Aeron Composites FY26: The ₹211 Crore Asset Pivot that Left Earnings in the Dust

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

1. At a Glance

The financial year 2026 has marked a structural inflection point for Aeron Composites Ltd, defined by an aggressive transition from an asset-light, rented setup to a fully owned, scaled manufacturing model. While the long-term strategic foundation has been expanded significantly, the immediate financial outcome reflects severe execution friction. Total revenue for FY26 crept forward marginally to ₹221.84 crore, representing a muted 3.03% annual expansion relative to the ₹215.31 crore recorded in FY25. This structural stagnation stands in stark contrast to the company’s historical five-year compounded sales growth of 23%.

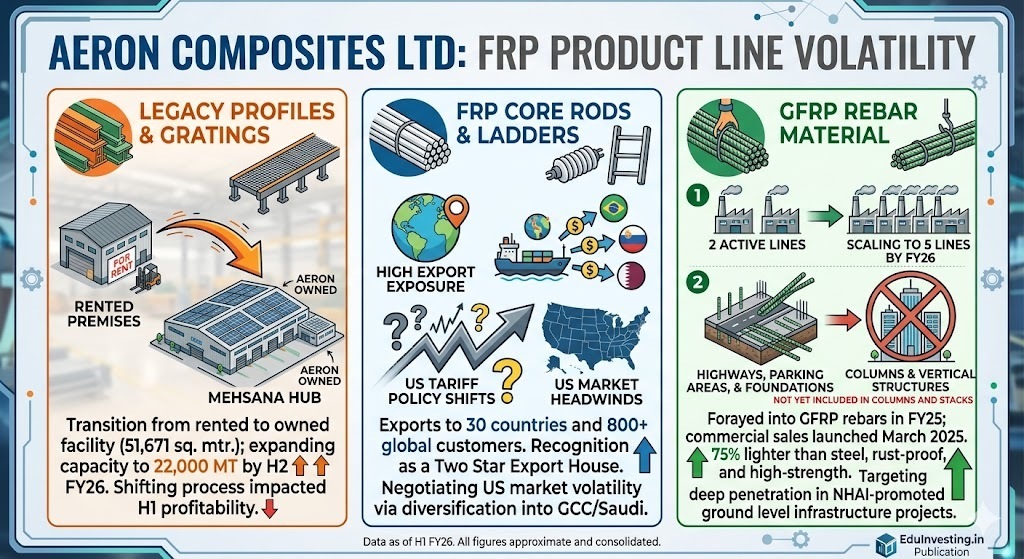

The primary operational pressure manifested in net profitability, which dropped sharply by 34.6% to ₹8.72 crore down from ₹13.34 crore in the preceding fiscal year. This compression was driven by severe operational inefficiencies encountered during the relocation of pultrusion manufacturing lines to the newly commissioned 51,671 square meter facility in Mehsana, Gujarat.

Investor concern is focused on capital efficiency, as the company’s Return on Capital Employed (ROCE) collapsed from 21% in FY25 to a mere 9.77% in FY26. This deterioration stems from a massive expansion of the asset base, with property, plant, and equipment skyrocketing from ₹19.54 crore to ₹76.32 crore, which has outpaced near-term output. The core question facing investors is whether the temporary sacrifice of near-term margins will successfully clear the path for management’s stated target of reaching ₹300 crore in revenue by FY27.

2. Introduction

Aeron Composites operates within the niche industrial architecture space, functioning as an integrated manufacturer of Fiber Glass Reinforced Polymer (FRP) products. Its portfolio encompasses cable trays, structural profiles, handrails, ladders, and molded gratings. These products serve as specialized alternatives to traditional steel and aluminum components across corrosion-heavy environments like chemical processing plants, wastewater treatment utilities, and coastal public infrastructure.

The operational narrative of FY26 was defined entirely by the commissioning of the Mehsana plant. Completed at the end of September 2025, the consolidation of pultrusion lines into this single owned location was designed to unlock long-term scale. However, moving complex industrial machinery while attempting to sustain delivery timelines is a difficult operational challenge. The disruption severely constrained H2 production windows, driving down capacity utilization and resulting in missed delivery targets. Consequently, the company enters the back half of 2026 racing to stabilize its operating metrics before its expanded capacity becomes an expensive overhead burden.

3. Business Model: WTF Do They Even Do?

Aeron Composites essentially takes industrial plastics, reinforces them with glass fibers, and convinces global engineers that steel is an outdated material. The core product line relies on pultrusion—a continuous manufacturing process that pulls raw fibers through heated dies to create structural beams, handrails, and cable trays that are rust-proof, non-conductive, and significantly lighter than traditional metals.

The commercial strategy targets two primary growth vectors:

The Structural Portfolio: Supplying infrastructure heavyweights like Adani, Reliance Industries, and L&T for applications in corrosive coastal or industrial settings.

New Material Formats: Launching Glass Fiber Reinforced Polymer (GFRP) rebars as direct steel substitutes in civil engineering projects, highly promoted by infrastructure bodies like NHAI.

Financially, the mix presents a structural challenge. While the company operates as a recognized “Two Star Export House” shipping 55% of its volume to 39 countries, this heavy export tilt introduces geopolitical risks. The remaining 45% domestic business is cyclical and tied to major infrastructure capex. This business model delivers strong returns when utilization is high, but becomes problematic when factory floors are quiet.

4. Financials Overview

Figures are consolidated, in ₹ crore. (Note: Aeron Composites reports standalone audited figures to the exchange as its primary operational basis, which are detailed below) .

Half-Yearly Financial Velocity

Metric

Latest Half (H2 FY26)

YoY (H2 FY25)

Previous Half (H1 FY26)

Revenue

₹103.01

₹108.59

₹118.83

EBITDA / Operating Profit

₹8.00

₹8.00

₹10.00

PAT

₹1.48

₹6.69

₹7.23

EPS (₹)

₹0.87

₹3.91

₹4.25

Concall Performance: Walk the Talk

During the November 2025 interaction, management projected confidence regarding a margin recovery in H2 FY26. The actual results show a different reality. H2 FY26 revenue contracted to ₹103.01 crore, lower than both the previous half-year and the corresponding period last year. Management had claimed that migrating from rented facilities would generate a direct savings of ₹32 lakhs per month. While those rental costs did drop, they were quickly replaced by depreciation charges, which rose from ₹3.20 crore in FY25 to ₹6.63 crore in FY26, alongside higher financing costs.

Management Note (Nov 2025): “H2 profitability should recover as operational normalization completes and rental expenses are eliminated from the ledger.”

The reality is that H2 FY26 net profit collapsed to ₹1.48 crore. While the relocation was completed structurally, the operational efficiency gains have yet to materialize in the financial performance.