ATV Projects India Ltd Mar 2026 : Profit of ₹7.16 Crore on Sub-Scale Sales of ₹67.65 Crore

Section 1 — At a Glance

ATV Projects India Ltd closed its fiscal year 2026 with a profit after tax of ₹7.16 crore, down from ₹7.40 crore in the prior fiscal year, even as annual sales dropped by 4.14% to ₹67.65 crore. While the company managed to post an operating profit of ₹8.18 crore due to lower base expenses in certain buckets, structural inefficiencies continue to restrict meaningful expansion.

Investor attention remains anchored to its deep asset value, notably a recently approved memorandum of understanding (MoU) to develop 3.29 acres of surplus land in Mathura under a 50:50 profit-sharing structure valued at ₹47.75 crore. However, significant worries prevent institutional enthusiasm: promoter shareholding is remarkably low at 26.89%, its Thermoplastic Elastomers (TPE) plant remains completely non-functional, and the return on equity stays locked at a weak 3.42%.

Operating margins can fluctuate wildly when a business handles major fabrication contracts on a small scale, as raw material movements dictate short-term outcomes. Profitability without a matching operational scale is an accounting trophy, not a commercial moat. This report evaluates whether its real estate assets can offset its weak engineering run-rate.

Section 2 — Introduction

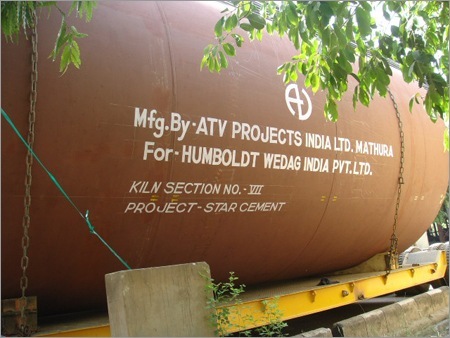

ATV Projects India Ltd, established in 1987, occupies a peculiar corner of the Indian industrial manufacturing ecosystem. Operating primarily out of its manufacturing unit near Mathura, the company renders project management, engineering services, and critical equipment fabrication for capital-intensive sectors like sugar, petrochemicals, fertilizers, and power.

The company is currently at a critical junction. It has spent years operating far below its structural capacity while holding legacy real estate and significant borrowings from financial institutions. With recent regulatory approvals allowing the company to liquidate or develop portions of its surplus land holdings, the investment thesis is transitioning from a core engineering turnaround story to an asset-monetization play.

Section 3 — Business Model: WTF Do They Even Do?

ATV Projects functions as a heavy engineering fabricator that builds massive industrial equipment. For the sugar industry, it manufactures energy-efficient mills and bagasse-fired boilers; for non-sugar clients, it builds spherical storage tanks (Horton Spheres), pressure vessels, heat exchangers, and chemical reactors.

The operations can be categorized as a customized job-work model. It relies on heavy procurement and detailed engineering to deliver individual large-scale orders rather than standardized manufacturing. Financially, this means extended manufacturing cycles and deep inventory commitments. To make matters more complicated, its high-tech Thermoplastic Elastomers (TPE) plant is entirely idle, leaving the company heavily reliant on traditional heavy engineering supplies and scrap or land monetization to keep its head above water.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

Comparison Table

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

20.10

17.78

18.35

EBITDA / Operating Profit

2.37

2.23

1.88

PAT

2.06

2.57

1.61

EPS (₹)

0.39

0.48

0.30

(Note: Data sourced from quarterly tables; EPS is not annualised ).

The quarterly trajectory illustrates an improved operational performance in terms of absolute top-line delivery, with March 2026 revenue hitting ₹20.10 crore. Operating profit ticked up to ₹2.37 crore. However, the net profit of ₹2.06 crore was lower than the March 2025 profit of ₹2.57 crore, which had been aided by higher other income elements.

When a business lacks revenue scale, quarterly financial trends reflect