Aeroflex Enterprises (formerly SAT Industries) is currently a shape-shifter in the Indian mid-cap space. If you are looking for a boring, linear manufacturing company, look elsewhere. This is a high-octane business incubator and holding giant that just pulled off a masterstroke. The headline grabber isn’t just the 24.4% YoY revenue growth in Q4; it is the absolute clinical execution of the “AEL Playbook”—identifying, scaling, and exiting businesses at massive valuations.

The company recently concluded the sale of its 68% stake in M.R. Organisation (MRO) to the global giant Ingersoll-Rand for a staggering ₹227.42 crore. This wasn’t just a transaction; it was a validation. AEL took a specialized air compressor parts business, scaled it through inorganic acquisitions in the US, UK, and Portugal, and flipped it to a Fortune 500 buyer within roughly 21 months, clocking an eye-watering XIRR of 107%.

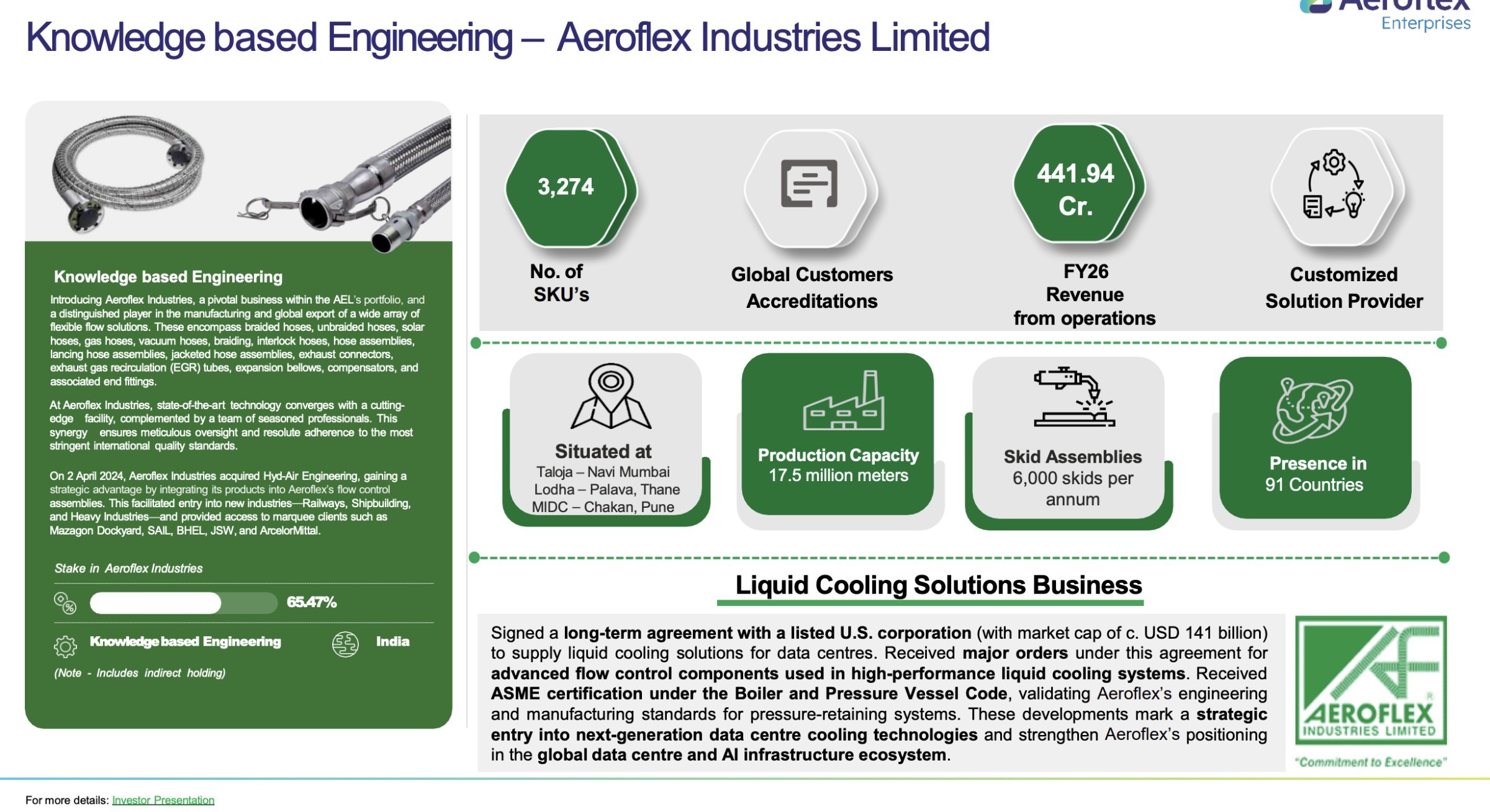

But don’t let the champagne distract you from the core. While the MRO exit provides a massive cash chest, the core manufacturing engine—Aeroflex Industries—is pivoting toward the AI revolution. By entering the liquid cooling solutions market for data centers and signing a long-term contract with a $141 billion US corporation, AEL is positioning itself at the heart of global tech infrastructure.

However, complexity brings shadows. With 10 subsidiaries, 6 business verticals, and a finger in over 160 startups, this is a financial labyrinth. The company is now aggressively pivoting into IT Parks, AI Parks, and real estate with a ₹325 crore capex plan. Critics might ask: is this strategic diversification or a lack of focus? The balance sheet is sparkling with a Debt-to-Equity of 0.05, but the “holding company discount” is a ghost that often haunts such structures. Can management maintain this M&A winning streak, or is the complexity starting to outpace the control?

Introduction

Aeroflex Enterprises is not your average industrial house. It is a diversified conglomerate that operates more like a Private Equity fund with manufacturing muscles. Founded in 1985, the company has evolved from a general trading firm into a sophisticated incubator. It operates across six distinct verticals: Knowledge-based Engineering, Innovative Packaging, Engineering Services, Fintech, Global Commerce, and Investments.

The company’s philosophy is built on a “Dual-Engine” model. One engine generates steady, predictable cash flows from manufacturing stainless steel flexible hoses and industrial packaging. The second engine is a high-growth investment vehicle that nurtures startups and subsidiaries for eventual high-value exits.

The recent name change from SAT Industries to Aeroflex Enterprises marks a new era where the brand “Aeroflex”—synonymous with high-end engineering—takes center stage. With a global footprint spanning 100+ countries and offices in major hubs like the USA and UK, AEL is leveraging its “Make in India” manufacturing base to capture premium global margins.

Business Model – WTF Do They Even Do?

To understand Aeroflex, you need to stop thinking about a single product and start thinking about a portfolio of platforms.

1. The Cash Cow: Aeroflex Industries (65.47% Stake)

This is the crown jewel. They make stainless steel flexible flow solutions (hoses and assemblies). These aren’t your garden-variety garden hoses; they are used in high-pressure environments like aerospace, refineries, and now, Data Center Liquid Cooling. When an AI server gets hot, Aeroflex’s skid assemblies keep it cool.

2. The Growth Bet: Innovative Packaging (Sah Polymers/Aeroflex Neu)

They manufacture FIBC (Flexible Intermediate Bulk Containers) or “big bags.” It sounds boring until you realize these are essential for global trade in chemicals, food, and minerals. They just secured a BRCGS Grade A+ certification, which is essentially a golden ticket to supply the high-margin global food and pharma industries.

3. The Money Lender: Aeroflex Finance

A 100% owned NBFC. They lend to MSMEs with a 22% Net Interest Margin (NIM). While the loan book is relatively small at ₹44.49 crore, they maintained a 0% Net NPA, which is almost unheard of in the risky MSME space.

4. The Startup Lab

AEL holds stakes in 168 startups across deep tech, fintech, and biotech. They treat this like a nursery—some will die, but the winners (like Pee Safe with a 9.39x exit) pay for the entire lot and then some.

Does having one foot in “Steel Hoses” and the other in “AI Parks” make sense to you, or does it feel like they are trying to cook too many dishes at once?

Financials Overview

The company has delivered a robust set of numbers, characterized by strong top-line growth and stable margins. The “Other Income” remains a significant part of the story due to investment gains.

Metrics (₹ Cr)

Latest Quarter (Q4 FY26)

Same Qtr Last Yr (YoY)

Previous Quarter (QoQ)

Revenue

199.58

160.83

191.42

EBITDA

43.53

33.14

42.78

PAT

25.67

18.50

24.81

EPS (₹)

2.12

0.98

1.42

Annualised EPS Calculation: Since this is the Q4 (March) result, we use the full-year reported EPS. The FY26 Consolidated EPS stands at ₹5.68.

Current P/E Ratio: With the CMP at ₹102 and FY26 EPS of ₹5.68,