The latest numbers are out, and the situation at Aarti Surfactants is a classic case of running faster just to stay in the same place. While the top-line growth is explosive—surpassing ₹859 crore for the full year—the profitability engine is coughing. Investors are watching a company that is successfully grabbing market share from giants like HUL and P&G, yet struggling to protect its own margins against the relentless tide of raw material volatility.

The most glaring red flag? A massive credit rating downgrade from CARE in late 2025, which saw the long-term bank facilities slide from A- to BBB+. The reason was simple: “continued lower-than-expected operating performance.” When the rating agencies stop being polite, the market starts getting nervous.

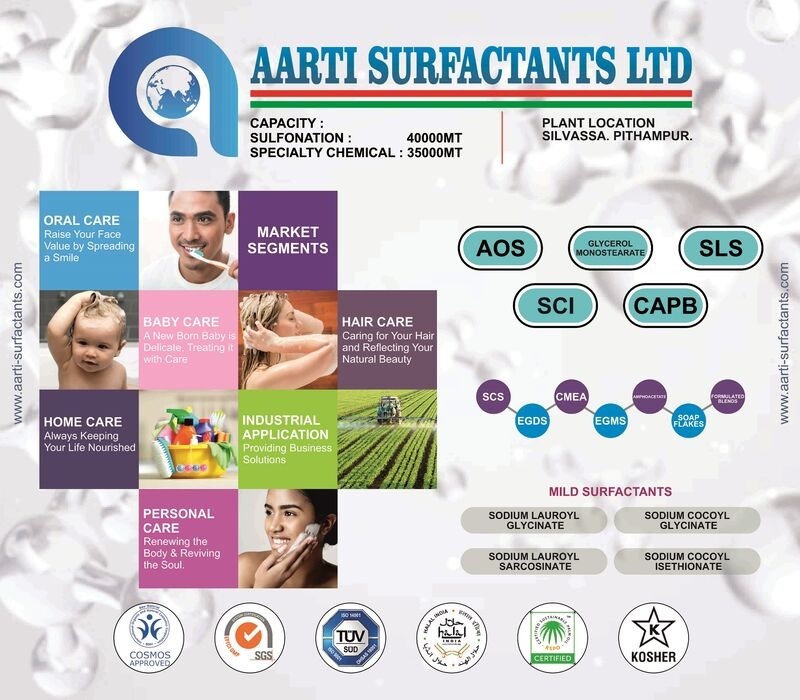

1. At a Glance

Aarti Surfactants is currently a study in contradiction. On one hand, you have a company that has successfully demerged from the legendary Aarti Industries and maintained a “preferred supplier” status with the gods of the FMCG world—Colgate, Dabur, and Hindustan Unilever. On the other hand, you have a financial profile that looks increasingly fragile.

In FY26, the company reported a massive 30% surge in sales, hitting ₹859.13 crore. This sounds like a victory lap until you look at the Net Profit. Despite the revenue boom, the Net Profit for the year actually fell to ₹12.34 crore from the previous year’s ₹14.54 crore. That is a textbook definition of “profitless growth.”

The Red Flags You Can’t Ignore:

- Margin Meltdown: Operating Profit Margins (OPM) have collapsed from double digits in FY24 to a measly 5.15% in the latest quarter.

- Raw Material Trap: About 80% of revenue is consumed by raw materials like Lauryl Alcohol and Fatty Acids. These are tied to palm oil prices. When palm oil swings, Aarti’s bottom line bleeds.

- The Debt Shadow: The company is funding an ₹85 crore capex mostly through debt (₹60 crore). With operating cash flows under pressure, servicing this debt is becoming a tightrope walk.

- Customer Concentration: A staggering 71% of revenue comes from just a few top customers. If one big FMCG player decides to squeeze prices or switch suppliers, the house of cards could wobble.

Is this a temporary transition or a permanent margin trap? The company is expanding capacity at Pithampur and Silvassa, betting big that scale will eventually lead to stability. But for now, the numbers tell a story of high stress and low returns.

2. Introduction

Aarti Surfactants (ASL) was born in 2018, carved out of the massive Aarti Industries group to focus specifically on the home and personal care ingredient space. If you’ve used a shampoo, a dishwashing liquid, or a baby wash in India, there is a very high probability you’ve used an Aarti product without knowing it. They make the “bubbles” and the “cleansing agents” that make soaps work.

The company operates in a niche that should, theoretically, be recession-proof. People don’t stop washing their hair or cleaning their floors because the economy is slow. However, being a middleman between global chemical suppliers and giant FMCG companies is a brutal business. You get squeezed from both ends.

Currently, ASL is in the middle of an aggressive expansion phase. They are moving from being a simple surfactant manufacturer to a producer of “specialty blends” and “mild surfactants”—the kind of stuff used in premium skin care and baby products.