BIGBLOC Construction FY26: Chasing Volume, Losing Margin

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Revenue surged 26% to ₹283 crore in FY26, but the bottom line fell ₹32 crore into red. The company manufactured 8.27 lakh cubic meters of AAC blocks—up 37% year-on-year—yet the financial engine sputtered. Margins compressed from 13% EBITDA (FY25) to 6.2% (FY26) as raw material inflation and labor disruptions overwhelmed pricing discipline. The balance sheet swallowed ₹202 crore in debt against equity of just ₹137 crore (₹28 crore capital + ₹109 crore reserves).

A 78% capacity utilization rate in Q4 looks respectable; six quarters back it was 53%. Yet profit per unit sold has cratered. Two new businesses—AAC wall panels and construction chemicals—are meant to heal this eventually, but they’re not profitable yet.

The company faces the odd tension: volume is working, but profitability is not. Can higher utilization fix it, or has the model fundamentally broken?

2. Introduction

BigBloc Construction Ltd, incorporated in 2015, manufactures and sells AAC (Aerated Autoclave Concrete) blocks and related products. The stock trades at ₹49.71 as of 9 June 2026 (not live), valuing the company at ₹704 crore.

FY26 ended 31 March 2026 with a net loss of ₹1.76 crore, a sharp reversal from FY25’s ₹30.9 crore profit. This happened despite revenues growing from ₹224 crore to ₹283 crore. The operating profit (EBITDA before interest, tax, depreciation) halved from ₹30 crore to ₹18 crore.

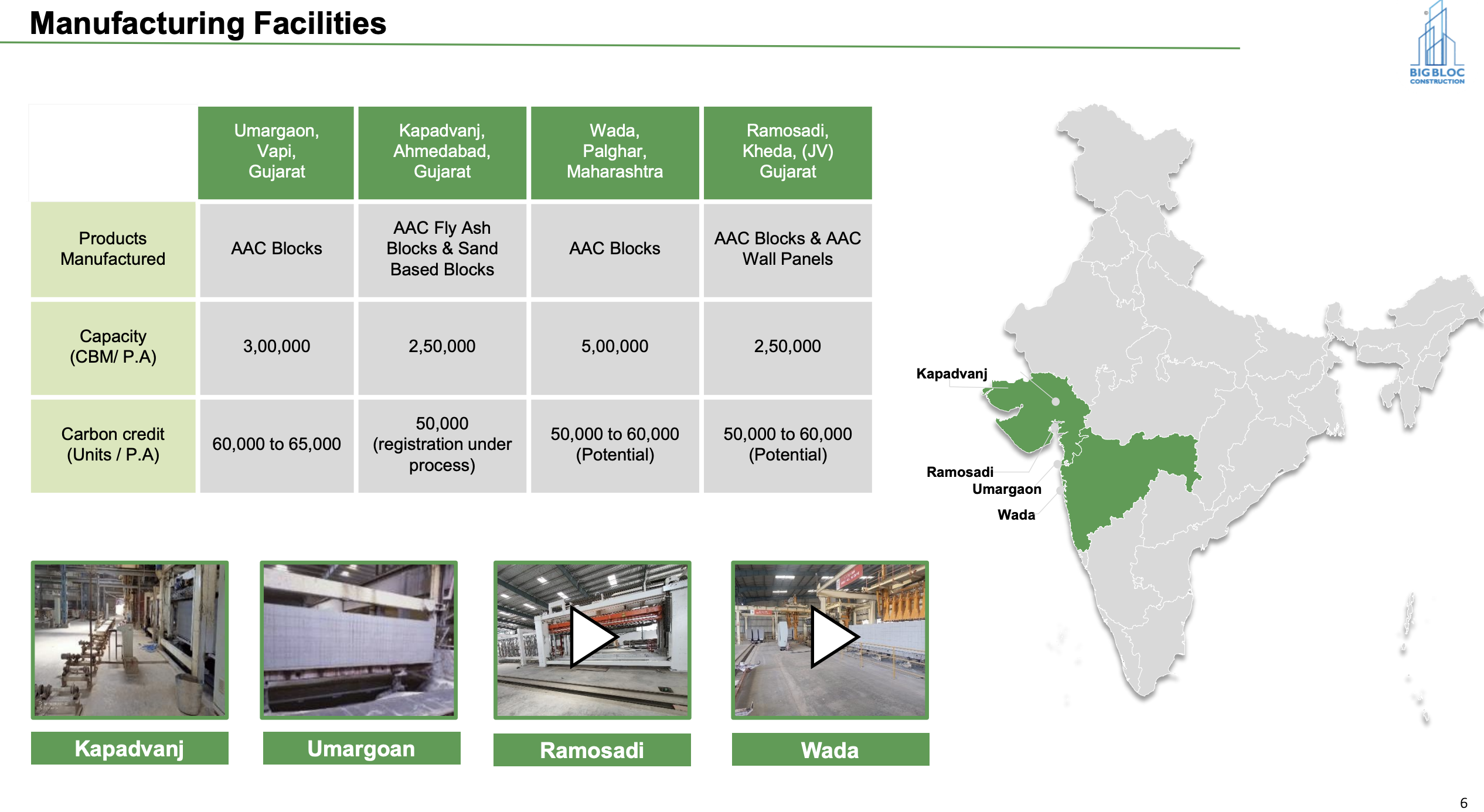

The company has four manufacturing plants: Vapi (capacity 3 lakh CBM), Ahmedabad (2.5 lakh), Wada (5 lakh), and Ramosadi (2.5 lakh). A fifth unit is a 50-50 joint venture with Siam Cement Thailand at 2.5 lakh CBM capacity. In April 2025, a subsidiary acquired land in Madhya Pradesh for a greenfield facility aimed at Central India.

3. Business Model: WTF Do They Even Do?

BigBloc makes two families of products: AAC blocks (the bulk, ~83% of FY25 sales) and AAC wall panels. It also trades in mortars and plasters under the NXTFIX and NXTPLAST brands, and since May 2026, operates a construction chemicals plant at Umargaon.

AAC blocks are lightweight, non-load-bearing masonry units made from fly ash, cement, and lime. They’re expensive per unit versus red bricks but require fewer units per wall, less labor, and (management claims) better crack resistance if installed properly. The blocks are bulky—effective distribution radius ~300–350 km—so geography matters.

Wall panels are longer-span products (8–20 feet), carry 30–45% EBITDA margins (against 8–10% for blocks), but adoption is slower than management hoped. This product mix shift is supposed to rescue margins eventually.

The company supplies 100+ real estate developers, construction firms, and corporates. Customer concentration is strict: no single client exceeds 3% of sales. The distribution mix in 9M FY26 was 56% via dealers, 30% to builders/contractors, and 14% to corporates like L&T, Adani, and Prestige.

The sequential margin bridge (per management commentary in May 2026 concall): input cost inflation (~5–6% on raw material and fuel, partly blamed on US–Iran geopolitics) and labor shortage (Western India, around Holi and elections in Q3–Q4) prevented immediate price pass-through. Selling prices in Q4 were “almost similar as compared to Q3,” meaning cost headwinds bit into EBITDA.

5. Valuation Discussion: Fair Value Range (Educational Only)

What follows is a walkthrough of how three valuation methods work, using this company’s numbers as the example — not a target, not a forecast, not advice.

Method 1 (P/E): Annualised EPS for FY26 is ₹-0.12 (a loss). The peer band (Ambuja, ACC, Shree Cement, J K Cements, Dalmia Bharat) trades at 11.7x to 48.7x