The Anup Engineering Ltd: FY26 in ₹822 Cr—The Sequel Nobody Ordered

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

The Anup Engineering grew revenue 12% to ₹822 Cr in FY26, driven largely by export orders and Kheda plant commissioning. EBITDA slipped to ₹174 Cr (21.2% margin), a dip from FY25’s ₹165 Cr (22.5% margin).

The company printed strong PAT of ₹110 Cr—but that’s down 6.7% YoY. This wasn’t a disaster; the concall made clear that FY26 was “very difficult and eventful,” with geopolitical disruption, steel volatility, and shipping-line closures compressing the last two months of execution.

The order book sits at ₹769 Cr, a 9% lift from ₹706 Cr at the start. Working capital deteriorated sharply: receivables jumped to ₹416 Cr (185 debtor days), and cash swung to near breakeven after the company deployed ₹36 Cr into capex and ₹33 Cr into acquiring Mabel Engineers.

The market is pricing Anup at 34.2x trailing EPS—well above its 5-year average P/E of 33.2x—a multiple the company must now defend amid margin pressure and execution risk.

The tension: a young, export-driven equipment manufacturer scaling aggressively into new verticals (nuclear, thermal power, skids, technical services) while working capital burns cash and execution remains lumpy quarter to quarter.

2. Introduction

The Anup Engineering Limited is a 62-year-old heat exchanger and process equipment manufacturer spun out of Arvind Limited in 2018. The Lalbhai Group sits at 41% ownership, with Sanjay Lalbhai serving as chairman (though stepped down in November 2025; Punit Lalbhai took over).

The business sits in a niche—custom-engineered, fixed-price equipment for oil refineries, petrochemicals, fertilizers, and power plants. Margins are guarded by technical moats (Helixchanger licensee from Lummus Tech, exclusive partnerships with Graham Corporation), a blue-chip customer roster (Reliance, IOC, GAIL, Nayara Energy), and a decades-long track record.

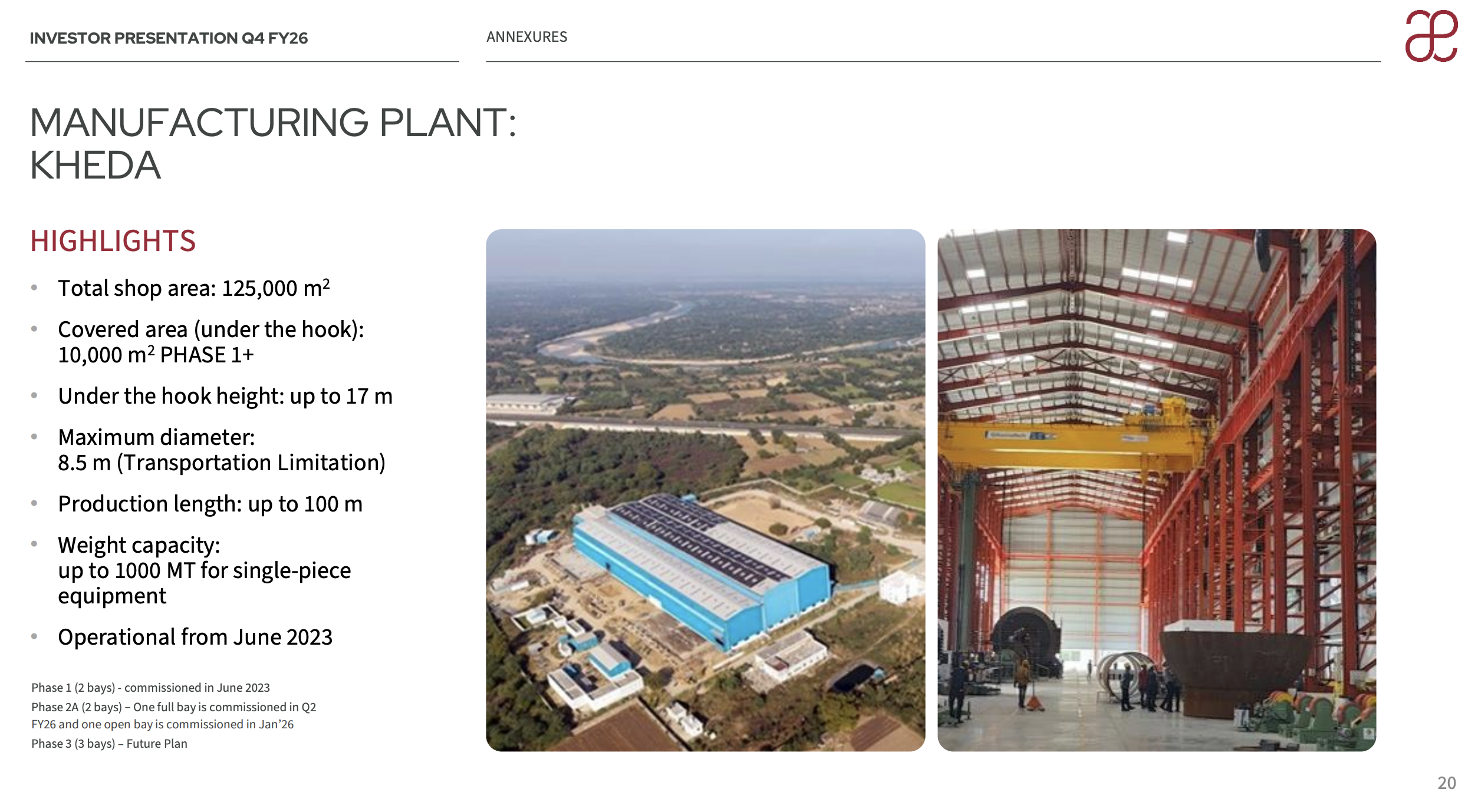

What changed in FY26: the company commissioned Phase-2 at its Kheda plant, boosting capacity from ~12,000 MTPA to 20,000 MTPA. Mabel Engineers, a Tamil Nadu-based silo/tank specialist, was acquired for ₹33 Cr in March 2024. A new design office at Vadodara came online. Technically, the chassis for ₹1,200 Cr+ revenue is now in place.

The catch: execution stumbled. FY26 was marked by raw material delays, constrained industrial gas supply, and shipping gridlock—the company couldn’t convert this infrastructure into profitable orders as fast as shareholders hoped.

3. Business Model: WTF Do They Even Do?

Anup makes heat exchangers (54% of FY26 revenue), pressure vessels (33%), and smaller volumes of reactors, centrifuges, towers, skids, and tanks. Every unit is custom-built—no standardization, no off-the-shelf economics. The engineering is bespoke; the metallurgy is exotic. A customer hands over a technical spec; Anup quotes a fixed price and a delivery date. Six to twelve months later, the equipment ships.

This is not a high-volume business. It’s a high-touch, high-skill business.

Revenue flows from two channels: domestic (48% in FY26) and exports (48%). Exports reached ₹460 Cr in FY25 (concall data shows 65% of orders now export-destined as of March 2025). The company’s three plants cover the geography: Ahmedabad (the legacy 45,000 sqm shop), Kheda (newly ramped, up to 8,000 MTPA), and Mabel in Tamil Nadu (20,000 sqm, lighter load capacity).

The product portfolio has been expanding with intent. FY26 milestones: first nuclear order (NPCIL’s Kaiga-5/6), first thermal power order (NTPC EPC), first clean energy storage order, first skids package (₹30 Cr, 12-month cycle, ADNOC). The concall framed these as “firsts”—stepping stones into higher-margin, higher-ROCE verticals.

The pricing structure is fixed per contract—no price escalation clauses in sight. This sounds suicidal in an inflationary environment, but Anup’s dodge is procurement timing. Management described a deliberate policy: buy raw materials immediately after PO (“protect ourselves from price volatility”), but delay procurement on ~₹200–250 Cr of pending order book, waiting for “the right time for raw material cost to cool down.” In other words: bid low, hold execution timing, protect margin.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

FY26

FY25

Change

Revenue

822

733

+12.2%

EBITDA

174

165

+5.4%

EBITDA %

21.2%

22.5%

–130 bps

PBT

139

143

–2.7%

PAT

110

118

–6.7%

EPS (annualised)

55.11

59.07

–6.7%

The concall attributed the margin squeeze to product mix. Q4 FY26 revenue was ₹208 Cr (–6.2% QoQ), and operating profit fell ₹38 Cr (–23% QoQ). Management pinned this on “the kind of projects executed in quarter 4″—mix had shifted toward lower-margin product categories and site-execution-heavy work.

The company also took a ₹1.45 Cr exceptional gratuity charge (Labour Code compliance) and booked a ₹5.33 Cr tax reversal in the PAT line. Net income, before those adjustments, would have been closer to ₹115 Cr.

5. Valuation Discussion: Fair Value Range (Educational Only)

What follows is a walkthrough of how three valuation methods work, using this company’s numbers as the example — not a target, not a forecast, not