Batliboi Ltd Mar 2026: The ₹593 Cr Backlog Mirage and the Non-Cooperative Credit Reality

At a Glance

Batliboi Ltd entering FY27 presents an intense paradox of operational optimism and deep financial distress signals. Headline revenue for FY26 closed at ₹440.43 crore, a modest 6.66% year-on-year increase from ₹412.94 crore in the preceding fiscal. On the surface, the company boasts a historic high order backlog of ₹593 crore, driven by a blistering order inflow of ~₹988 crore during the year. This operational momentum implies deep demand visibility in its core machine tools, air engineering, and newly integrated environmental engineering segments.

However, a serious divergence appears in the statutory profitability and credit profile. Consolidated net profit crashed by 57.89% to just ₹5.68 crore in FY26, down from ₹13.49 crore in FY25, weighed down by an exceptional provision of ₹7.49 crore and rising structural overheads. Even more alarming for public market participants is the complete freeze in institutional credit relationships.

On February 27, 2026, CRISIL Ratings finalized a rating action maintaining the company’s bank loan facilities at ‘CRISIL C’ and ‘CRISIL A4’ with a explicit ‘ISSUER NOT COOPERATING’ tag. The credit rating agency cited absolute non-cooperation from management and a continuous failure to submit mandatory No Default Statements (NDS) for three consecutive months. While the investor desk highlights structural macro tailwinds and a path to debt-free overseas operations, the compliance framework paints a much more urgent reality.

Capital efficiency cannot be falsified by a large order book when the banking system treats the underlying entity as a dark box.

Introduction

Batliboi Ltd is a veteran of industrial India, tracing its lineage back to 1892. Over its century-and-a-half existence, the company has transitioned from a pure-play trading agency into a highly diversified manufacturer and distributor of capital goods. Operating out of its primary domestic manufacturing hub in Surat and an overseas manufacturing base in Canada via its step-down subsidiary Quickmill Inc, the company targets highly cyclical downstream sectors.

Historically known for keeping its head down through long capital goods recessions, Batliboi has recently attempted a structural transformation. The corporate narrative is built around two pillars: expanding its heavy industrial footprint and aggressively integrating its sister concerns—most notably the amalgamation of Batliboi Environmental Engineering Limited (BEEL) to present a larger, greener balance sheet to the street.

Business Model: WTF Do They Even Do?

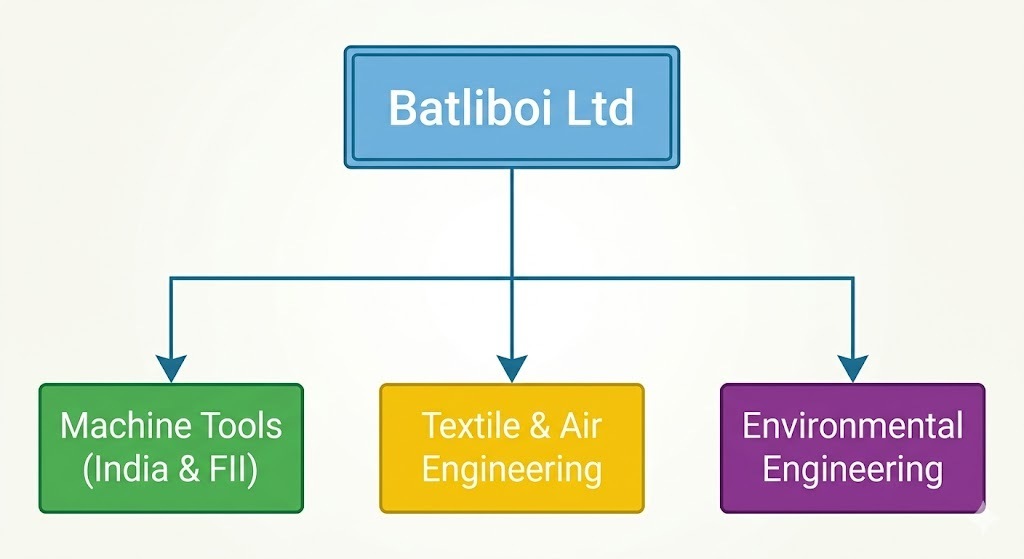

Batliboi operates a corporate structure that resembles a legacy industrial flea market. Rather than dominating a single precise niche, it splits its attention across three separate, operationally distinct silos.

Machine Tools (Manufacturing & Agencies): They build conventional and CNC milling, drilling, and turning machines in India and Canada, selling them to automotive and defense heavyweights. When they aren’t manufacturing them, they act as brokers—selling massive foreign-built metal-forming systems on commission.

Textile & Air Engineering: This segment sells massive air humidification and waste collection systems to spinning and knitting mills. They also double as commissioning agents for European textile hardware, meaning their fortunes are entirely linked to the financial health of garment exporters.

Environmental Engineering (The New Horizon): Post-merger, they now sell industrial fans, de-dusting systems, and effluent water treatment plants to solar manufacturers and steel plants.

Essentially, they act as an outsourced engineering floor and a sales agent wrapped into one. The business model relies heavily on working capital velocity—buying raw metal, engineering it into heavy machinery, and hoping the client pays before the inventory cycle ages out.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

₹125.63

+8.80%

+1.05%

EBITDA / Operating Profit

₹6.76

+23.36%

-4.52%

PAT

₹5.02

+180.45%

+304.07%

EPS (Reported)

₹1.07

+72.58%

+305.77%

Data compiled from Quarters and Profit & Loss blocks.

The multi-quarter trend demonstrates extreme volatility. While March 2026 showed a spectacular bounce-back in quarterly net profit to ₹5.02 crore compared to the immediate losses of the preceding quarters, the aggregate full-year performance tells a far more sobering story.