Modison Ltd Mar 2026: The 443% Profit Explosion Built on High-Voltage Silver Drama

Section 1 — At a Glance

An extraordinary surge in net profit has captured the market’s attention, shifting the spotlight onto a highly specialized component manufacturer. Modison Ltd reported a remarkable 442.75% year-on-year increase in quarterly profit, reaching ₹36.00 crore for the period ending March 2026. This bottom-line velocity was supported by a robust 120.90% increase in quarterly sales, which climbed to ₹287.32 crore.

While these headline indicators suggest an unprecedented growth trajectory, a deeper examination of the underlying operational metrics reveals structural challenges. The company’s expansion has been heavily financed by short-term bank credit, causing total borrowings to rise sharply to ₹174.00 crore in March 2026 from just ₹31.00 crore in the prior year. This aggressive inventory accumulation and an extended cash conversion cycle of 223 days have generated substantial negative operating cash flows.

Furthermore, the operational performance remains deeply vulnerable to extreme price volatility in raw silver, which constitutes approximately 75% to 80% of total material purchases. High client concentration persists, with the top five customers controlling nearly 45% of total income. The core investment question shifts from celebrating the immediate quarterly surge to evaluating capital efficiency: spectacular short-term earnings acceleration loses its value if the incremental cash is permanently trapped inside the working capital cycle.

Section 2 — Introduction

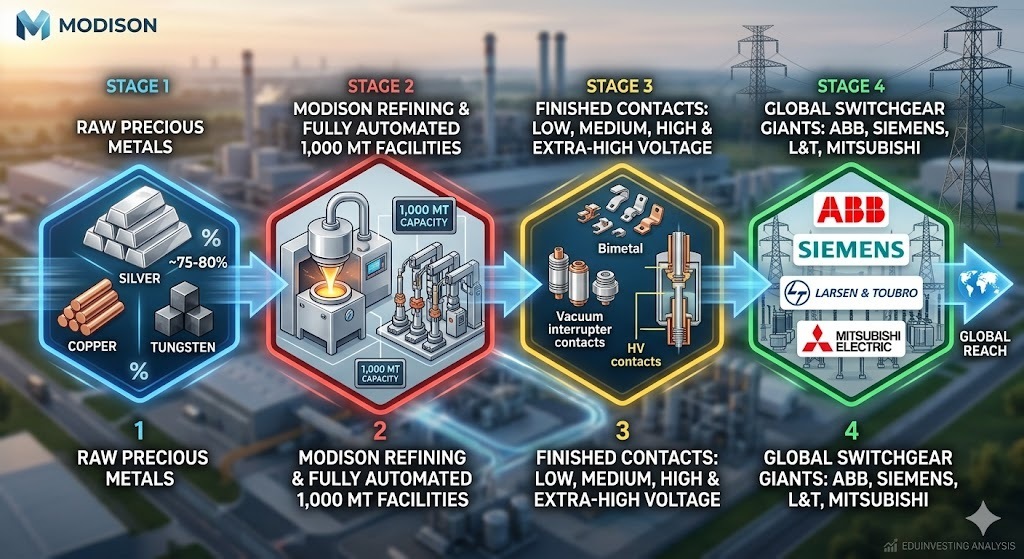

Modison Ltd has quietly anchored itself within the core infrastructure of global electrical switchgear. Established originally as a trading house in 1965, the enterprise pivoted toward manufacturing in 1975 by establishing silver refining operations. Over the subsequent decades, it transformed into a highly technical collaborator with global entities like Germany’s DODUCO KG.

Today, the business functions as a rare specialist manufacturing electrical contacts across low, medium, high, and extra-high voltage applications. Operating from its key facilities in Vapi and Silvassa, the company manages fully backward-integrated systems capable of refining raw precious metals and turning them into precision-engineered switchgear components.

Section 3 — Business Model: WTF Do They Even Do?

Modison is effectively a precious metal refinery masquerading as an engineering heavy-weight. They melt silver, copper, and tungsten into highly precise shapes like “tulips,” “plugs,” and “rivets” that prevent high-voltage electrical circuits from exploding when someone flips a switch.

The low and medium-voltage segments bring home 80% of the sales volume, while the elite high-voltage contacts bring in the remaining 20%. The brand client list reads like a global industrial country club: Siemens, ABB, Mitsubishi, Alstom, and Larsen & Toubro. However, the business model comes with high-voltage drama. When 75% to 80% of your raw material bills are dependent on raw silver, you are not just a manufacturer; you are a levered bet on precious metal spot prices. If silver spikes before an order is locked, the margins go on a sudden vacation.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Mar 2026

Dec 2025

Mar 2025

YoY (%)

QoQ (%)

Revenue

287.32

144.20

130.07

120.90%

99.25%

EBITDA

71.00

19.00

11.00

545.45%

273.68%

PAT

36.00

20.00

6.64

442.17%

80.00%

EPS (₹)

11.09

6.18

1.90

483.68%

79.45%

What is Management Promising in the Coming Quarters?

Management has maintained an optimistic posture, pointing to higher domestic capacity utilization and rising export realizations in the high-voltage segment as structural tailwinds. During recent interactions, leadership outlined plans to fully operationalize the new subsidiary, Modison Hitech Pvt Ltd, aimed at diversifying into advanced Nickel and Nickel alloy products.

However, they admitted that the capital structure would continue to bear the weight of higher short-term funding lines to protect against wild commodity swings. Margins that expand violently because of low-cost inventory positioning can compress just as fast when spot prices reverse course.

Would you celebrate an enterprise that doubles its revenue if it takes six times the amount of bank debt to move the inventory out the door?

Section 5 — Valuation Discussion: Fair Value Range Only