Ganesh Infraworld Ltd Mar 2026 : Order Book Surges 254% but Cash Generation Bleeds Deeply

Section 1 — At a Glance

Ganesh Infraworld Limited’s financial metrics for the fiscal year ended March 31, 2026, present a striking divergence between rapid top-line scaling and structural cash-flow stress. The company reported an 55.24% expansion in revenue from operations to ₹835.55 crore, compared to ₹538.22 crore in the previous fiscal year. Profit before tax moved upward by 79.20% to ₹95.64 crore , while net profit for the year grew by 90.19% to reach ₹76.17 crore. This volume growth was mirrored in the fourth quarter, where quarterly revenue climbed by 44.72% year-on-year to ₹229.58 crore , pushing quarterly net profit up by 110.50% to ₹24.46 crore.

However, investor attention is increasingly drawn to the operational balance sheet. Despite robust accounting profits, cash flow from operating activities remained deeply negative at -₹40.90 crore for FY26, following a negative outgo of -₹80.14 crore in FY25. This severe mismatch is driven by an intense working capital footprint, with trade receivables ballooning from ₹116.92 crore to ₹337.48 crore , and inventory tracking upward from ₹39.93 crore to ₹111.97 crore. Consequently, debtor days climbed from 79 days to 147 days. To sustain this asset growth, the company relied heavily on leverage. Total borrowings escalated by 1,206.24% from ₹37.85 crore to ₹494.41 crore , driving annual interest obligations from ₹1.91 crore to ₹9.76 crore. Book profits lack utility if they reside permanently in a customer’s ledger. While the massive multi-quarter order book provides strong visibility, the structural shift into capital-intensive mining operations and higher-complexity water engineering requires close observation.

Section 2 — Introduction

Ganesh Infraworld Limited has transformed rapidly from a local partnership firm established in 2017 into an infrastructure player listed on the National Stock Exchange SME platform in December 2024. Historically functioning as a traditional sub-contractor for large engineering, procurement, and construction (EPC) conglomerates, the entity has altered its strategic direction to bid directly for capital projects via joint venture routes and special purpose vehicles.

This review is prompted by the publication of the audited full-year financial results for the fiscal year ended March 31, 2026. The period has seen aggressive commercial shifts: the deployment of a new equipment-leasing division, a large corporate acquisition to cement an entry into mining logistics, and an expanding order book that crossed ₹2,200 crore during the year. The primary objective is to analyze whether this breakneck pace of expansion is structurally stable or if the balance sheet is being overextended to deliver cosmetic growth.

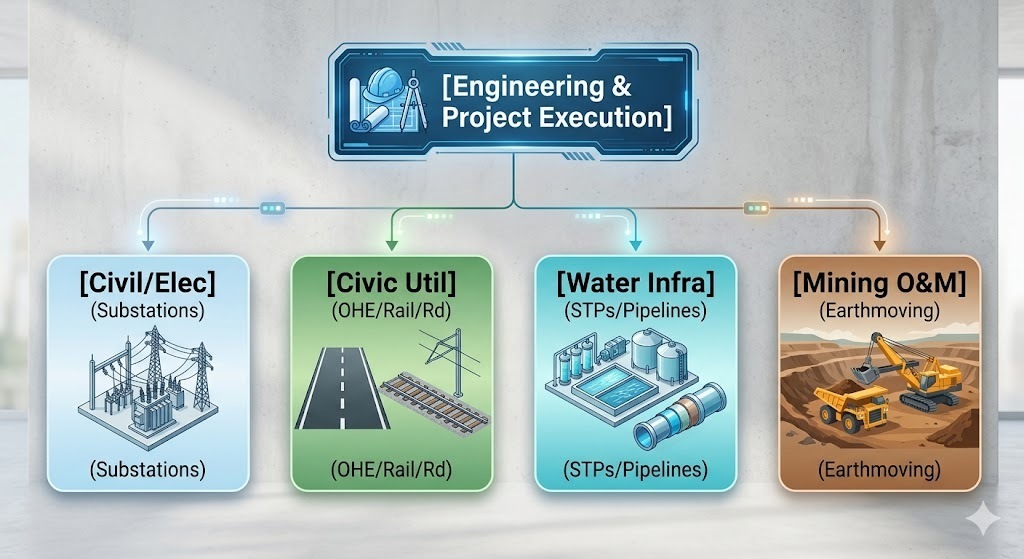

Section 3 — Business Model: WTF Do They Even Do?

Ganesh Infraworld operates as an engineering and construction execution partner across four principal infrastructure verticals. Historically, its revenue core lay in Civil and Electrical Infrastructure, where it erects industrial warehouses, installs extra-high-voltage substations, and executes underground cabling. In Civic Utilities, it constructs roads, bridges, and handles the electrification of railway overhead equipment. Its Water Infrastructure segment focuses on treatment plants and bulk cross-country pipelines, moving strategically away from low-margin household connections. The newest and most capital-intensive segment is Mining Operations, where the company takes on long-term contracts for overburden removal and heavy equipment fleet maintenance.

The operation relies on a mix of unit-price item-rate contracts and cost-plus percentage-rate contracts. While subcontracting for mega-infrastructure players gives them access to technical capabilities without intensive working capital requirements, the company is systematically increasing its direct-bidding mix to eliminate intermediate margin leakage.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

The company files financial results on a quarterly frequency. The table below outlines execution performance over recent sequential and trailing periods:

Performance Trajectory

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

229.58

44.72%

6.62%

EBITDA / Operating Profit

29.59

105.49%

1.27%

PAT

24.46

110.50%

28.47%

EPS (₹)

5.73

110.66%

28.48%

The trailing momentum reflects aggressive mid-year order execution. However, operating margins softened slightly by 70 basis points on a sequential quarter basis to 12.89%, highlighting the impact of initial mobilization costs on newer project sites.

What is Management Promising in the Coming Quarters?

During recent interactions, management expressed strong confidence in maintaining an upward growth trajectory, targeting elevated execution run-rates through the next fiscal year. They highlighted that historical revenue skews toward the second half of the year will persist due to seasonal monsoon disruptions