Borosil Ltd March 2026: The ₹429 Crore Mystery Expense That Shattered the Kitchen

Section 1 — At a Glance

Borosil Ltd has served up a highly disruptive fiscal finale for March 2026, where a completely unheralded, monstrous accounting entry has turned a structural sales growth story into a bottom-line crime scene. Top-line momentum remains remarkably resilient, with annual sales climbing 9.7% to cross the four-figure mark at ₹1,195.92 crore, up from ₹1,090.15 crore in the previous fiscal year. However, any optimism surrounding structural volume growth was immediately vaporized by a bizarre, un-itemized “Other Expense” explosion of ₹429.00 crore in the annual numbers. This single line item completely disfigured the operating profitability structure of what has historically been a steady-state consumer brand.

Investors are currently grappling with severe mixed signals. On one hand, the core retail footprint continues to scale up nicely, driven by an accelerating consumer transition from toxic plastics to premium glassware and consumer-ware essentials. On the other hand, the financial quality of those earnings has been heavily compromised by severe margin compression and massive inventory pile-ups. Annual net profit managed a mathematically microscopic growth of 0.57% to land at ₹74.66 crore. This was artificially salvaged only by an aggressive reduction in interest expenses and an unexplained collapse in standard manufacturing cost heads. When a business experiences severe, unexplained cost variations alongside expanding capacities, it usually signals that structural capacity additions are running far ahead of commercial execution efficiency. The core machinery is producing more goods, but the economics of selling them have temporarily broken down. What follows is a forensic investigation into India’s premier glassmaker to see if this kitchenware champion is cracked, or merely undergoing a temporary, high-temperature transition.

Section 2 — Introduction

Borosil Ltd has long enjoyed the status of a household monopoly, synonymous with the very glass containers spinning inside urban Indian microwaves. Yet, the corporate reality behind this kitchen staple has undergone massive structural upheaval over the last 24 months. Having successfully completed the demerger of its scientific and industrial glass division to reposition itself as a pure-play B2C consumer lifestyle vehicle, the company has entered a high-stakes growth phase.

The rationale for evaluating Borosil right now is critical: the stock is currently undergoing a violent valuation adjustment, down 36.4% over the last year, even as management continues to deploy multi-million dollar capital expenditure programs in Rajasthan and Gujarat. With a newly reshuffled C-suite, including the induction of a fresh Chief Executive Officer, the company is attempting to transition from an occasional-use premium glassware seller to an omnipresent, daily-use consumer durables powerhouse. This piece deconstructs the financial mechanics behind this transition, separating genuine brand equity from transactional supply-chain friction.

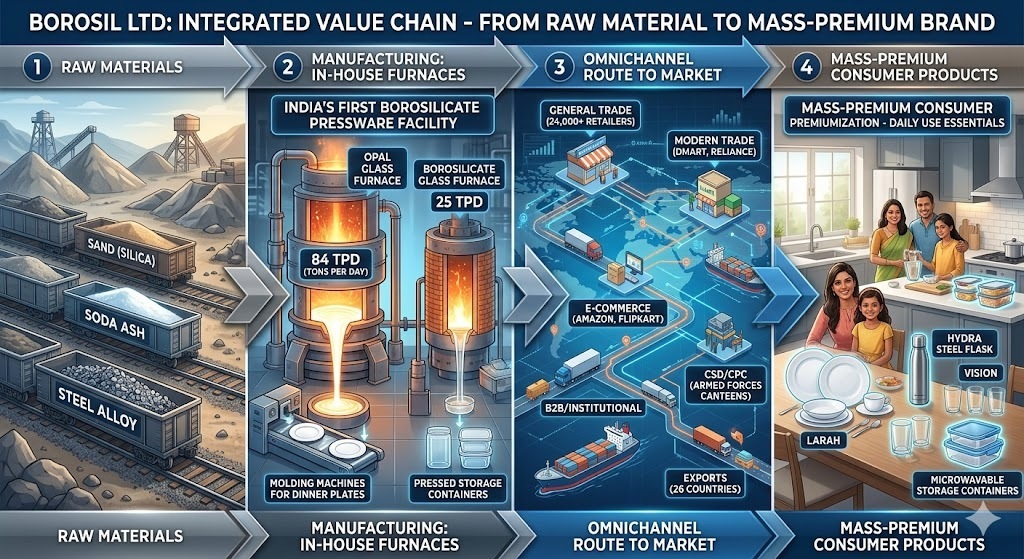

Section 3 — Business Model: WTF Do They Even Do?

Borosil’s business model is fundamentally a premiumization proxy on the Indian kitchen counter. It converts industrial sand and soda ash into high-margin consumer pride across three core pillars: classic Borosilicate Glassware, Larah Opalware dinner sets, and a rapidly expanding Non-Glassware portfolio encompassing domestic appliances and stainless-steel hydration flasks.

The company operates a hybrid manufacturing-cum-trading engine. While it owns massive infrastructure—including an 84 tons-per-day (TPD) opal glass capacity and India’s first 25 TPD borosilicate pressware plant—it aggressively trades in non-glass categories like steel cookware and small appliances. By positioning itself square in the “mass-premium” sweet spot, Borosil avoids the cutthroat, low-margin street fights of unbranded plastics while remaining accessible enough to systematically displace traditional melamine and stainless steel from middle-class dining tables.

The quarterly trajectory illustrates an uncomfortable reality: Borosil’s margins are getting squeezed between regulatory walls and raw material realities. Revenue for March 2026 grew a modest 5.16% YoY to ₹284.12 crore, but operating