Bodal Chemicals FY26: A ₹27 Crore Tax-Free Gift from Punjab Barely Covers the Cost of Building a Benzene Empire

At a Glance

Bodal Chemicals concluded FY26 with an apparent operational recovery, reporting a 14.8% expansion in multi-year consolidated revenue to ₹2,012.24 crore. However, this expansion was significantly augmented by a ₹26.98 crore state incentive booked as operating income under the Punjab Industrial Incentive Scheme. Behind the headline expansion lines lies a complex web of structural shifts, highly capital-intensive projects, and mounting overhead costs.

While annual consolidated net profit expanded by 158.5% to ₹47.83 crore, it must be viewed against the multi-year cyclical low of FY24. Profitability continues to be hindered by substantial depreciation and finance costs stemming from the greenfield Saykha benzene downstream venture. Operating margins are heavily exposed to international trade disputes and severe structural headwinds within the domestic chlor-alkali market. Debt optimization has commenced via non-core asset liquidations, yet structural capital efficiency indicators remain constrained.

Introduction

Bodal Chemicals Limited is an established chemical manufacturing corporate headquartered in Ahmedabad. Over three decades of operations, it has built a business model integrated across dyestuffs, dye intermediates, and basic chemical chains.

The corporate strategy is focused on moving away from highly volatile textile-dependent chemical commodities toward highly specialized downstream derivatives. The practical execution of this shift has introduced financial friction, as the commissioning of heavy infrastructure brings fixed costs online well ahead of volume scale-up.

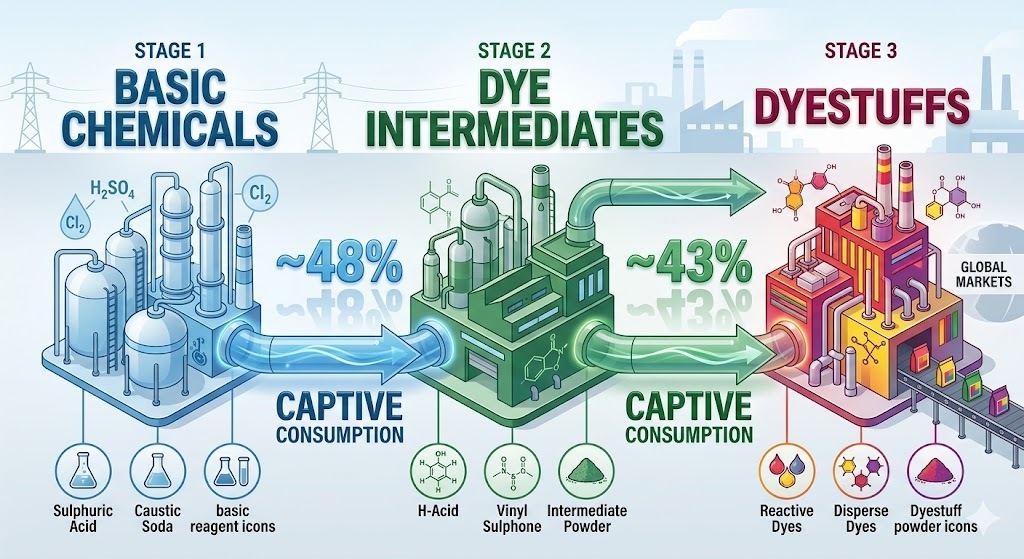

Business Model: WTF Do They Even Do?

Bodal is essentially a massive chemical assembly line where one division’s waste or output is another division’s primary raw material. It controls roughly 20% of the domestic market share for dye intermediates and 13% for dyestuffs, feeding global supply chains for textiles, leather, and paper.

To protect itself from wild raw material price swings, management expanded into chlor-alkali by buying a massive facility in Punjab. They also built India’s only domestic manufacturing facility for Trichloroisocyanuric Acid (TCCA), a water treatment chemical, and built a massive, ₹300 crore revenue-potential benzene downstream plant at Saykha. When functioning perfectly, this horizontal and backward integration provides a cost advantage. When global demand stumbles, it means they are running a multi-million-rupee manufacturing machine at less than half its capacity, turning fixed infrastructure costs into a drag on earnings.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4 FY26)

YoY change (%)

QoQ change (%)

Revenue

₹588.02

30.4%

20.1%

EBITDA

₹68.56

173.0%

211.1%

PAT

₹32.06

1,471.6%

13,258.3%

EPS

₹2.55

1,493.8%

12,650.0%

Dynamic adjustments to volatile input costs are critical to preserving mid-cycle absolute margins when absolute end-demand volume cycles compress.

Did Management Walk the Talk?

During the August 2025 concall, management downsized its near-term expectations for the new Saykha benzene division, cutting the FY26 asset turnover target from ₹150 crore to ₹100 crore due to protracted verification and qualification cycles with pharmaceutical end-customers. They guided for a recovery in utilization from 20% to over 70% by the second half of the year.

The Q4 financial prints demonstrate that while topline volumes scaled up significantly, intense regional pricing matches and elevated raw material indices compressed the segment’s margin realization. Deleveraging progressed inline with guidance through targeted asset liquidations, including the complete closure and sale of inoperative legacy units.

Valuation Discussion: Fair Value Range Only

To evaluate Bodal Chemicals, we apply three distinct methodological lenses anchored against normalized multi-year operational data. The corporate has 12.59 crore adjusted equity shares outstanding.