🧪 “Acutaas Chemicals: Pharma Intermediates + Korean Chip Drama = Multi-Bagger Plotline?”

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

1. 🧬 At a Glance

Acutaas Chemicals (FKA Ami Organics) is a specialty chemicals company focused on pharma intermediates, agrochemicals, and now… semiconductor chemicals. With a ₹9,200 Cr market cap, 41% 5Y PAT CAGR, and zero serious debt, it’s got the ingredients of a compounder. But a P/E of 58x and recent promoter stake cuts mean you better look closer before sipping the Kool-Aid.

2. 🧠 Introduction with Hook

Pharma + semiconductors in one company? Sounds like a LinkedIn overachiever.

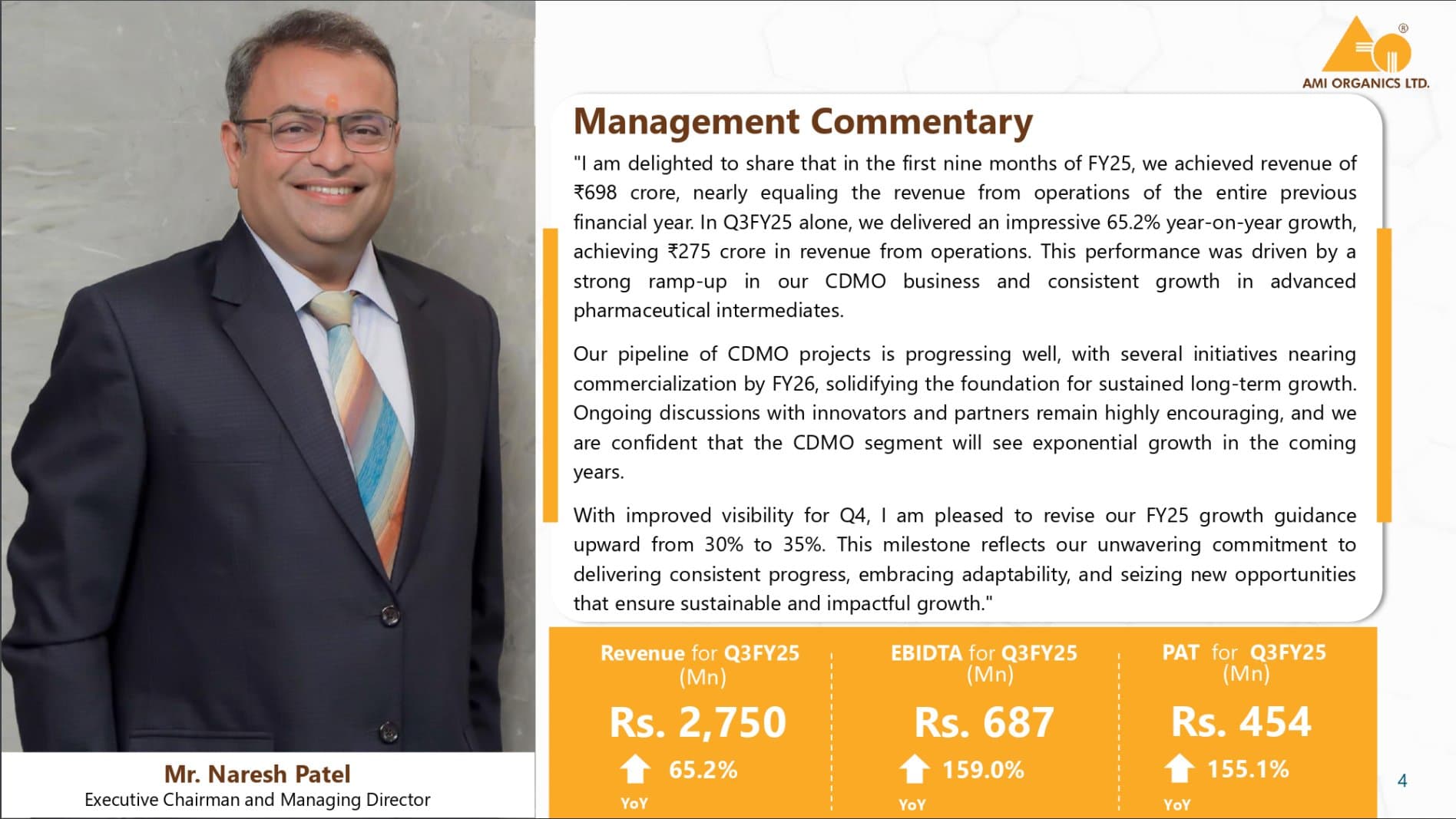

Acutaas started as a humble pharma intermediates maker and now wants to supply chemicals to chip fabs in South Korea.

ROCE of ~20%, profits up 3x in 3 years, cash flows finally kicking in.

So… is this the new Neuland Labs x Tata Elxsi combo? Or just high-multiple hype?

3. 🏭 WTF Do They Even Do? – Business Model

Acutaas operates in 3 verticals:

Pharmaceutical Intermediates (core biz)

Advanced intermediates for regulated APIs and New Chemical Entities (NCEs)

Products for oncology, neuro, anti-psychotic APIs

Agro & Fine Chemicals

Custom intermediates for global crop protection majors

Includes key starting materials (KSMs)

New Bet – Semiconductor Chemicals 🧪

JV with Korean partner (KRW 30B) to make chip-grade fine chemicals

Strategic: High-margin, import substitution play, but early stage

Clients include 8 of the top 10 global pharma companies, but now diversifying hard.