Cello World Ltd Mar 2026: Highest-Ever Quarterly Revenue Amid Subdued Hydration Margins

General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1 — At a Glance

The financial narrative for Cello World Ltd in FY26 reflects a distinct divergence between top-line expansion and bottom-line optimization. Annual revenue rose to ₹2,323.71 crore in FY26, up from ₹2,136.39 crore in FY25. Despite this growth, annual net profit contracted slightly from ₹338.82 crore to ₹331.51 crore over the same period.

Operational constraints presented persistent headwinds throughout the year. Glassware utilization levels hovered at 60% due to aggressive import dumping from China, while a strategic shift from Chinese imports to domestic original equipment manufacturers (OEMs) compressed hydration margins by 5% to 6%. On the positive side, Q4 FY26 delivered record quarterly revenue of ₹653.59 crore, driven by a 64% year-on-year surge in the writing instruments segment.

Balance sheet liquidity metrics signals clear inefficiencies, as working capital days expanded significantly from 184 days to 279 days. A growing top-line provides minimal comfort when structural supply transitions and underutilized production lines strain near-term profitability. The analysis turns next to how these moving parts fit into the broader operational reset.

2 — Introduction

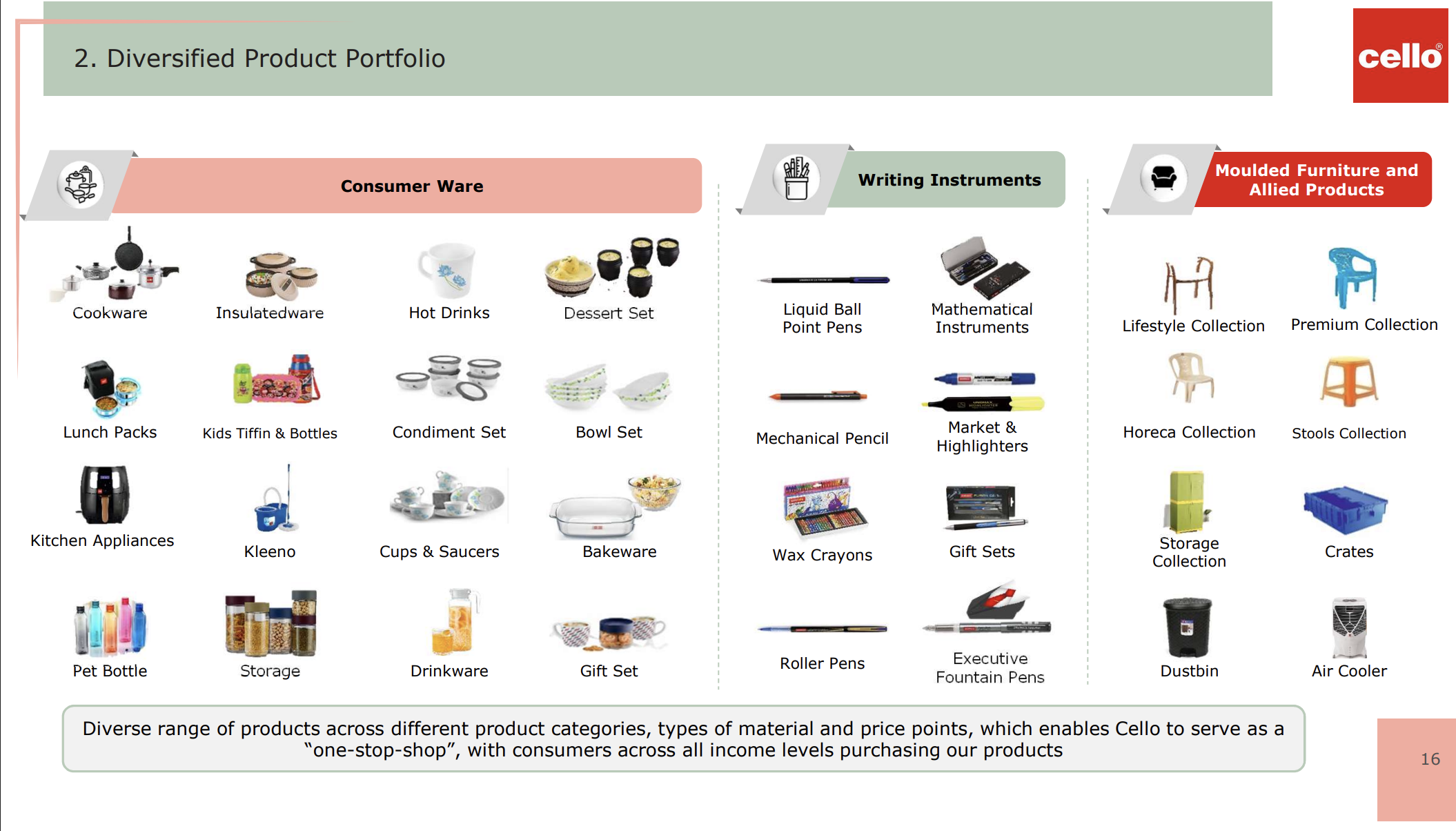

Cello World Ltd operates as an established participant in the Indian consumer products market, maintaining a presence across multiple consumer categories. The company’s operational footprint spans consumer houseware, writing instruments and stationery, alongside molded furniture and allied items. This structural diversification is designed to capture varied consumer spending points across household lifecycles.

A major structural reorganization concluded recently with the merger of Wim Plast Ltd into Cello World Ltd, effective May 27, 2026, with an appointed date of April 1, 2025. This corporate consolidation seeks to streamline regulatory compliance and integrate overlapping manufacturing and distribution frameworks.

The market has priced in these operational transitions through a prolonged correction. The stock delivered a 1-year return of -37.4%, reflecting near-term caution regarding margin compression and competitive pressures. Prices referenced in this analysis are not live, utilizing a lagged reference price of ₹382.1 per share. This valuation context serves as the baseline for evaluating the company’s asset efficiency and category performance.

3 — Business Model: WTF Do They Even Do?

The company effectively manufactures and distributes the plastic, glass, and steel material culture of the Indian middle-class household. Its corporate architecture relies on three primary segments: Consumer Houseware, Moulded Furniture & Allied Products, and Writing Instruments

The consumer houseware business represents the largest chunk, driven by brands like Maxfresh, Puro, and Duro. The company recently committed ₹250 crore to an in-house glassware facility in Falna, Rajasthan. However, the plant operates at a modest ~60% utilization rate, constrained by low-cost Chinese imports that have kept the segment near financial breakeven.

The writing instruments division operates via the Unomax brand and was recently augmented by a zero-royalty lease agreement with the promoter group to regain the use of the legacy “Cello” trademark. While this segment expanded rapidly in Q4 FY26, the integration acts as an immediate drag because the acquired stationery operations were structurally loss-making prior to absorption.

A unique characteristic of the model is that the listed entity does not own its core trademarks. The brands Cello, Unomax, Kleeno, and Puro remain registered under a private promoter partnership firm, Cello Plastic Industrial Works. The business essentially leases its brand identity from its founders. Furthermore, a legacy litigation initiated in 2017 by competitor BIC Clichy alleging non-compete violations continues to sit unresolved before the Bombay High Court.