Virat Industries Ltd (Mar 2026): The ₹114 Crore Cash Pile and the Curious Case of the Vanishing Core Business

Date of Publishing -

Spotted a factual error — a wrong number, date, or fact? Tell us and we will check the source.

1. At a Glance

Virat Industries Ltd presents a striking paradox in the micro-cap landscape as of March 2026. The company reported full-year FY26 revenue of ₹26.79 crore, marking a significant 15.30% decline from ₹31.63 crore in FY25. However, the headline net profit surged to ₹4.94 crore from ₹0.90 crore in the previous year, driven almost entirely by an other income spike of ₹6.28 crore.

The primary catalyst altering the company’s financial DNA is a massive preferential allotment of 95,99,999 equity shares executed in March 2026, which expanded the equity base from ₹4.92 crore to ₹14.52 crore and injected liquid cash onto the balance sheet. Consequently, the cash and bank balances ballooned from ₹7.38 crore to ₹114.53 crore. This cash pile now constitutes 85.04% of the total asset base, completely overshadowing the shrinking operations of the core hosiery manufacturing business.

When a corporate balance sheet transforms faster than its underlying business operations, public investors must differentiate between operational earnings power and structural balance sheet re-engineering.

While public shareholders face an immediate and massive equity dilution, the sudden influx of liquidity presents an entirely new capital allocation trajectory. The market is now forced to price this entity not as a legacy textile exporter, but as a cash-heavy shell awaiting a definitive corporate transformation.

2. Introduction

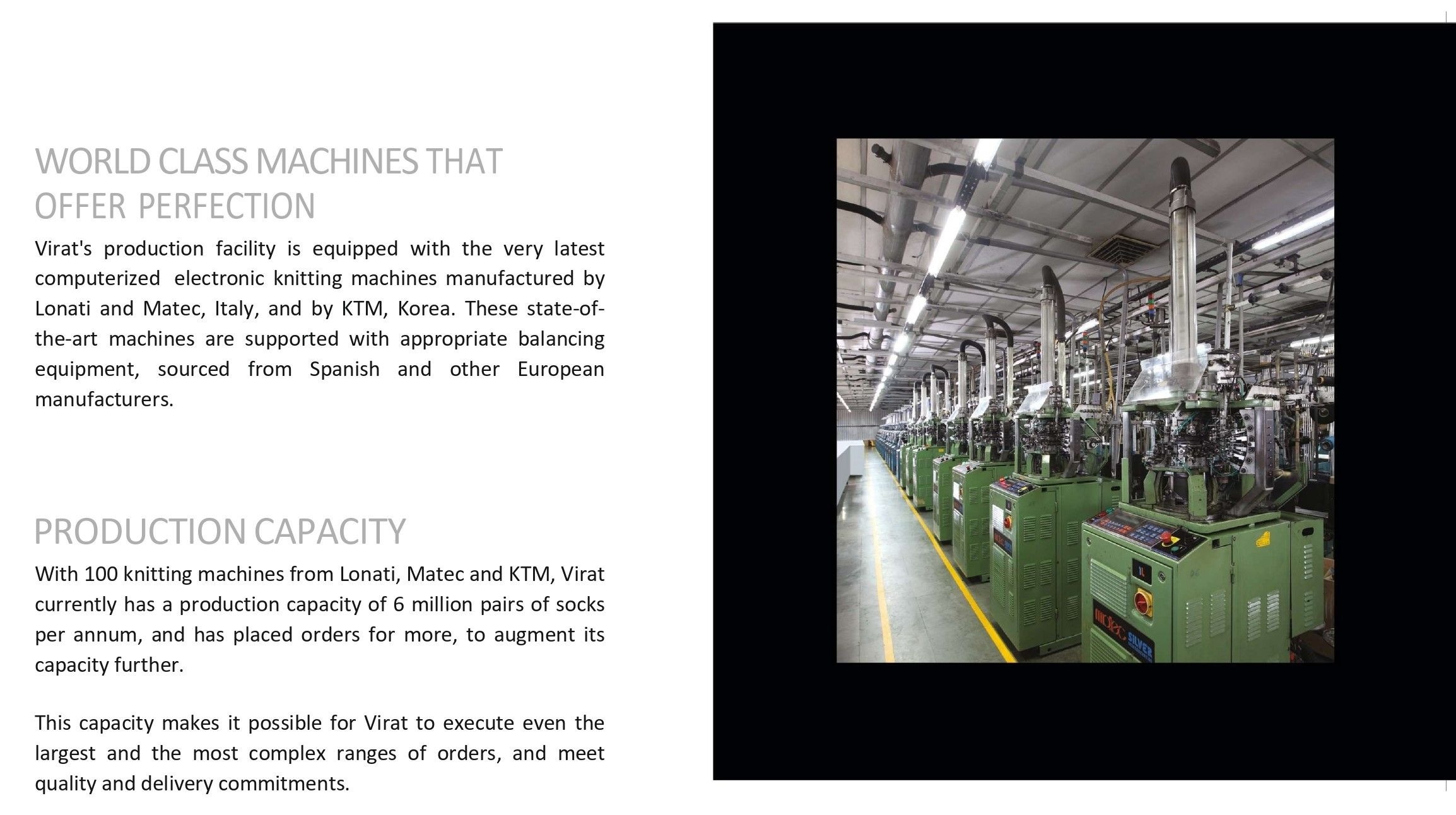

Virat Industries Ltd, established in 1995, has historically operated as a small-scale contract manufacturer and exporter of premium dress and sports socks. From its manufacturing facility in GIDC, Gujarat, engineered with an installed capacity of 8.7 million pairs per annum, the company has traditionally supplied European markets, including relationships with international brands such as Puma, John Lewis, and Ted Baker.

However, recent corporate actions indicate that the legacy textile business is no longer the primary focus of management. Over the past twelve months, the company has undergone significant board restructuring, changes in majority control, proposals for corporate name changes, and an aggressive expansion of investment limits. The business stands at an existential crossroads, transitioning away from its export-oriented manufacturing roots toward an unmapped corporate canvas.

3. Business Model: WTF Do They Even Do?

At its core, the operational model of Virat Industries involves turning raw cotton, nylon, and lycra into high-end footwear accessories using computerized electronic knitting machines imported from Italy and Korea. Historically, the company was a pure-play export vehicle, sending 47% of its production to Switzerland and 37% to the United Kingdom, leaving India with a meager 6% share of sales.

The structural flaw in this model is its complete dependence on specific international contract orders without any proprietary brand equity. When European retail demand softens, the factory floors grow quiet. Production dropped from a peak of 97.05 lakh pairs in FY23 down to 69.80 lakh pairs. With a sales realization of roughly ₹42.60 per pair, the business operates on thin variables, high inventory dependency, and a long cash conversion cycle. It is a business that essentially manufactures socks for global giants while bearing all the operational overhead and capturing very little of the ultimate consumer premium.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Mar 2026)

YoY Change (%)

QoQ Change (%)

Revenue

5.10

-34.02%

-12.82%

EBITDA / Operating Profit

-0.37

-276.19%

-232.14%

PAT

1.05

+483.33%

-11.02%

EPS (₹)

0.72

+94.59%

-11.11%

The financial performance for the quarter ended March 31, 2026, reveals a stark decoupling between core operations and final profitability. Operational revenue contracted sharply to ₹5.10 crore, and the core manufacturing engine slipped into an operating loss of ₹0.37 crore as operating profit margins crashed to -7.25%.

The optical expansion in Net Profit to ₹1.05 crore was salvaged solely by ₹1.91 crore of other income, which represents interest on the newly acquired cash pile rather than manufacturing execution. Furthermore, while PAT grew by 483.33% YoY, the quarterly EPS only advanced by 94.59% due to the expanded share base resulting from the preferential share issuance.

Operational cash generation is the ultimate arbiter of corporate health; when net profits are manufactured in treasury desks while factory floors produce losses, the structural sustainability of earnings collapses.

What is Management Promising in the Coming Quarters?

Reviewing the recent corporate developments, management has remained tight-lipped regarding specific operational guidance for the hosiery segment. Instead, corporate announcements emphasize systemic re-allocation. The board previously authorized an increase in loans and investments under Section 186 up to ₹500 crore, telegraphing plans for significant external capital employment.

5. Valuation Discussion: Fair Value Range Only

To evaluate Virat Industries, standard historical earnings multiples are functionally obsolete because the corporate asset structure completely altered