Frontier Springs Ltd FY26: When Margins Widen Faster Than the Order Book

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1 — At a Glance

Frontier Springs just delivered something the rail supply chain rarely gifts twice: volume and profitability in the same year. Revenue climbed 39% to ₹322 crore; EBITDA margins bloated 533 basis points to 26.8%; PAT nearly doubled to ₹61.31 crore. The company supplies compression springs and forging to Indian Railways—essentially the shock absorber that keeps Vande Bharat Express riders from shaking themselves to pieces.

Orders are queuing. FY27 ambition is ₹500 crore gross—30% growth again.

But there’s a wrinkle: the orders locked in are fixed-price. Steel costs haven’t locked in with them. Management flagged margin risk if raw material inflation lingers.

The balance sheet is nearly debt-free and cash generation is steady. P/E sits at 28.5x, a hair below the peer median of 27.4x.

The central tension: can a company on the margin-upswing maintain both growth and profitability when its customers refuse to renegotiate?

2 — Introduction

Frontier Springs is a 45-year-old manufacturer of hot coiled compression springs, air springs, and forged components. Its primary customer is Indian Railways—a relationship that accounts for the majority of revenue and explains why management mentions government capex plans with the frequency of a chant.

The company operates two manufacturing plants: Kanpur (Uttar Pradesh) and Poanta Sahib (Himachal Pradesh), with a combined installed capacity of 8,700 tonnes per annum for springs and 1,200 tpa for forgings. It was founded in 1981 and has remained a private, founder-family-controlled business—51.8% held by the Bhatia family.

FY26 marked a turning point: the company scaled rapidly across all three divisions (coil springs, forgings, air springs) and entered the fiscal year with an order book of ₹250–370 crore, depending on when you measure. The earnings concall in June 2026 reframed FY27 as a ₹500 crore revenue play.

3 — Business Model: WTF Do They Even Do?

Coil Springs (~₹175 Cr, ~54% of FY26 gross): hot coiled compression springs that absorb the shock and vibration of trains. These are fitted to freight wagons, coaching stock, diesel locomotives, and electric locomotives. They arrive in various diameters (10–65 mm wire thickness) and are made from chrome-moly or chrome-silicon steel rods with epoxy coatings. Springs are ordered by Indian Railways in long tenders; the company supplies approved component.

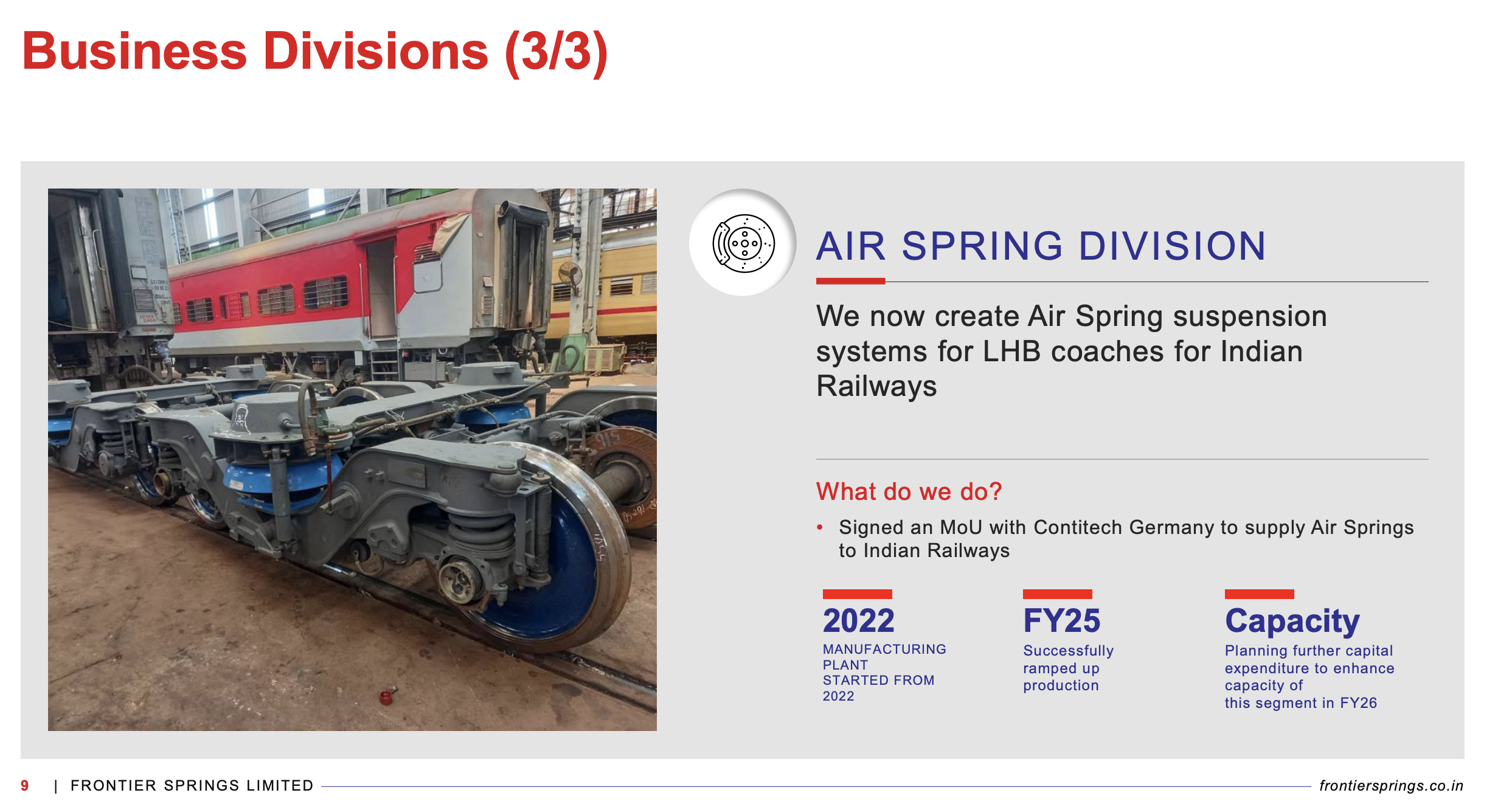

Air Springs (~₹150 Cr, ~47% of FY26 gross): rubber bellows filled with compressed air, used in modern LHB (Linton Hopkinson Bogie) coaches. The company works under an MOU with Contitech (Germany), who supply the rubber bellows; Frontier manufactures the metal frame and final assembly. This is a newer play—production kicked off in FY22 but only scaled meaningfully in FY25/FY26. Capacity is still ramping: current run-rate is 180–200 coach sets/month (a coach set = 4 air springs); installed capacity is ~300 sets/month, but testing is the bottleneck.

Forgings (~₹60+ Cr, ~19% of FY26 gross, rapidly growing): components like anti-roll bar assemblies, screw couplings, draft gear assemblies, brake block hangers, and wedges. Weights range from 100 grams to 80 kilograms. The division uses a 1-tonne, 3-tonne, and newly installed 6-tonne hammer (added in FY25). The 6-tonne hammer is currently running single-shift (8 hours) with 16 hours available; management sees non-Railways industrial OEMs (L&T, JCB, Caterpillar) and export as the fill-up lever.

The Math: Coil springs are high-volume, relatively commoditised; the margin game is scale and execution. Air springs are higher-margin and newer; testing bottleneck is the key constraint. Forgings are the strategic swing—underutilized capacity, margin-selective positioning, and a captive 6-tonne hammer that hasn’t been fully fed.

4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

FY26

FY25

YoY Change

Q4 FY26

Q3 FY26

QoQ Change

Revenue

322.06

231.34

+39.2%

82.54

81.43

+1.4%

EBITDA

86.31

49.66

+73.8%

23.54

20.27

+16.1%

PAT

61.31

34.66

+76.9%

16.59

14.28

+16.2%

EPS (annualised)

51.9

29.93

+73.4%

–

–

–

FY26 narrative: The company started FY26 (April 2025) with pent-up order demand from Indian Railways and executed aggressively. Revenue jumped 39%, but EBITDA margin expanded 533 basis points—a sign that either the sales mix shifted up-market (air springs, higher-margin forgings) or execution efficiency improved materially. PAT growth outpaced revenue growth, suggesting operating leverage kicked in. Q4 FY26 (Jan–Mar) revenue was ₹82.54 crore, slightly ahead of Q3’s ₹81.43 crore, indicating the company approached FY27 with a steady run-rate rather than a cliff edge.

Management concall (June 3, 2026): Management cited an order book of “₹300–370 crore” entering FY27 and guided for “around 30% growth also” in FY27 (i.e., ₹500 crore gross). EBITDA margin guidance for FY27 was cautiously conservative: “23–24% definitely, if not 26–28%.” The disclaimer: Railways contracts are fixed-price; raw material inflation (steel, power) creates a lag in margin recovery until new tenders reprice.

5 — Market Expectations & Historical Multiples

This section describes how the market is currently pricing the company and how that compares with its own history and peer group. It is descriptive, not predictive.

Metric

Current

Historical Average (5Yr)

Peer Median (Auto Components)

P/E

28.5x

30.3x

27.4x

EV/EBITDA

20.1x

–

–

ROE

39.9%

25.8%

13.5%

ROCE

50.9%

42%

15.88%

The market currently pays 28.5x earnings, a tick below its own 5-year average of 30.3x and fractionally above the auto-components