Atal Realtech Ltd Q2 FY26 – ₹19.7 Cr Revenue, EPS ₹0.09, but 99× P/E: Government Contractor or Market’s Optical Illusion?

1. At a Glance – “Small Contractor, Big Valuation, Bigger Questions”

Atal Realtech Limited is that classic Indian SME stock which looks like a polite government contractor on paper but trades like it’s secretly building airports on Mars. With a market capitalisation of about ₹318 crore and a current price hovering near ₹25.7, the stock has delivered an eye-popping ~81% return over one year, while quietly reporting quarterly revenue of ₹19.7 crore and quarterly PAT of ₹1.04 crore. The result? A headline P/E of nearly 99×, which for a civil contractor sounds less like valuation and more like fiction writing.

ROCE is around 10.8%, ROE near 6.7%, debt-to-equity a modest 0.24, and operating margins fluctuate like a monsoon-dependent irrigation project. The latest quarter saw sales decline YoY and QoQ, profits fall faster than promoter holding, and yet the stock refuses to behave like a boring contractor. Is the market seeing future order book fireworks, or is this just another case of “SME mein momentum, logic later”? Before you decide, grab some chai, because this contractor has more corporate actions than an average Bollywood script.

2. Introduction – Welcome to the Government Tender Multiverse

Atal Realtech Limited was incorporated in 2012, which means it has survived more policy changes, tender delays, and payment cycles than most startups survive funding winters. The company operates in civil construction and government contracting — the kind of business where patience is a skill, cash flow is a suggestion, and receivables are more philosophical than financial.

Listed on NSE Emerge in October 2020, Atal Realtech entered the markets promising exposure to infrastructure development without the scale headaches of mega EPC giants. Roads, bridges, water supply, drainage, irrigation, stadiums, government buildings — basically anything that requires concrete, approvals, and endless paperwork.

But here’s the twist. Despite operating in a low-margin, working-capital-heavy business, the stock market currently values Atal Realtech like it has discovered a new construction material made of gold dust. The company is profitable, yes. It is growing over the long term, yes. But does that justify a near-triple-digit P/E when industry averages sit near one-third of that? Or is this a classic case of “float kam hai, imagination zyada”?

Before forming opinions, let’s actually understand what the company does, how the numbers look, and where the red flags and green shoots coexist uncomfortably.

3. Business Model – WTF Do They Even Build?

Atal Realtech is an integrated civil construction contractor. In simpler terms: they take government and institutional contracts, arrange design and planning, procure materials, execute construction, and hand over the project — ideally before the next election cycle.

Their services fall into three buckets:

Project management: end-to-end execution of civil and industrial construction projects. Construction services: actual on-ground building — roads, bridges, irrigation works, buildings. Engineering services: subcontracting structural and infrastructure work.

The company is registered as a Class I-A contractor with the Maharashtra PWD, which is basically the contractor equivalent of a VIP pass — it allows them to bid for larger and more complex government projects.

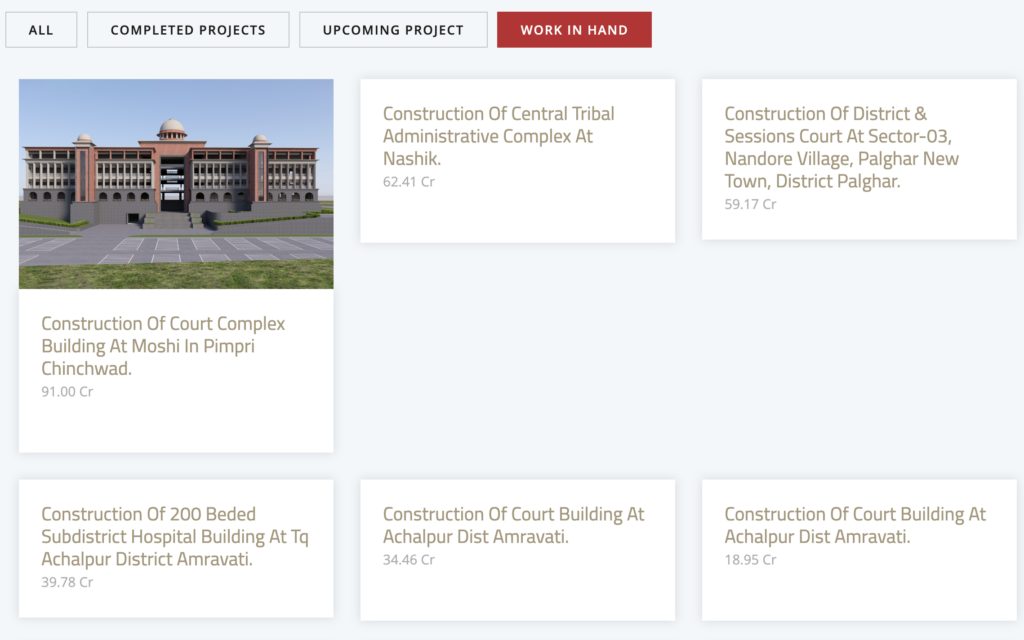

Projects undertaken include collector office buildings, district courts, government rest houses, malls, housing projects, and educational complexes. No fancy luxury branding here — this is pure “sarkari kaam”, with all its pros (steady demand) and cons (slow payments).

Revenue is almost entirely from contract receipts. No asset-light SaaS dreams, no recurring subscription fantasies — just concrete, steel, labour, and bills raised to government departments.

So the business model is clear, understandable, and boring. Which raises the obvious question: why is the valuation not boring at all?