ASK Automotive FY26: The 50% Market Leader Chokes Out Low-Value Assemblies as EPS Marches to ₹15.08

Section 1 — At a Glance

ASK Automotive Limited closed the fiscal year ending March 31, 2026, on an emphatically strong footing, solidifying its dominant position with a massive 50% market share in the domestic two-wheeler advanced braking systems landscape. Headline operational expansion took center stage as full-year revenue from operations grew to ₹4,176.32 crore, up from ₹3,600.83 crore in the preceding fiscal. This volume-led expansion trickled cleanly down the financial funnel, yielding an annual consolidated Net Profit of ₹297.32 crore. The top-line momentum trickled directly to shareholders, elevating reported full-year Earnings Per Share (EPS) to ₹15.08, up from ₹12.56 in FY25.

What continues to pull investor gravity is the management’s tactical maneuvering of its business mix. The company has aggressively and deliberately downscaled its low-margin wheel assembly business, which contracted by 46% during the year, effectively driving automated operational efficiencies across higher-value core segments. However, this expansionary velocity has not come without structural trade-offs. Raw material dynamics—particularly volatile aluminum prices that function on a month-on-month contractual pass-through mechanism—have induced an artificial denominator contraction, slightly shaving percentage-based margins despite strong absolute EBITDA expansion. Furthermore, the company’s capital allocation has pivoted heavily into aggressive greenfield rollouts across Rajasthan and Bengaluru, sending capital work-in-progress (CWIP) soaring to ₹148.15 crore. Corporate governance and leadership structural changes also introduced noise during the year, highlighted by the resignation of CEO Shalender Singh Birla and President Prashant Kumar Gupta. High capital intensity breeds short-term operational friction before yielding economies of scale.

Section 2 — Introduction

ASK Automotive Limited enters the 2026 financial discourse as an industrial heavyweight navigating a vital structural transition. Historically anchored as the primary go-to friction material and advanced braking supplier to top-tier two-wheeler Internal Combustion Engine (ICE) giants like Hero MotoCorp, Honda, TVS, and Suzuki, the company is systematically rewiring its manufacturing core. This structural repositioning is precisely why the stock commands an eye-watering market valuation of ₹8,975.90 crore at a snapshot current market price of ₹455.30.

The auto-component game is inherently punitive to companies that over-rely on a single client or vintage propulsion systems. Understanding this vulnerability, ASK has spent the last 18 months deploying multi-segment diversifications across safety control cables and aluminum lightweighting precision solutions. With a footprint spanning 18 state-of-the-art manufacturing facilities, the company is transitioning from a localized components provider into a global, powertrain-agnostic systems architect. This deep dive unpacks whether ASK’s capital-heavy bets will construct an impenetrable competitive moat or simply dilute its historically high capital efficiency metrics.

Section 3 — Business Model: WTF Do They Even Do?

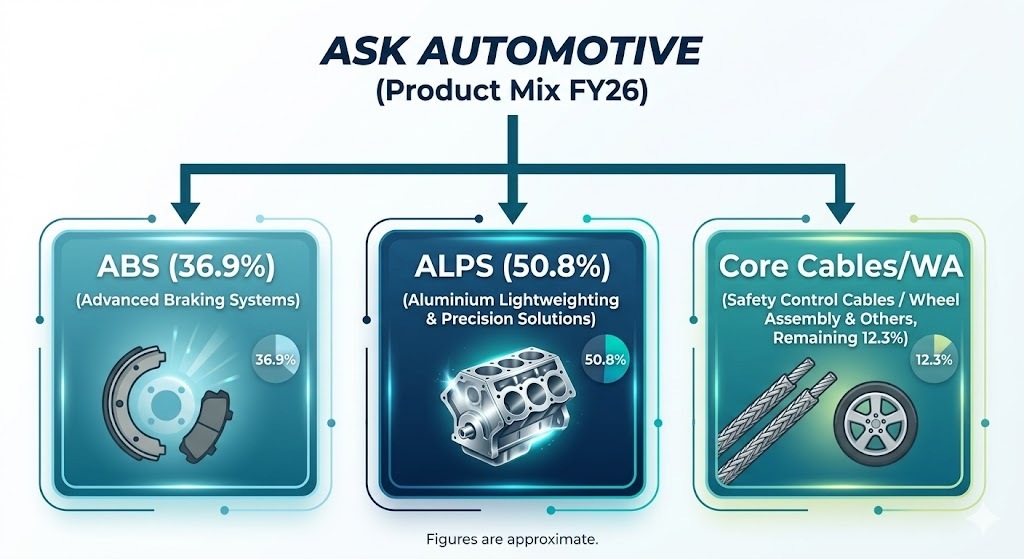

At its architectural core, ASK Automotive converts heavy metallurgical and chemical inputs into high-stakes safety and thermal management components. They function via three primary, powertrain-agnostic verticals: Advanced Braking Systems (ABS), Aluminium Lightweighting Precision Solutions (ALPS), and Safety Control Cables (SCC). If it stops a bike, sheds engine heat, or flexes a mechanical boundary on an Indian two-wheeler, there is a literal 50% probability it rolled out of an ASK foundry.

The revenue architecture has experienced a major tectonic shift: ALPS has officially overtaken braking as the largest segment, capturing 50.8% of the mix in FY26, driven by intense lightweighting demand from both ICE and Electric Vehicle (EV) original equipment manufacturers (OEMs). The business relies heavily on an integrated design-to-delivery model, utilizing proprietary material formulations and in-house tool rooms. Geographically, domestic markets swallow 95.5% of production, leaving international markets at a modest 4.5% across 14 export countries. They sell safety, but more importantly, they sell deep logistics integration via just-in-time (JIT) supply chains that auto OEMs simply cannot afford to disrupt.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

The locked evaluation parameters confirm that the company reports on a strict QUARTERLY filing frequency, with standalone and consolidated disclosures synchronizing flawlessly across long-term reporting intervals.

Metric

Latest Quarter (Mar 2026)

YoY

QoQ

Revenue

₹1,147.12

+35.01%

+5.80%

EBITDA / Operating Profit

₹132.44

+27.57%

-6.02%

PAT

₹71.54

+24.18%

-10.49%

EPS

₹3.63

+24.32%

-10.37%

Data Source: Compiled from quarterly tables. YoY matches Screener headline variances.

While the year-on-year revenue trajectory showcases an exceptional 35.01% blast radius, the sequential (QoQ) metrics tell a tale of short-term margin compression, with PAT