Divgi Torqtransfer Systems March 2026: The 92% Profit Surge and a 295 Crore Cash Cushion

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

Section 1 — At a Glance

Divgi Torqtransfer Systems has staged a dramatic operational turnaround in the financial year ended March 31, 2026. Total revenue from operations rebounded sharply to reach ₹352.89 crore, representing an expansion of 61.2% over the previous fiscal year. This structural recovery was mirrored in the bottom-line performance, where net profits expanded by 92.4% to reach ₹46.93 crore.

Despite this aggressive growth momentum, the company’s capital efficiency metrics continue to signal underlying friction. The return on equity stands at a modest 7.62%, failing to match the velocity of the headline earnings growth.

An overflowing cash chest offers absolute downside protection during macro downturns, but excessive liquidity without immediate productive deployment acts as a structural drag on capital efficiency.

The balance sheet remains heavily weighted toward liquid assets, with cash and bank balances ballooning to ₹294.52 crore—accounting for over 40% of the total asset base. This massive liquidity buffer shields the company from solvency risks but limits active operational leverage. Investors find themselves assessing a business that has effectively de-risked its financial survival but must now demonstrate the capability to convert substantial global order wins into premium capital returns.

Section 2 — Introduction

Divgi Torqtransfer Systems is a specialized automotive component designer and manufacturer that traces its roots back to 1964. The company operates in a highly technical niche, engineering and manufacturing precision drivetrain systems, transfer cases, synchronizers, and electronic gear drives.

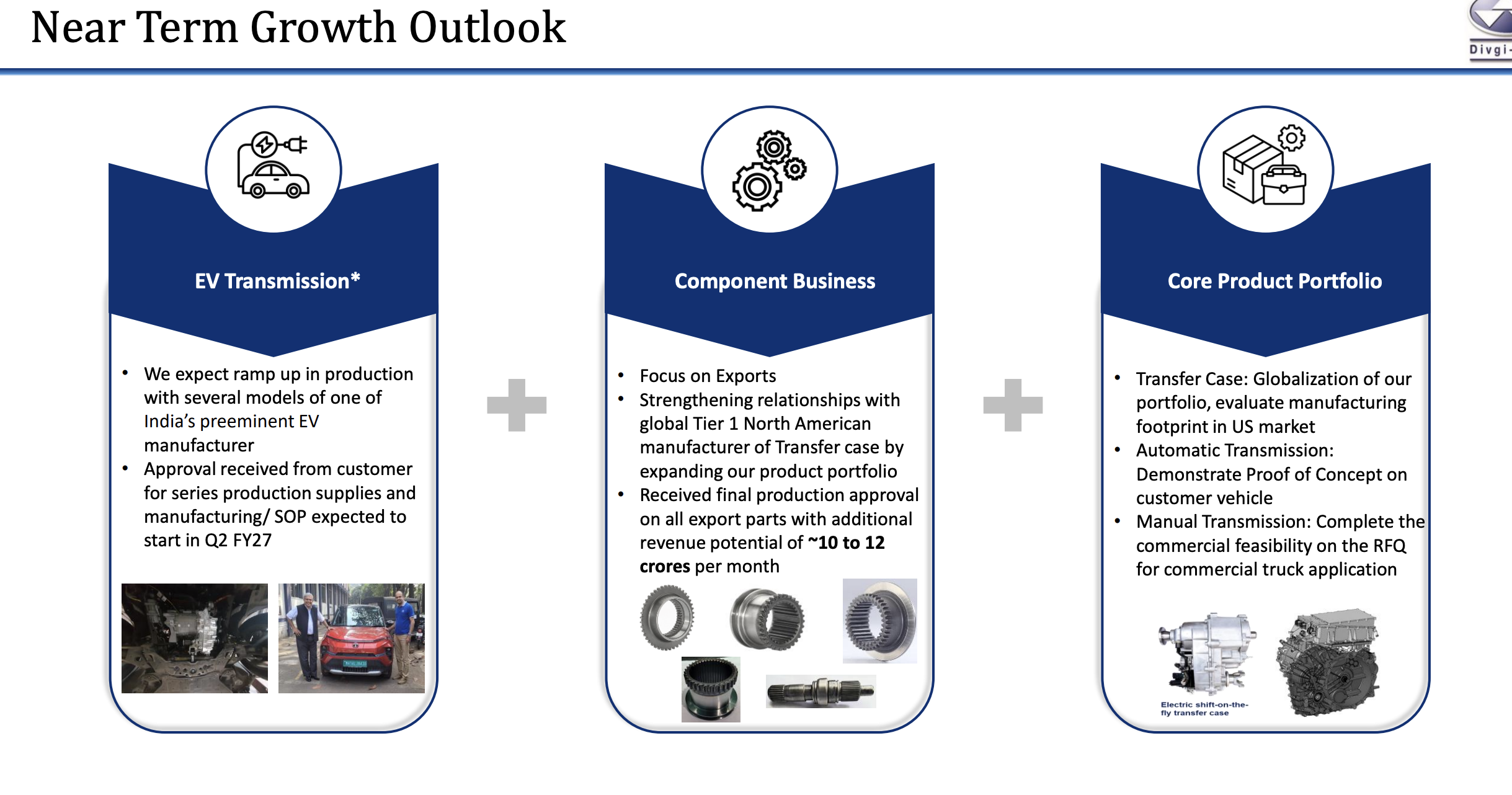

With four manufacturing plants strategically located across Maharashtra and Karnataka, the organization serves as an essential tier-1 supplier to major automotive original equipment manufacturers (OEMs). While legacy internal combustion engine platforms continue to drive the baseline volumes, the company has increasingly oriented its incremental capital expenditure toward electric vehicle transmission assemblies, attempting to position itself at the front end of automotive structural shifts.

Section 3 — Business Model: WTF Do They Even Do?

Divgi essentially builds the mechanical and electronic muscle that prevents your SUV from getting stuck in a ditch when you decide to go off-roading. They specialize in four-wheel-drive transfer cases, synchronizers, and advanced dual-clutch transmission components.

Their revenue mix tells a fascinating story of modern engineering being subsidized by traditional heavy machinery. Transfer cases remain the undisputed anchor of the company, accounting for a massive 50% of segment revenues. Precision components bring in another 29%.

Meanwhile, their highly publicized E-Gear drives—the crown jewel of their futuristic electric vehicle transmission thesis—accounted for a tiny 8% of the mix. In short, while management spends a significant portion of their presentations talking about the electric future, it is old-school, gas-guzzling four-wheel-drive diesel beasts that are actually keeping the lights on in the factories.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Latest Quarter (Mar 2026)

YoY Change (%)

QoQ Change (%)

Revenue

107.62

+84.8%

+18.8%

Operating Profit

21.67

+150.2%

+22.4%

Net Profit

15.48

+189.3%

+31.5%

Reported EPS (₹)

5.06

+189.1%

+31.4%

The final quarter of the fiscal year delivered a dramatic surge across all primary headline metrics. Operating profit growth significantly outpaced revenue expansion, highlighting the material impact of operating leverage as factory utilization moved past structural thresholds.

During recent management interactions, leadership was highly enthusiastic regarding an incremental export program to Indonesia. Under an exclusive arrangement, the company will act as the sole supplier of transfer case systems for 70,000 pickup truck units across the Mahindra Scorpio and Tata Yodha platforms. Management characterized the initial rollout as a “soft ramp from February till June, followed by a flat plateau through December.”

Exclusivity in a single geography shields a supplier from immediate margin erosion, but it simultaneously concentrates structural risk on the client’s localized volume adoption.

Does a massive localized export order justify building out long-term capacity ahead of actual demand?

Section 5 — Valuation Discussion: Fair Value Range Only

To determine where the company sits relative to its intrinsic value, we assess valuation through multiple independent lenses using the full-year reported metrics. The company’s full-year reported EPS stands at ₹15.34.

1. Peer-Linked Price-to-Earnings (P/E) Method

The broader auto-component sector trades across a wide valuation band, with top-tier transmission and drivetrain peers fetching multiples between 35x and 55x. Applying this normalized peer multiple band to