Electrotherm (India) Ltd FY26: The Illusion of a ₹13.63 Crore Profit Meets a Hidden ₹1,407.64 Crore Reality

Section 1 — At a Glance

Electrotherm (India) Ltd presents a classic case study in financial structural complexity. On paper, the consolidated headline figures indicate a net profit of ₹13.63 crore for the final quarter of the financial year 2025-26, ending March 31, 2026. However, this reported figure operates under severe accounting qualifications. Over a multi-year horizon, the company has undergone substantial debt adjustments, with reported borrowings declining from ₹2,293.70 crore in FY20 down to ₹1,063.55 crore by the close of FY26.

The primary area of operational and financial concern centers on the company’s non-provision of interest expenses on several loan accounts categorized as Non-Performing Assets (NPAs) by its lenders. According to the independent auditor’s report, unprovided interest for the fiscal year amounted to approximately ₹194.99 crore on a consolidated basis. Cumulatively, the total unprovided interest standing outside the balance sheet has reached a staggering ₹1,407.64 crore.

When adjusted for these unprovided obligations, the company’s reported financial position faces a significant correction, turning its apparent nominal equity into a deeply negative net worth configuration. For investors assessing structural risk, the divergence between operating performance and absolute structural liability remains a critical focal point.

True economic liability cannot be erased by accounting omission; when unprovided interest outpaces market valuation, the reported net profit functions merely as an operational abstraction.

The ultimate path forward depends on the final resolution of ongoing debt restructuring and pending judicial evaluations.

Section 2 — Introduction

Electrotherm (India) Ltd, established in 1983, has built its engineering reputation on designing industrial furnace systems and manufacturing steel products. Headquartered in Gujarat, the company expanded beyond heavy engineering into manufacturing special steel products, ductile iron pipes, and a minor venture into electric two-wheelers.

While its operational footprint remains visible in heavy industrial clusters, Electrotherm’s corporate narrative over the last decade has been dominated by extreme leverage, severe banking defaults, and continuous legal engagements with investigative agencies and asset reconstruction companies. The business continues to navigate a delicate path, trying to generate enough operating cash flow from its furnaces to survive under an immense mountain of legacy defaults.

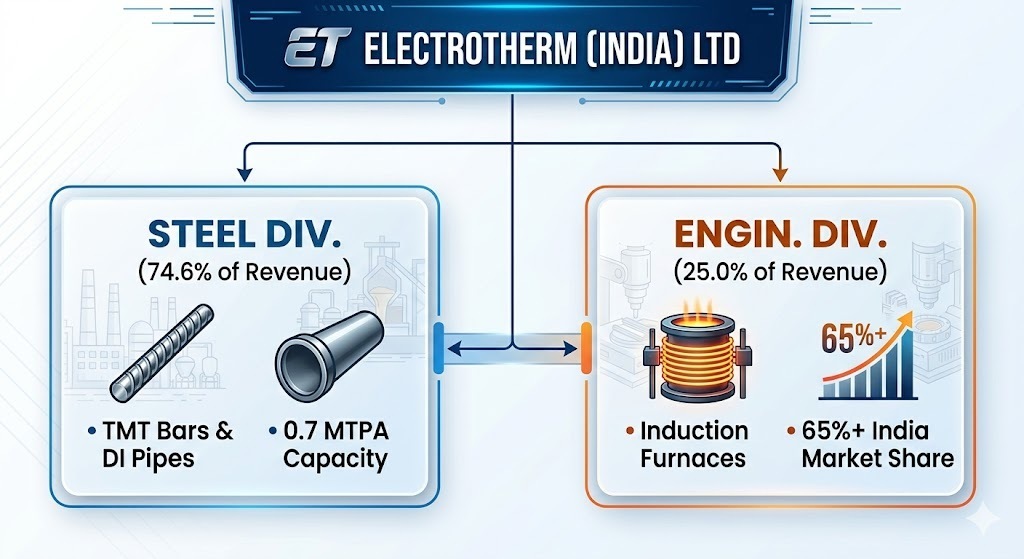

Section 3 — Business Model: WTF Do They Even Do?

Electrotherm operates a business model that looks like someone tried to combine a heavy industrial engineering firm with a steel plant, and then added an electric scooter hobby in the garage just for laughs.

The core engines driving this machinery include:

Special Steel Division: Contributing 74.6% of operational revenues, this segment manufactures TMT bars and ductile iron (DI) pipes at its 0.7 MTPA facility in Kutch. It keeps the lights on by supplying infrastructure projects.

Engineering and Technologies Division: The historic crown jewel, commanding a 65%+ domestic market share in induction melting equipment. It makes the massive furnaces that other steelmakers use to melt metal.

Electric Vehicle Division: Operating under the brand name YoBykes, this unit represents a microscopic 0.4% of revenues. It serves as a nostalgic reminder of the early 2000s low-speed EV era, quietly watching its sales contract by 20% in recent years while the rest of the world entered an EV boom.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Headline Results Performance

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

₹1,139.99

-1.82%

+26.13%

EBITDA / Operating Profit

₹24.50

-81.28%

-180.0%

PAT

₹13.63

-92.65%

-138.5%

Reported EPS (₹)

₹10.70

-92.65%

-138.5%

Concall Handling & Management Outlook

While a formal concall transcript was omitted, management explicitly laid out its state of affairs in the statutory disclosures. The board acknowledged defaulting on a principal payment of ₹24.00 crore and interest obligations of ₹4.68 crore to Invent ARC during the year.

Meanwhile, they have requested an extension from Edelweiss ARC for a final instalment