Dhampur Sugar Mills Q4 & FY26: Recovery on Borrowed Time

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Dhampur has engineered a sharp turnaround in Q4—net profit ₹45.6 Cr versus ₹49.0 Cr in Q4 FY25—but the full year tells a different story. FY26 net profit of ₹65.1 Cr trails FY24’s ₹134.3 Cr by half, though it inches ahead of FY25’s ₹52.2 Cr.

The company sits on ₹13 Cr of cash, down from ₹124 Cr a year ago. Inventory, which swelled to crush-season levels, has begun to thin—₹858 Cr down from ₹899 Cr. The balance sheet remains heavy with ₹899 Cr in borrowing.

A buyback at ₹185 per share (completed in FY26) cost ₹20 Cr. The income tax department conducted a search in late October 2025 across offices and plants; the company says no disruption. Credit ratings sit at AA−/Negative, reflecting the creditor anxiety that margins alone cannot ease.

This is a business pausing between cycles—margin squeeze and leverage working in opposite directions, with exports and government policy as the wildcard.

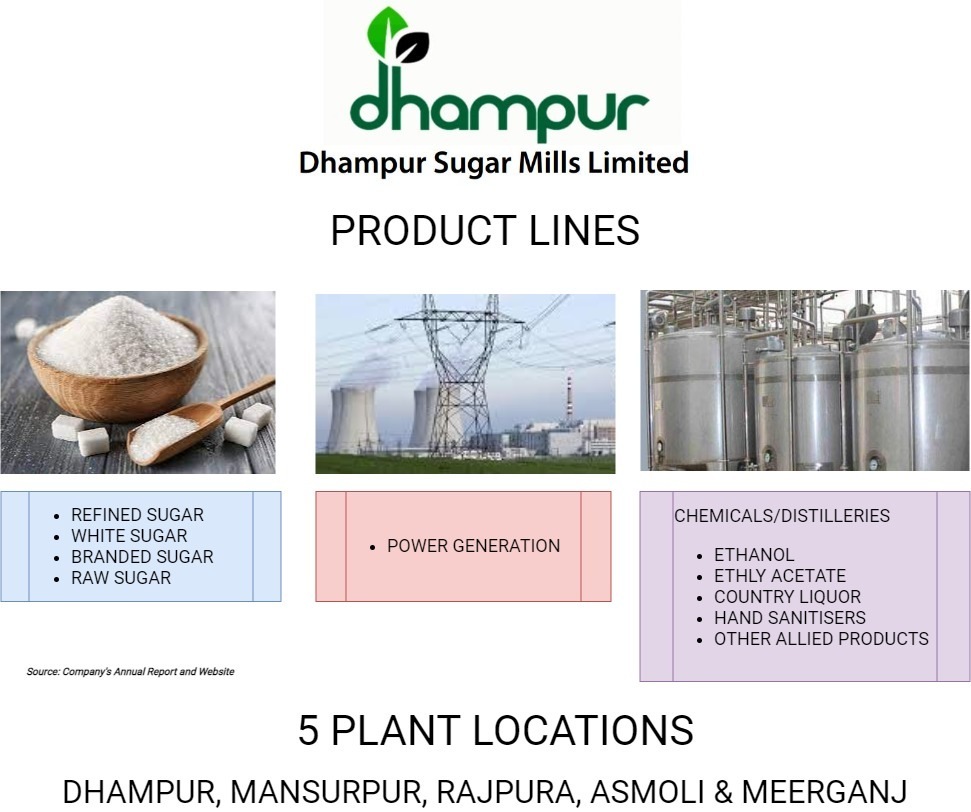

2. Introduction

Incorporated in 1933, Dhampur Sugar Mills is a nine-decade-old integrated operation sited in Uttar Pradesh’s western belt: Dhampur and Rajpura plants with a combined crushing capacity of 24,000 tonnes per day. The company has evolved beyond sugar into ethanol distillation (350 KLPD capacity), power co-generation (127 MW), chemical production (140 tonnes/day ethyl acetate), and a growing potable spirits business under the “Mishti by Dhampur” brand.

Management completed an ₹20 crore buyback of 1.08 crore shares in June 2025 at ₹185 per share, reducing share count to 6.43 crore. In May 2026, an interim dividend of ₹2 per share (20% on face value ₹10) was declared. The board has also approved a share purchase agreement to acquire 51% of Venus India Asset-Finance (a non-deposit-taking NBFC) for ₹50 crore, pending RBI clearance.

Sugar, which accounts for over half of group revenue, faces headwinds: the state advisory price (SAP) of sugarcane in Uttar Pradesh rose ₹30 per quintal to ₹400/qt for the 2025–26 season. Ethanol, once the margin buffer, has stalled on fixed government pricing unchanged since November 2023. Power continues to perform, and potable spirits—buoyed by new tetra-pack capacity added late FY25—has become a material revenue driver.

3. Business Model: WTF Do They Even Do?

Sugar dominates—₹1,496 Cr of FY26 revenue (76% of net sales), produced from 27.96 lakh tons of cane crushed in the year. But the model folds in a built-in margin cushion through three adjacent streams.

Ethanol. The company operates 350 KLPD of cane-based capacity and 100 KLPD of grain-fed multi-feed distillery. FY26 ethanol sales of ₹434 Cr (22% of revenue net of excise) fell sharply from FY25’s ₹510 Cr, chiefly because the company cut molasses-based production by 75% and syrup-derived output by 55%—both are margin destroyers when ethanol prices don’t move. Grain-based ethanol, sold at ₹69/litre, cushioned the blow and provided 337 lakh BL of the year’s 570 lakh BL total. The government’s ethanol blending target for ESY26 (Nov 2025–Oct 2026) appears set at 20%, reached almost entirely in ESY25 itself; beyond that, the roadmap is a fog.

Power. Co-generation of 127 MW capacity turned 31.95 crore units in FY26 (27.96 lakh tons of cane crushed worth 1.14 MW-days), exporting 14.6 crore units at an average ₹4.55 per unit, earning ₹250 Cr (12.7% of revenue). The segment’s EBITDA rose to ~40% of group total in FY25 (from 30% in FY24), reflecting the shift as sugar and ethanol margins compress. Power realizations are steady but not lucrative.

Chemicals and Potable Spirits. Ethyl acetate production dropped sharply FY26 (249 lakh kg vs. 323 lakh kg FY25) due to geopolitical price volatility and operational lag; the chemical segment posted a ₹2 Cr loss in FY25 but recovered to ₹10 Cr EBITDA in FY26. Potable spirits, by contrast, has raced ahead: 33.16 lakh cases sold in FY26 (31.16 in FY25), generating ₹935 Cr revenue on newly installed tetra-pack lines (10,000 cases/day added across two tranches). This business is high-volume, low-margin work, but it moves the aggregate revenue needle.

The model’s elegance is also its curse: it is hyper-sensitive to cane availability (weather, disease, policy-set pricing), government ethanol mandates, and commodity volatility. Integrated mills are not conglomerates—they are sugar mills that happen to have ancillary income.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Q4 FY26

Q4 FY25

YoY

FY26

FY25

YoY

Revenue (Net)

490.7

618.5

-20.7%

1,967.4

1,956.5

+0.6%

EBITDA

92.4

102.5

-9.9%

196.7

187.3

+5.0%

PBT

59.9

71.2

-15.9%

85.8

75.1

+14.4%

PAT (Net Profit)

45.6

49.0

-6.9%

65.1

52.2

+24.8%

EPS (₹)

7.08

7.49

-5.5%

10.12

8.12

+24.6%

The full-year narrative reflects two forces in tension. Q4 dragged (sales -20.7% YoY), yet FY26’s aggregate sales edged ahead of FY25 by a whisker (₹1,967 Cr vs. ₹1,957 Cr). The prior-year base was compressed: FY25 suffered a harvest crunch (cane crush down to 28.49 lakh tons from 36.69 in FY24); FY26 saw further contraction to 27.96 lakh tons. Lower cane volume fed a squeeze on both sugar revenue and byproduct income.

EBITDA, surprisingly, expanded 5% despite revenue flatness. This reflects a shift in mix: power and potable spirits (higher-EBITDA streams) gained share as sugar, starved of feedstock, retreated. Interest costs remained flat at ₹49 Cr, a slight relief as debt levels declined. Depreciation spiked to ₹62 Cr (from ₹62 Cr in FY25, nearly unchanged), weighted by legacy capex on ZLD infrastructure and distillery upgrades.

Net profit rose 24.8% to ₹65.1 Cr, bumped by lower tax impact (effective tax rate fell to 24% in FY26 from 29% a year prior). Yet this is earnings walking on stilts: the operational cash inflow of ₹243 Cr (FY25: ₹201 Cr) is real, but it masks a working capital unwinding—inventory dipped to ₹858 Cr from ₹899 Cr. Strip that, and underlying operating leverage is flat.

5. Market Expectations & Historical Multiples

This section describes how the market is currently pricing the company and how that compares with its own history and peer group. It is descriptive, not predictive.

Metric

Current

5-Year Avg

Peer Median

P/E Ratio

14.0x

11.4x

17.1x

EV/EBITDA

9.1x

N/A

8.5x

P/B Ratio

0.76x

N/A

0.93x

ROE

5.4%

7.1% (3-yr)

7.02%

ROCE

3.1%

5.6% (3-yr)

7.54%

The market currently assigns a P/E of 14.0x to Dhampur, above its five-year median of 11.4x but below the peer group’s 17.1x median (which includes higher-return sugar companies like Balrampur Chini at 29.8x and Triveni at 29.4x).

EV/EBITDA sits at 9.1x, in line with peers at 8.5x—the valuation framework does not penalize leverage or scale differentials. Price-to-book of 0.76x indicates the market perceives