Excelsoft Technologies Q4 FY26: The ₹464 Crore Receivable Puzzle and the Price of Same-Time-Zone Delivery

Section 1 — At a Glance

A newly listed entity presents a unique vulnerability to market expectations, where structural improvements can be entirely obscured by localized cost inflation. Excelsoft Technologies Ltd’s performance for the financial year ending March 31, 2026, highlights this delicate balance. Operating revenue reached ₹272.52 crore, representing a 16.82% year-on-year expansion, driven by a 37% volume expansion in its core Educational Technology Services wing. However, the absolute growth in revenue was met with a substantial compression in operating profitability. EBITDA margins deteriorated by 424 basis points to close at 26.83%, down from 31.07% in the prior fiscal year, caused primarily by a 46.8% spike in other operational overheads.

While headline net profit expanded by 25.03% to reach ₹43.38 crore, this improvement was fundamentally a reflection of statutory tax optimization rather than core structural efficiency, as the effective tax expense dropped from ₹24.85 crore to ₹15.96 crore. Concurrently, the balance sheet exhibits significant capital concentration. Trade receivables escalated to ₹46.41 crore, tying up vital working capital despite an improvement in collection cycles. Furthermore, despite generating substantial net profits across sequential cycles, the organization continues to maintain a zero-dividend payout policy, retaining all liquid surpluses within its reserves. Total equity expanded to ₹578.33 crore, yet the underlying return on equity remains constrained at 9.83%. The divergence between top-line expansion and margin degradation forms the primary analytical anchor for evaluating the asset’s current valuation framework.

Section 2 — Introduction

Excelsoft Technologies Ltd, established at the turn of the millennium in 2000, has spent more than two decades quietly anchoring itself in the corporate backdrop of Mysuru. The organization operates at the intersection of digital education platforms and enterprise software infrastructure. Having recently crossed the threshold from a private software house to a publicly traded entity listed on both the BSE and NSE, the company is experiencing the unvarnished scrutiny of public markets. Management’s recent strategic maneuvers indicate an aggressive push to transform a regional engineering hub into a globally distributed service framework, navigating the structural friction that such transitions inevitably entail.

Section 3 — Business Model: WTF Do They Even Do?

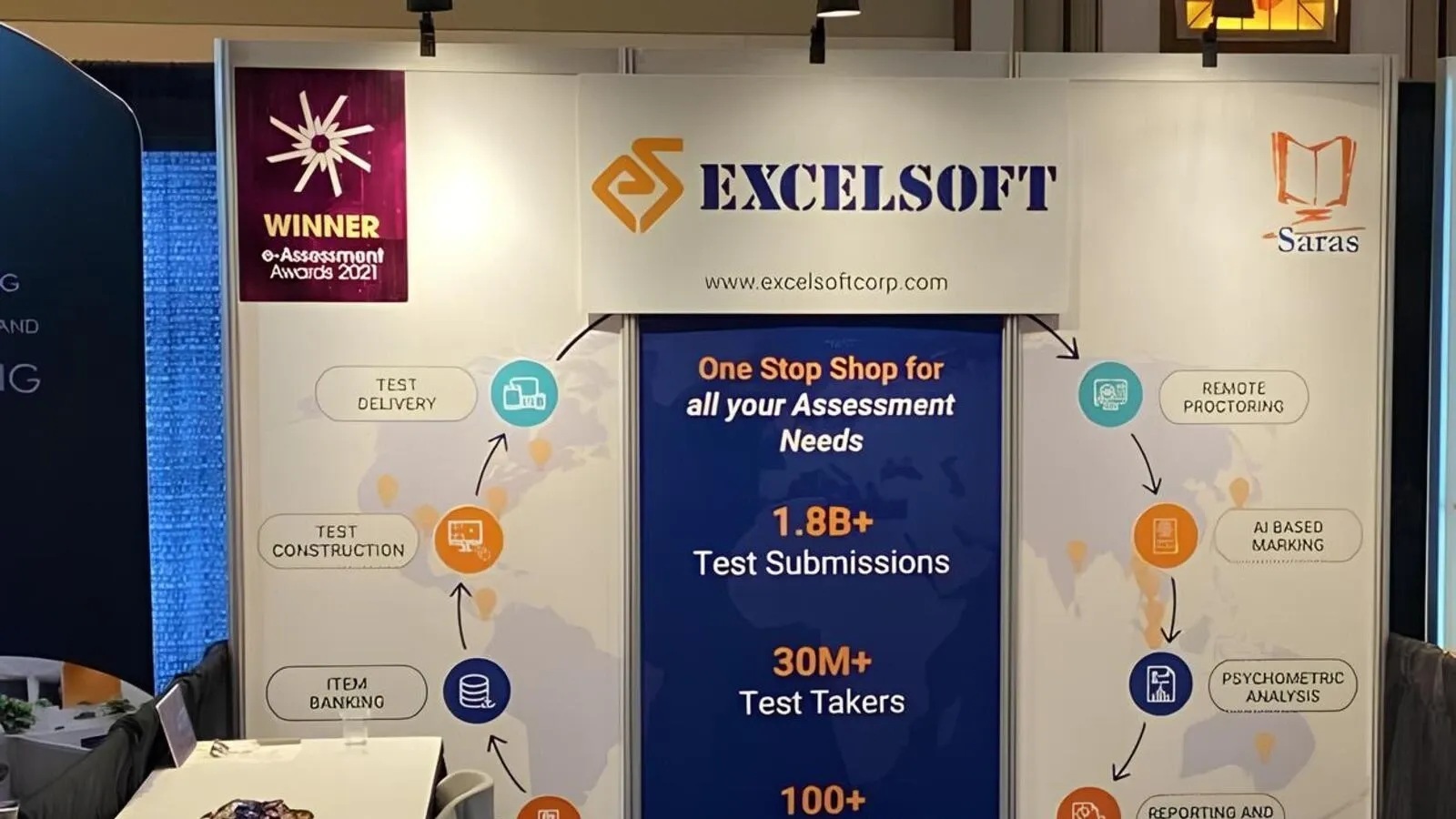

To the casual observer, Excelsoft sounds like generic tech nomenclature generated by an uninspired algorithm. In practice, they build the digital scaffolding that stops online examinations from collapsing into anarchy. The company operates as a vertical SaaS and product engineering business divided into four distinct buckets. Educational Technology Services (ETS) brings in the bulk of the money at 56.4% of total revenue. Assessment & Proctoring (A&P) brings in 27.3%, followed by Learning & Student Success at 11.8%, leaving a tiny 4.5% sliver for traditional Learning Design & Content.

Their flagship product, “Saras E-Assessments,” handles everything from test creation to role-based digital marking dashboards for evaluators. When students take exams remotely, Excelsoft deploys “EasyProctor,” an AI-enabled remote monitoring tool that uses computer vision algorithms to score behavior based on risk thresholds, categorizing students into low, medium, or high-risk categories. Essentially, if an enterprise client or a government body globally wants to administer a high-stakes test without students collaborating via smartphone, Excelsoft sells them the digital monitoring net.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Q4 FY26

YoY (%)

QoQ (%)

Revenue

81.16

16.08%

14.31%

EBITDA

24.57

-13.31%

24.72%

PAT

16.60

-18.95%

61.17%

Reported EPS (₹)

1.44

-31.75%

61.80%

The numbers for the final quarter of FY26 tell a story of growth meeting an expensive operational wall. While operational revenue climbed comfortably by 16.08% compared to the previous year’s winter quarter, the operating profit line suffered a 13.31% drop.

Earnings quality is never an abstract concept; it is the direct consequence of how much cash actually survives the operational funnel. In this case, the profit compression was driven entirely by a massive 76% surge in “Other Expenses,” which jumped from ₹11.84 crore to ₹20.86 crore in a single quarter.

What is Management Promising in the Coming Quarters?

During the post-earnings communications, management was remarkably vocal about this cost escalation. The Chief Strategy Officer clarified that the margin squeeze was a deliberate, customer-enforced maneuver. To secure high-value contracts in North America—which contributes 64.9% of total revenue—Excelsoft had to build a 30-member “nearshore” engineering and consulting team physically located within the United States.

Because these professionals were onboarded as external consultants for legal and structural reasons, their compensation did not touch the employee benefits line; instead, it landed directly inside other operational expenses to the tune of ₹8.50 crore in Q4 alone. Management noted that this ₹34 crore annualized run-rate is structural but expects it to serve as a wedge to pull down more profitable, high-margin back-end work to their Mysuru campus. The executive guidance explicitly targets a return to baseline EBITDA margins of 30% to 31% as these global implementations scale over the next twelve months.

Will the premium US consultant footprint actually pull down high-margin offshore development work, or simply act as a permanent tax on their operational margins?

Section 5 — Valuation Discussion: Fair Value Range Only

To establish a credible baseline for Excelsoft’s valuation, we must anchor the mathematical models to the actual reported performance metrics of FY26, utilizing a total share count of 11.51 crore equity shares. The reported full-year net profit stands at ₹43.38 crore, yielding an unadjusted full-year EPS of ₹3.77.

P/E Multiple Method

The broader information technology and IT-enabled services sector trades within a highly fragmented band. While premium digital engineering peers frequently command multiples above 40x, conservative small-cap IT service entities trade