D.P. Abhushan FY26: The 20% Volume Meltdown Behind a ₹4,070 Crore Glittering Facade

Section 1 — At a Glance

A dramatic decoupling between financial value and physical reality defined the fiscal year 2026 for D.P. Abhushan Limited. On paper, the retail jewellery chain delivered a glittering performance, breaching the milestone of ₹4,000 crore in annual revenue and staging an 88% year-on-year surge in net profit. Headline metrics suggest absolute regional dominance, with store footprint expanding and operating efficiency apparently rising to new heights. Yet, beneath this polished exterior lies a stark operational reality that has sparked intense investor anxiety: a severe 20% contraction in overall sales volumes.

The entirety of the company’s growth was engineered by price inflation rather than transactional traction. As global gold prices escalated to unprecedented levels, retail consumers pulled back sharply on volume consumption, forcing the company to rely on inventory revaluation gains and value-driven ticketing to inflate its financial statements. At the same time, the aggressive building out of new physical showrooms has triggered structural strains across the balance sheet. Operating cash flows have plunged deeper into negative territory, and working capital intensity has risen dramatically as millions of rupees remain locked up in static floor stock. While the market evaluates the stock at a remarkably compressed valuation relative to national peers, the core conflict remains unresolved: a business can mask volume weakness through price hikes only for so long before inventory carrying costs catch up with the profit and loss statement. Earnings growth that relies on the escalation of commodity prices rather than transactional velocity is inherently fragile. Investors are now forced to weigh a spectacular margin expansion against a cash-bleeding corporate model.

Section 2 — Introduction

D.P. Abhushan Limited occupies a unique, hyper-regionalized niche within India’s discretionary retail landscape. Tracing its operational lineage back over eight decades under the heritage banner of ‘DP Jewellers’, the company has historically anchored its operations in Madhya Pradesh and Rajasthan. Unlike national behemoths that rely on massive corporate marketing apparatuses, this tier-2 and tier-3 operator relies on deep generational customer loyalty, where jewellery is treated as an essential financial asset and a cultural necessity rather than casual fashion.

The corporate journey from a traditional family partnership into a modern public entity culminated in its recent migration and listing on the main board of the Bombay Stock Exchange on April 15, 2024. This listing was intended to usher in an era of rapid institutionalized growth. Management set into motion an aggressive expansion blueprint, aiming to transform a localized family operation into a multi-state retail network spanning Gujarat, Maharashtra, and Chhattisgarh. However, executing this strategy in a highly volatile macroeconomic environment has forced a delicate balancing act. The company must seed capital into massive new company-owned showrooms while navigating a severe gold price regime that threatens the purchasing power of its core middle-class consumer base.

Section 3 — Business Model: WTF Do They Even Do?

At its core, D.P. Abhushan runs a remarkably simple yet capital-devouring retail pipeline: they sell weight disguised as art. The company’s revenue mix is overwhelmingly skewed toward traditional gold jewellery, which commands a staggering 92% of total sales. Diamond-studded jewellery chips in a modest 6%, while silver accounts for the remaining 2% baseline.

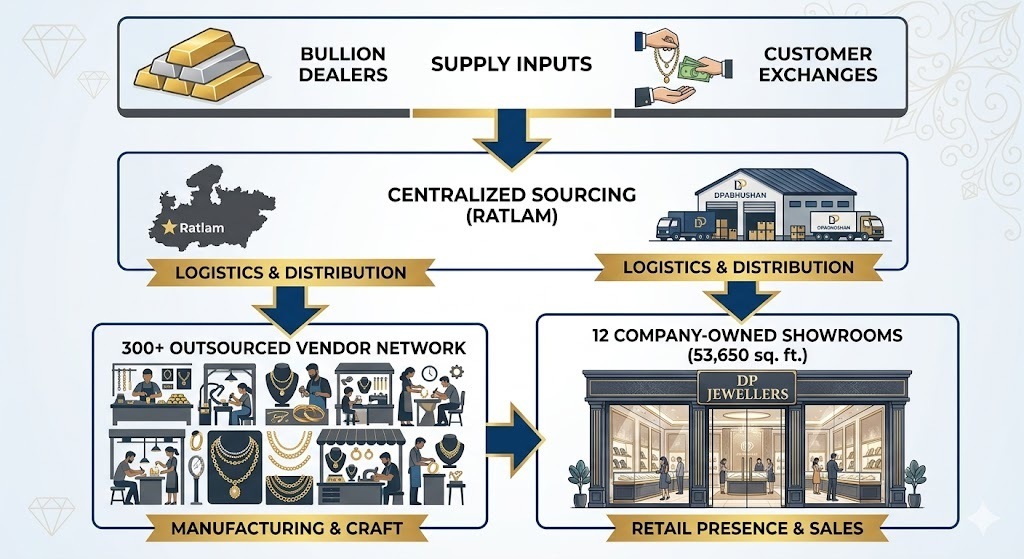

The operation completely eliminates manufacturing risk by outsourcing the actual crafting of its portfolios to a nationwide network of more than 300 third-party goldsmiths and specialized vendors. This leaves management free to focus entirely on its real core competency: managing a massive logistics wheel. Sourcing is entirely centralized at its corporate headquarters in Ratlam, from where inventory is dynamically shuffled across 12 operational showrooms spanning a tight 300-kilometer geographic radius.

To keep customer walk-ins from walking out empty-handed, the company utilizes an inventory-heavy strategy, stuffed with physical stock to drive a footfall conversion rate of 82.38%. Operating primarily in lower-tier cities allows the company to secure depressed rental and overhead structures, but it also tethers their fate entirely to traditional wedding-driven demand, which commands 60% of total company sales. It is an asset-heavy, design-centric model that functions excellently when gold is cheap and transactional velocity is high—but turns into a gilded cage when commodity costs turn erratic.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly and Annual Performance Trajectory

Metric

Q4 FY26

YoY (Q4)

QoQ

Full Year FY26

YoY (Full Year)

Revenue

1,338.89

86.57%

9.53%

4,070.33

22.88%

EBITDA

72.99

72.19%

-30.90%

309.67

77.43%

PAT

50.60

101.19%

-31.02%

211.84

87.97%

Reported EPS (₹)

22.17

101.18%

-31.02%

92.80

86.61%

The final quarter of the fiscal year showcased an explosive headline acceleration, with revenue expanding 86.57% year-on-year to hit ₹1,338.89 crore. Full-year profit after tax surged to ₹211.84 crore, representing an extraordinary step-up in profitability that comfortably outpaced raw top-line growth. This margin expansion was explicitly driven by a non-recurring tailwind: massive inventory gains. Because the company held a deep well of lower-cost gold stock when global bullion market values skyrocketed, approximately 28% to 30% of these paper inventory gains flowed directly into the reported financials, masking the underlying volume distress.

Did Management Walk the Talk?

Reviewing historical management commentary reveals a significant pivot in corporate posture. In prior quarters, leadership confidently broadcasted an uncompromised multi-state retail rollout, promising to aggressively seed new stores across new geographies. Instead, actual physical execution cooled significantly, ending the year with 12 operational showrooms.

During the latest investor interactions, management openly addressed this tactical deceleration. The CEO noted that expansion had been intentionally “slowed down due to the current scenario,” confessing that multiple planned store openings had been deferred by one to two