Eureka Forbes Ltd FY26 : Advent’s Blueprint Faces Input Inflation As Net Cash Hits All-Time High Of ₹443 Crore

Section 1 — At a Glance

Eureka Forbes Limited closed the final quarter of fiscal year 2026 by reporting a consolidated revenue from operations of ₹2,710.47 crore for the full year, translating to an 11.33% growth over the previous fiscal year. The institutionalization of the company’s cost of goods sold (COGS) program allowed gross margins to remain structurally resilient at 58.83% , while full-year profit before tax (PBT) reached ₹215.69 crore despite taking a sharp, one-time pre-tax exceptional charge of ₹40.40 crore on account of transition provisions for new labor codes. For the final quarter (Q4 FY26), operations re-accelerated to log a revenue of ₹683.83 crore, expanding by 11.64% year-on-year, demonstrating recovery from structural inventory bottlenecks that had compromised trade velocity in the third quarter.

Investor attention is increasingly drawn to the steady improvement of the business’s internal economics under the professional stewardship of private equity sponsor Advent International, visible through an adjusted EBITDA margin expansion to 13.20% in Q4 FY26. Balance sheet parameters have fundamentally shifted, with the company’s net cash surplus hitting a historic ceiling of ₹443.30 crore, providing immense capital allocation flexibility. However, execution friction remains evident. Operating leverage gains are partially masked by a steep escalation in growth investments, including a 13.18% annual increase in advertising and sales promotion (A&SP) outlays to ₹293.70 crore, and structural capital efficiency metrics like the Return on Capital Employed (ROCE) continue to be dragged down by a bloated balance sheet equity base. The premiumization playbook is working, but it requires continuous capital feeding to defend market share.

Section 2 — Introduction

Eureka Forbes Limited has long stood as a ubiquitous household fixture in the domestic consumer durables landscape, pioneering commercial archetypes in premium consumer care. The corporate trajectory split into a distinct era in July 2022 when global private equity firm Advent International acquired a majority control of 62.56% via Lunolux Limited for an aggregate outlay of ₹4,400 crore, effectively taking the reigns out of the legacy Shapoorji Pallonji Group structure and converting the business into a professionally managed operation governed by an independent board.

This article analyzes the quantitative reality of this turnaround effort following the conclusion of the company’s full fiscal year ended March 31, 2026. With corporate actions expanding beyond traditional vacuum cleaners and water purifiers into complex automated consumer robotics, the operational footprint is changing rapidly. The listing of equity shares on the National Stock Exchange (NSE) in September 2024 has further opened the firm to institutional scrutiny. As management aggressively implements calibrated product portfolio transformations, the financials reveal whether the premiumization strategy is yielding structural cash flow or simply burning through capital to maintain optical growth metrics.

Section 3 — Business Model: WTF Do They Even Do?

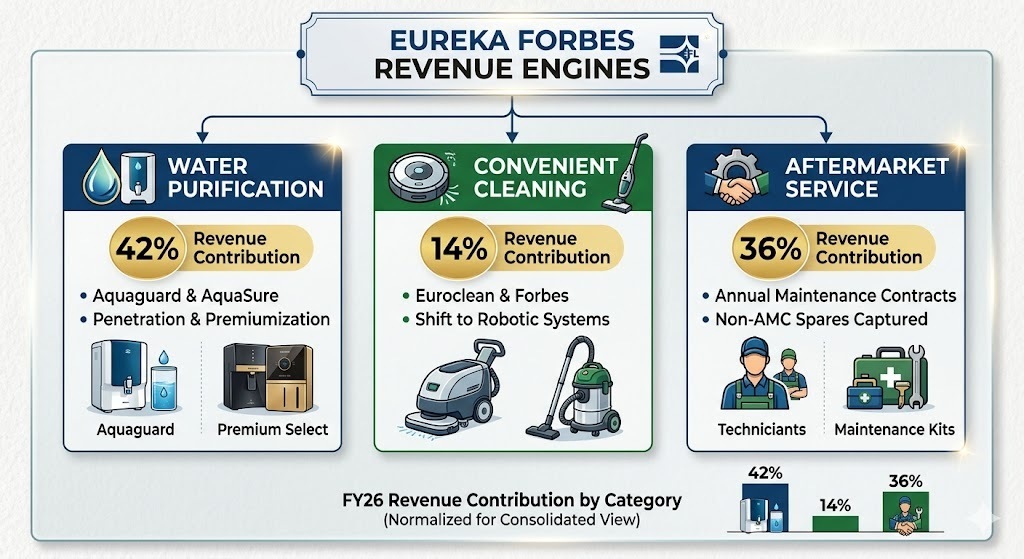

Strip away the marketing vocabulary, and Eureka Forbes is effectively a dual-engine direct-to-consumer (D2C) monetization platform that sells capital hardware to domestic households and then extracts an annuity-style stream of cash via high-margin maintenance services. The operational architecture is split across three pillars: Water Purification (anchored by the flagship Aquaguard and AquaSure brands), Convenient Cleaning (encompassing legacy vacuum lines and newer robotic systems), and the Aftermarket Service framework.

The underlying economic moat is not purely the product technology, but the dense service delivery loop. The firm actively monitors a massive first-party relational database exceeding 14 million active consumers across 19,500 distinct postal codes, deployed through an internal on-ground force of 8,000 field technicians. Water purification infrastructure generates approximately 42% of direct product billings, while the automated service layer contributes a stable 36% of top-line revenues via sticky advance-paid Annual Maintenance Contracts (AMCs). The remainder is driven by vacuum cleaners at 14% and ancillary air-treatment systems. To optimize fixed overheads, the company has ruthlessly rationalized its inventory keeping systems, cutting historical stock-keeping units (SKUs) down from 200 to approximately 80 to eliminate operational redundancies while introducing high-margin variants.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

The locked financial configuration for Eureka Forbes exhibits an acceleration in top-line volumes for the quarter ended March 31, 2026, bouncing back from an inventory correction cycle observed late in the previous calendar year.

Quarterly Performance Comparison

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue from Operations

₹683.83

+11.64%

+5.95%

EBITDA / Operating Profit

₹85.20

+61.79%

+26.34%

Net Profit (PAT)

₹51.09

+139.07%

+467.67%

Reported EPS (₹)

₹2.64

+137.84%

+461.70%

The sharp sequential escalation in net profitability highlights the inherent earnings quality variance seen when trade channel pipelines normalize. Earnings volatility is the tax a business pays for over-relying on concentrated e-commerce channels where inventory backlogs can choke cash generation.

Did Management Walk the Talk?

During the Q3 FY26 concall held in February 2026, management explicitly characterized the third quarter’s deceleration—where