from natural mint extraction to advanced synthetic aroma chemistry. The company’s historical identity was anchored firmly to the domestic agricultural mint belt. However, its contemporary corporate strategy involves moving down the value chain into hyper-specialty molecules, cooling agents, and phenol derivatives. This structural shift led to its listing on the NSE and BSE in August 2025, raising a total of ₹451 crore, including a ₹175 crore fresh issue meant to de-leverage the balance sheet and clear the way for its massive asset deployment.

The fundamental risk for any commodity-adjacent specialty player is timing. Gem Aromatics chose to commercialize its massive Dahej greenfield project precisely when global trade barriers and geopolitical supply-chain blockages were peaking. The underlying business remains structurally sound, boasting an expansive portfolio of approximately 70 products and deep multi-year institutional relationships with global FMCG heavyweights. Yet, the fiscal year 2026 performance underscores the exact friction that occurs when legacy cash cows slow down before new manufacturing engines have been fully certified and throttled up.

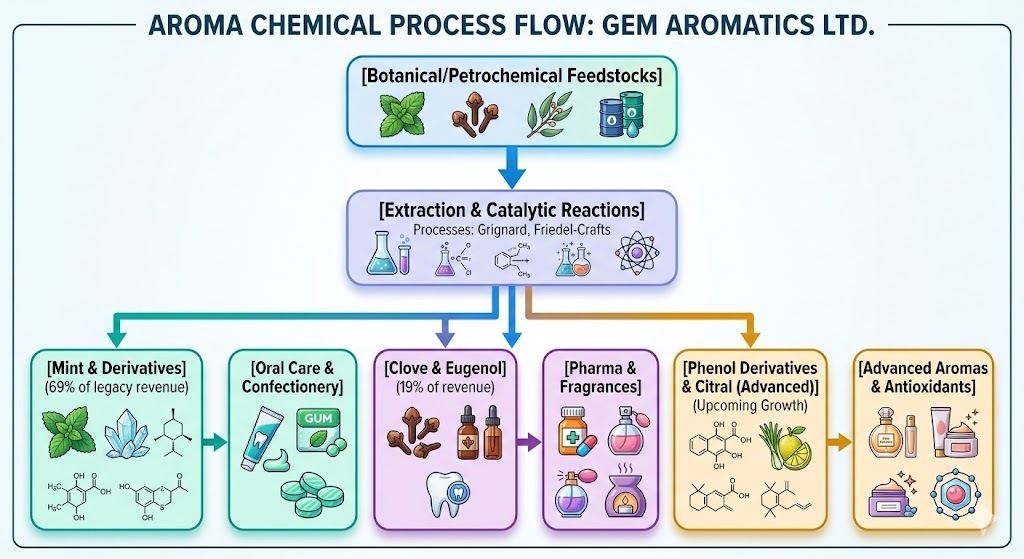

Section 3 — Business Model: WTF Do They Even Do?

To understand Gem Aromatics, you must visualize a business that functions as the invisible taste, smell, and temperature behind your daily routine. If you brushed your teeth this morning with a major brand, washed your hands, or popped a confectionery mint, you likely consumed their molecules. They take basic botanicals and petrochemical feedstocks and subject them to complex reactions like Grignard and Friedel-Crafts to create high-purity aroma chemicals and essential oils.

Their business model historically relied on the mint vertical, which commanded a dominant 69% of total revenues in fiscal year 2025. This is an environment where they control a staggering 53% to 55% share of India’s positioning in the global supply landscape. However, raw mint extraction is a volatile, low-margin game. To fix this, management forward-integrated into high-value value-added derivatives like cooling agents (the chemical compounds that give toothpaste and gum that sub-zero kick without using pure menthol).

They also control a highly defensive clove oil and eugenol extraction setup, maintaining a 65% domestic market share in India for eugenol. The entire strategic architecture is currently shifting toward advanced phenol derivatives and citral chemistry at their massive new Dahej site. The goal is to evolve from a basic ingredient vendor into a highly qualified, specialized custom manufacturing partner (CMO/CDMO) for global clients. The challenge, of course, is that global clients take months to audit a facility, leaving expensive steel tanks sitting empty in the interim.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Mar 2026

Dec 2025

Sep 2025

Jun 2025

Mar 2025

YoY (%)

QoQ (%)

Revenue

110.41

78.90

89.53

87.63

202.22

-45.4%

+39.9%

EBITDA / Operating Profit

15.71

7.02

3.05

14.86

45.87

-65.7%

+123.8%

PAT

1.01

-4.99

-2.58

7.98

27.60

-96.3%

—

Reported EPS (₹)

0.19

-0.96

-0.49

1.70

5.89

-96.8%

—

The financial data highlights the stark contrast between historical comparisons and near-term direction. On a year-on-year basis, the March 2026 quarter looks like an absolute disaster zone—revenue slashed nearly in half and operating profits dropping 65.7%. This severe drop stems from the fact that the previous year’s fourth quarter was the peak export period for high-margin US-bound mint shipments, before tariff confusion halted new orders.

However, looking sequentially, the operational recovery is highly visible. Revenue rebounded sharply by 39.9% from the December 2025 quarter, while operating profit surged 123.8% off a very low base. The major structural drag on net profit remains non-cash depreciation, which escalated to ₹9.01 crore in the current quarter due to the complete capitalization of the ₹260 crore Dahej asset base. When fixed overhead increases overnight by multiple orders of magnitude, sequential volume recovery is the only mechanism that can save the bottom line from mathematical obliteration.

What is Management Promising in the Coming Quarters?

During the May 2026 investor conference call, management chose to completely bypass near-term FY27 utilization guidance, citing high geopolitical ambiguity and ongoing customer qualification timelines. However, they provided an explicit, highly ambitious long-term target for fiscal year 2028. The CEO and directors noted that they expect a consolidated turnover of approximately ₹1,100 crore by FY28, with sustainable EBITDA margins settling between 16% and 18%.

Management emphasized that the newly capitalized Dahej asset base has a theoretical asset turnover ratio of 3 to 3.5 times, translating into peak revenue potential of nearly ₹800 crore from that single site. Regarding the immediate quarters, the CEO noted: