Prime Cable Industries FY26: A 67% Topline Jump, an SME Listing, and the Heavy Drama of a Negative Operating Cash Flow

1. At a Glance

A stunning ₹234.88 crore in revenue headlines the financial year 2026 performance for this freshly listed manufacturer. This marks a massive 66.58% growth over the previous year’s ₹140.84 crore. This aggressive expansion represents a multi-year pivot away from local tender execution toward state-level grid infrastructure and specialized engineering contracts. Profitability mirrored this trajectory, with net profit leaping from ₹7.50 crore to ₹12.24 crore. Yet, beneath this high-voltage growth engine lies a critical working capital imbalance that demands close scrutiny.

Trade receivables expanded aggressively to ₹70.52 crore. This stretch in payment timelines has pushed the cash conversion cycle out to 81 days. Consequently, operating cash flow turned deeply negative at -₹13.21 crore. This divergence demonstrates that rapid topline growth can heavily stress liquidity if cash collections lag execution.

While a successful ₹38 crore public listing on the National Stock Exchange SME platform in late 2025 replenished the cash reserves, the business remains closely tied to institutional capital expenditure. The unexecuted order book provides strong near-term revenue visibility. However, managing raw material pass-throughs alongside a highly capital-intensive manufacturing cycle will determine if this operational scale translates into real wealth for shareholders.

2. Introduction

Prime Cable Industries Limited has come a long way since its inception in 1997 as a small industrial proprietorship in Delhi. Over nearly three decades, the business has systematically transitioned from basic wire drawing to producing complex low-tension power, control, and aerial bunched cables under its proprietary brands.

The company entered a new corporate era on November 18, 2025, when its shares officially listed on the NSE Emerge platform after a highly anticipated public offering. Operating via two production hubs in Delhi and Rajasthan, the business has capitalized on domestic infrastructure spending. The fresh capital infusion was intended to fund a capital expenditure program, reduce outstanding debt, and support working capital requirements. Management is now looking to move further up the product value chain while widening its geographic reach outside its traditional northern strongholds.

3. Business Model: WTF Do They Even Do?

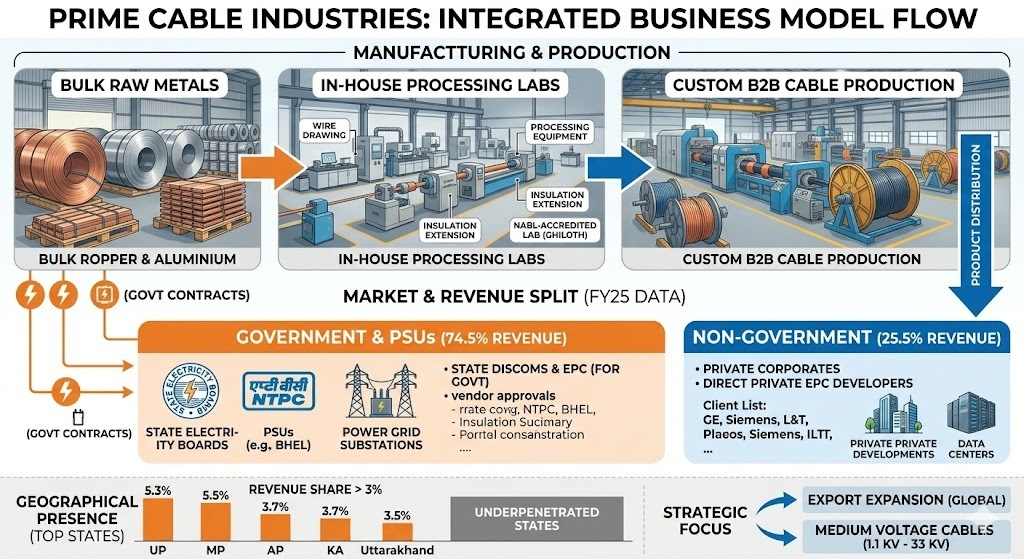

At its core, the company converts bulk copper and aluminium into heavily insulated industrial cabling systems designed to transmit electricity without turning into spontaneous fire hazards. Instead of competing in the chaotic retail retail space against legacy consumer giants, the business operates entirely in the institutional B2B segment.

The company runs a customized, made-to-order assembly line. Its product mix is heavily weighted toward control cables and low-tension power cables. These are sold directly to state electricity distribution utilities or engineering, procurement, and construction contractors working on public infrastructure projects.

The underlying economic reality is that the company functions as a direct play on government utility spending. Government entities and public sector undertakings directly account for 74.5% of total sales. While the company serves 129 distinct institutional customers, 74 repeat accounts generate nearly 70% of total revenue. This structural reliance creates excellent order stickiness, but it also means the balance sheet is permanently exposed to the payment cycles of state bureaucracy.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Headline Results Table

Metric

Latest Period (FY26)

YoY Change (%)

Revenue from Operations

₹234.88

+66.58%

EBITDA

₹23.41

+60.34%

Profit Before Tax (PBT)

₹16.49

+58.71%

Profit After Tax (PAT)

₹12.24

+63.20%

Reported EPS (₹)

₹6.68

+22.34%

Note: EBITDA is calculated as PBT (₹16.49 cr) + Interest (₹4.48 cr) + Depreciation (₹1.44 cr). Reported EPS is based on the year-end adjusted share count of 1.83 crore shares.

The income statement shows strong revenue acceleration, with the topline jumping to ₹234.88 crore from ₹140.84 crore a year prior. This volume-driven growth expanded operating profits to ₹23.41 crore. However, operating margins softened slightly to 9.97% due to rising raw material input costs. Profit after tax grew to ₹12.24 crore despite a non-recurring professional and advisory expense of ₹2.00 crore incurred during the public market restructuring.

What is Management Promising in the Coming Quarters?

During the post-earnings briefing, management outlined an ambitious goal of maintaining a 40% to 45% compound annual growth rate over the next two fiscal years. Growth is expected to be supported by the commissioning of their upcoming Unit 3 facility in Ghiloth, Rajasthan. This plant will specialize in higher-margin medium-voltage cables up to 33 kV.

The transition to medium-voltage products is expected to expand long-term EBITDA margins, as these products command yields of 12.5% to 13% compared to low-tension options. For the upcoming fiscal year, management has guided for steady EBITDA margins between 10% and 11%, noting that volume contributions from the new facility will ramp up gradually following initial trial runs.

5. Valuation Discussion: Fair Value Range Only

1. Trailing P/E Method

The company reports a trailing EPS of ₹6.68 for FY26 based on its expanded post-IPO share base of 1.83 crore shares. Looking across the broader electrical manufacturing peer universe, listed cable entities command a median price-to-earnings multiple of approximately 28.1x. However, secondary tier players and small-cap infrastructure suppliers typically trade at a discounted peer band between 14.0x and 18.0x. Multiplying the trailing EPS of ₹6.68 by this benchmark multiple range yields an implied equity value bracket between ₹93.52 and ₹120.24 per share.

2. EV/EBITDA Method

For FY26, the calculated EBITDA stands at ₹23.41 crore. Given a current market capitalization of ₹195.70 crore, total borrowings of ₹51.55 crore, and a cash cushion of ₹12.87 crore, the enterprise value calculates to ₹234.38 crore. This places the trailing EV/EBITDA multiple at 10.01x. Applying a conservative infrastructure equipment multiple range of 9.0x to 11.5x to the operating profit implies an enterprise value range of ₹210.69 crore to ₹269.22 crore. Adjusting for net debt brings the implied per-share valuation range to ₹93.94 to ₹125.92.

3. Simplified Discounted Cash Flow (DCF) Approach

Assuming a multi-year cash flow forecast anchored on management’s guided revenue growth target of 45% for the next two years, followed by a normalized terminal growth rate of 5.0%, a cost of capital of 12.5% is applied. Factoring in a continuing working capital drag of 15.0% of incremental sales to account for state utility receivables yields an estimated intrinsic equity value range between ₹91.10 and ₹118.50 per share.

Combined Valuation Range

By blending these quantitative methodologies, we establish a structural fair value range for the equity:

[Conservative Floor] ₹91.00 ═══════════◯═══════════ ₹125.00 [Optimistic Ceiling]

Current Price: ₹106.80

Fair Value Disclaimer: This fair value range is for educational purposes only and is not investment advice.

6. What’s Cooking: News, Triggers, Drama

The SME Milestone: The company officially transitioned from a closely held family operation to a publicly traded entity on November 18, 2025, raising ₹38.00 crore in gross proceeds via its fresh issue.

The Largest Single Win: In April 2026, the company secured its largest individual