Excelsoft Technologies Q3 FY26: ₹710m Revenue, 29% Growth, AI Betting Big While Margins Play Hide & Seek

1. At a Glance – The EdTech Company That Thinks It’s OpenAI’s Cousin

If most IT companies are like roadside dosa stalls—cheap, fast, and easily replicable—Excelsoft is trying very hard to position itself as that one overpriced Mysore café where they serve “AI-powered dosa with blockchain chutney.” And somehow… it’s actually working.

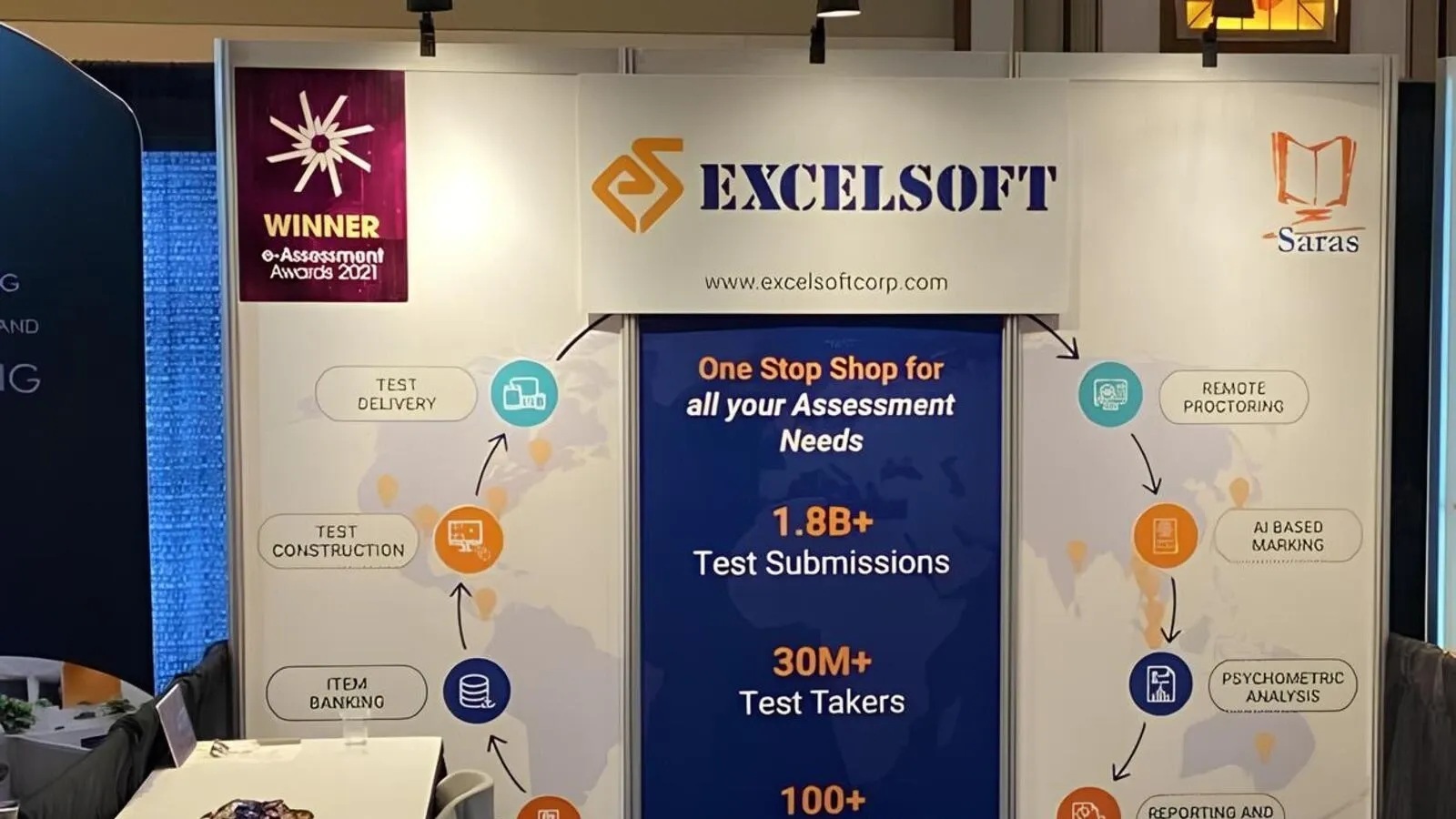

Here’s what we know: this ₹872 crore company is quietly building a niche in digital learning and online assessments, with AI sprinkled on top like masala peanuts at a bar. Revenue is growing, profits are improving, debt is reducing, and management is speaking the language every investor loves right now: “platform-led recurring revenue + AI + global clients.”

But before you get too excited and start imagining this as the next SaaS unicorn, let’s pause.

Margins dipped this quarter. Client concentration is high (top 5 clients = 72% revenue 😳). And management is investing heavily in AI infra like GPUs, which sounds cool—but also expensive.

So the real question is:

👉 Is this a genuine EdTech SaaS evolution story… or just another IT services company wearing AI makeup?

Let’s investigate. Detective mode ON.

2. Introduction – From IT Services to “AI Platform Baba”

Excelsoft started life like most Indian IT companies—doing custom software work, probably building LMS systems while sipping filter coffee in Mysore.