Bizotic Commercial Ltd Q2FY26 – When Fast Fashion Meets Faster Valuations: ₹8.38 Cr PAT, 521% Profit Surge, and a P/E Higher Than Most Designer Labels

1. At a Glance

Meet Bizotic Commercial Ltd — the Jaipur-based fast-fashion dream that seems to have swapped tailoring threads for rocket fuel. In Q2FY26 (half year ending September 2025), the company reported revenue of ₹73.78 crore and a net profit of ₹8.38 crore — a sizzling 39.6% jump in sales and 521% surge in profit year-on-year. The market, clearly impressed, dressed up the stock price to ₹899 (as of November 25, 2025), making it a ₹723 crore SME fashion powerhouse.

But wait — the P/E sits at 66.7x, nearly double the industry median (29.4x). That’s like wearing Gucci prices on a Pantaloons product. And yet, the 803% one-year return laughs at all critics, proving that this small-cap tailors’ tale has turned into a multibagger wardrobe essential.

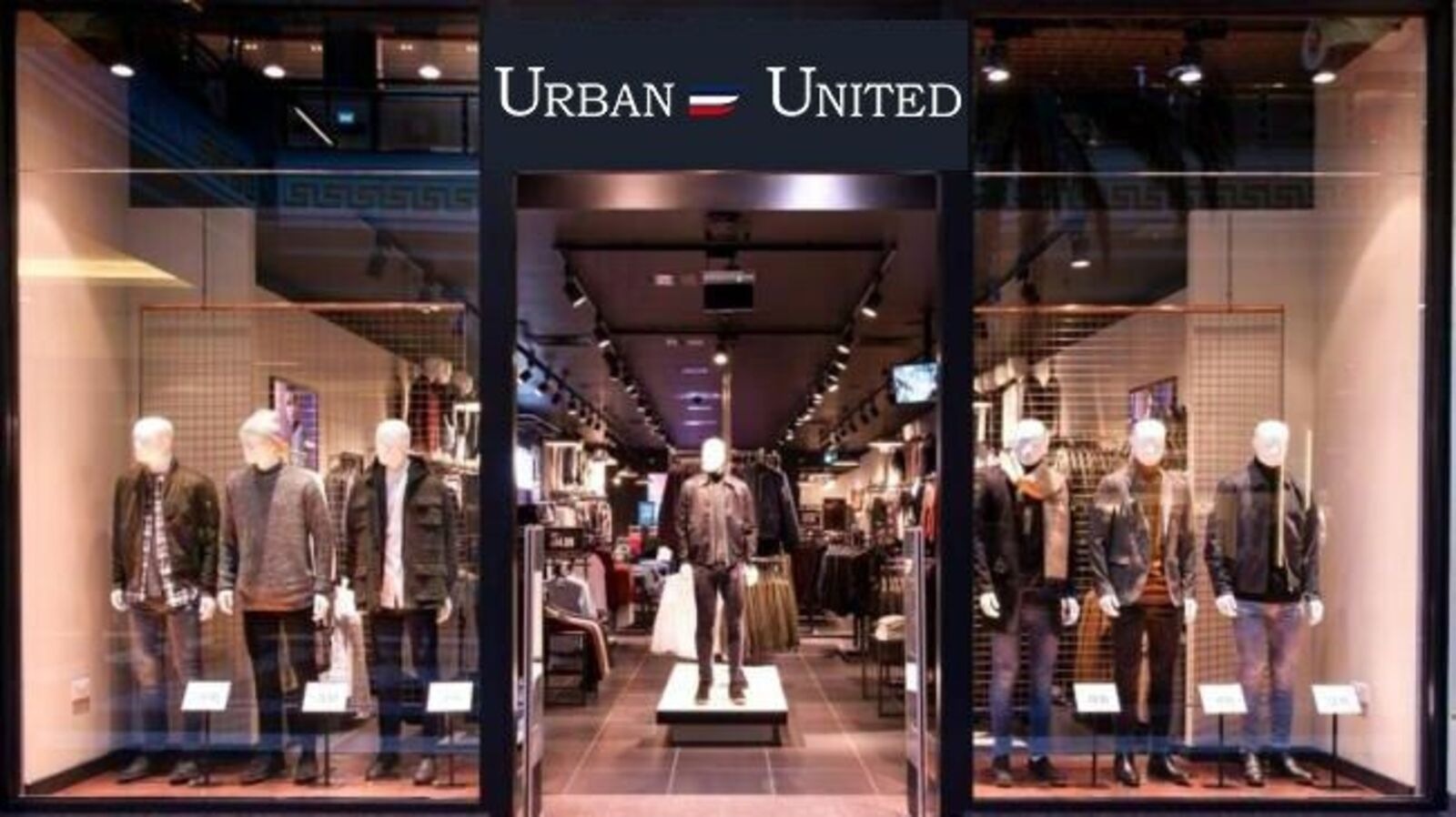

Bizotic runs under the men’s fashion label Urban United, with 21 stores across India (mostly in Rajasthan) and plans to keep opening new ones faster than Indian weddings happen in November. With ROCE at 11.4%, ROE at 7.6%, and Debt to Equity at just 0.13, the financial stitching looks tight — though the margins need better ironing.

If you blinked during FY24–FY25, you probably missed this company’s Cinderella transformation from ₹8 crore sales in FY19 to ₹132 crore TTM — a fashion startup to listed entity leap that even Shark Tank would find overdressed.

2. Introduction

What happens when you mix Rajasthan’s textile DNA with startup-era Instagram energy? You get Bizotic Commercial Ltd, a company that manufactures, trades, and sells men’s garments but markets them with the flair of a Bollywood stylist on a sugar rush.

Founded in 2016, Bizotic started as a small trading business, quietly dealing in fabrics and wholesale garments. Fast-forward to FY25, and it’s become a ₹132 crore sales story with its brand Urban United plastered across city malls and e-commerce listings.

The company designs, markets, and retails menswear across every mood swing: formal, casual, party, ethnic, fit, comfort, and even “winter wear” (for people who still believe Rajasthan gets cold). The brand currently operates 20 stores in Rajasthan and one in Bihar, mostly on franchisee models — a smart way to expand without bleeding cash like most apparel startups.

But here’s the twist — despite all this glamour, Bizotic isn’t shy about its humble structure. It outsources manufacturing to third-party job workers, handling design, quality, and packaging in-house. In short, it’s a fashion orchestrator, not a factory-heavy behemoth.

And investors love the melody — because while competitors like Lux, Arvind, and Gokaldas are grinding through global headwinds, this ₹723 crore SME just pulled off a 520% profit jump. Who knew a Jaipur fashion brand could outpace even influencer growth rates?

3. Business Model – WTF Do They Even Do?

Bizotic’s playbook is simple but stylish: design locally, outsource efficiently, sell aggressively. Under its flagship brand Urban United, it curates a full wardrobe for men — from formal shirts to party jackets, from “ethnic wear for shaadis” to “comfort wear for hangovers.”

The process works like this: Bizotic finalizes the design and fabric specs, sends them to third-party job workers for production, and handles quality inspection, finishing, and distribution in-house. Think of it as Zara’s fast-fashion model, but executed in Jaipur’s industrial bylanes with desi cost control.

Here’s where it gets smarter — 17 out of 21 stores are franchisee-owned. That means the company takes a security deposit, supplies merchandise, and gets brand reach without the headache of rent and staff costs. This keeps capital expenditure light and scalability high.

It’s also a fabric trader, selling cloth material wholesale and retail. So even if apparel demand slows, the company’s trading leg cushions the P&L.

Revenue mix (FY24):

94% from product sales (the core business)

3% from sundry write-offs

2% from capital gains

1% from interest income

A neat structure, though one wonders — when 94% comes from selling shirts, is the 6% “extra income” their version of accessorizing?

4. Financials Overview

Source table

Metric

Latest Qtr (Sep 2025)

YoY Qtr (Sep 2024)

Prev Qtr (Mar 2025)

YoY %

QoQ %

Revenue (₹ Cr)

73.8

52.9

58.0

39.6%

27.2%

EBITDA (₹ Cr)

12.0

2.0

4.0

500%

200%

PAT (₹ Cr)

8.38

1.35

2.06

521%

306%

EPS (₹)

10.42

1.68

3.05

520%

242%

Annualised EPS = ₹10.42 × 2 = ₹20.84 (since these are half-yearly numbers).

At ₹899 per share, the P/E = 899 / 20.84 = 43.1x (annualised) — though the screener quotes 66.7x on trailing earnings, which suggests FY25 was still warming up.

Commentary: From ₹1 crore profit in FY22 to ₹8 crore in H1FY26 — that’s a glow-up Bollywood makeup artists would envy. The EBITDA margin has climbed from a patchy 2–6% range to a solid 16%, hinting that Urban United’s pricing power is finally