Welspun Corp FY26: A ₹25,350 Crore Order Book Flex Proves Big Pipes Mean Big Profits

Section 1 — At a Glance

Welspun Corp Limited has concluded the financial year 2026 by establishing a profound baseline of operational outperformance, decoupling itself from standard infrastructure cyclicality. The headline metric capturing investor attention is a monumental consolidated order book of ₹25,350 Cr, providing revenue visibility stretching cleanly into FY28. This performance is punctuated by a full-year EBITDA of ₹2,371 Cr, soundly outstepping the management’s prior market guidance of ₹2,200 Cr. Simultaneously, full-year normalized net profit surged to ₹1,613 Cr, displaying a 42% expansion year-on-year when adjusted for previous non-recurring exceptional windfalls.

Yet, beneath these highly visible corporate milestones lie structural variables requiring analytical vigilance. The business executed a massive asset-heavy capital expenditure program of ₹2,532 Cr during the year, highlighting its aggressive commitment to global capacity expansion. While the balance sheet successfully retained a robust net cash buffer of ₹1,627 Cr, the underlying working capital lifecycle is structurally deeply negative. This liquidity architecture remains heavily reliant on significant, upfront customer advances rather than pure-play programmatic cash conversion cycles.

True capital efficiency is measured by a company’s ability to extract premium pricing from capacity additions before macro cycles inevitably turn. While current returns on capital appear highly optimized, the operational overhang of domestic structural overcapacity in secondary segments like ductile iron pipes looms quietly in the background.

Section 2 — Introduction

Welspun Corp has spent the last few financial years attempting to shed its traditional, hyper-cyclical skin. Long regarded by the street as merely a seasonal fabricator of massive steel tubes for oil and gas projects, the corporate entity has fundamentally pivoted towards a multi-layered building materials and specialized infrastructure model.

The strategic roadmap shifted gears aggressively with the landmark acquisition of Sintex-BAPL for ₹1,251 Cr in 2023, instantly buying the group a direct, high-margin pathway into the domestic consumer plastic water storage and polymer piping space. Following that up, the company absorbed specified assets of ABG Shipyard to anchor heavy manufacturing capacities, while systematically funding massive internal greenfield and brownfield buildouts in the United States, Saudi Arabia, and domestic hubs. As these disparate manufacturing projects approach operational maturity, Welspun is transitioning into a structural engineering conglomerate operating across six continents.

Section 3 — Business Model: WTF Do They Even Do?

If you think Welspun Corp simply makes ordinary plumbing pipes, your portfolio is in grave danger. The company essentially operates a high-stakes heavy engineering model designed to evacuate oil, gas, and massive volumes of water across global geographies.

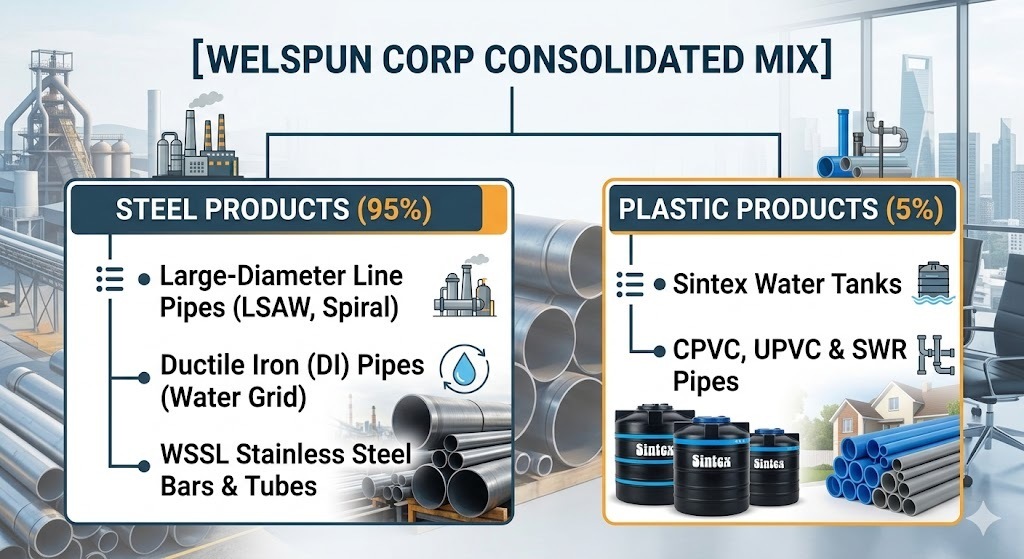

The core engine is the Steel Products division, accounting for a dominant 95% of current business volumes. This isn’t commodity steel; it is a specialized line-pipe setup focusing on high-grade Longitudinal Submerged Arc Welding (LSAW), Helically Submerged Arc Welding (HSAW), and Electrical Resistance Welded (ERW) configurations. These are the literal arteries running beneath deserts and oceans. To hedge against the terrifying volatility of global oil exploration capex, the group built out a secondary tier: Ductile Iron (DI) pipes for urban water grids, high-integrity TMT Rebars for structural concrete, and an integrated stainless-steel play via Welspun Specialty Solutions Ltd (WSSL).

The remaining 5% of the business belongs to the Plastic Products division, spearheaded by the ubiquitous Sintex brand. Here, they manufacture consumer water storage tanks and have recently bolted on Weetek Plastics for ₹85 Cr to pump out CPVC and UPVC building fixtures. It is an industrial balancing act: selling custom multi-million-dollar cross-country pipelines to sovereign entities on one hand, while distributing standard plastic water tanks to neighborhood hardware stores on the other.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Performance Trend Table

Metric

Q4FY26

Q4FY25

YoY (%)

QoQ (%)

FY26 Full Year

Revenue from Operations

4,313

3,925

9.89%

-4.83%

16,770

EBITDA

539

502

7.37%

-12.50%

2,371

Profit After Tax (PAT)

370

698

-47.00%

-18.86%

1,613

Reported EPS (₹)

14.04

26.62

-47.26%

-18.18%

61.15

The headline earnings drop in Q4 is an accounting optical illusion that sent short-term algorithmic traders into a brief panic. The Q4FY25 baseline was artificially inflated by a massive one-time cash injection of ₹477 Cr derived from selling their stake in Nauyaan Shipyard. Strip out that corporate housekeeping, and the real core business performance looks significantly more robust. Core underlying PAT without exceptional items actually expanded by a very healthy 28% for the quarter.

The real driver here is the quality of the earnings mix. It is an ironclad rule of heavy manufacturing that operational leverage is a double-edged sword: high utilization yields exponential margin gains, while empty factories destroy capital. Welspun managed to expand its consolidated full-year EBITDA margins to a sleek 14.0%, up from 13.1% in FY25, by consciously prioritizing high-value, bespoke international orders over low-margin local utility bidding wars.

What is Management Promising in the Coming Quarters?

During the May 2026 earnings conference, the executive leadership did not hold back on confidence, handing out an explicit FY27 revenue target of ₹20,000 Cr alongside an EBITDA guidance of ₹2,850 Cr. When analysts probed if an entirely booked out facility structure until FY28 caps their near-term financial upside, the CEO noted:

“All of our plants are almost booked till FY 2028… [but] at Welspun, we will never let go of a very profitable opportunity.”

Management confirmed they have intentionally held back a slice of large-diameter spot capacity across their global footprint. This unbooked production real estate is specifically reserved