International Gemological Institute Limited (India) Mar 2026: 74% Operating Margins on a 16.45 Million Volume Flex

1. At a Glance

The structural architecture of the global diamond trading network requires absolute, uncompromised verification systems. International Gemological Institute Limited (India) occupies a dominant bottleneck position within this framework, translating volume verification metrics into a highly optimized cash machine. The company operates as a critical, high-margin validation engine for both natural and laboratory-grown diamonds across major global cutting and distribution hubs.

As the industry undergoes a permanent transition toward institutional scale, product traceability, and SKU-level disclosure, the structural value of third-party certification has expanded from an optional luxury to an absolute regulatory and consumer compliance mandate.

Earnings performance for the 15-month period ending March 31, 2026, details total consolidated operational revenue reaching ₹1,597.6 crore, accompanied by an exceptionally strong Group EBITDA of ₹972.8 crore, highlighting a 61% core operating margin profile. Total report certification processing volumes expanded to 16.45 million units globally. Consolidated profit after tax reached ₹711.2 crore.

Concurrently, the standalone operation in India recorded a 24% revenue expansion to ₹1,233.9 crore, carrying an EBITDA performance of ₹919.8 crore at a 73.4% segment margin. However, extreme market premium structures and high capital concentration levels are clearly visible. The current valuation multiples reflect a scenario assuming flawless long-term volume expansion.

Exceptional capital efficiency metrics within narrow market niches are structurally protected only if the absolute control over distribution channels remains unchallenged by institutional market counter-strategies.

2. Introduction

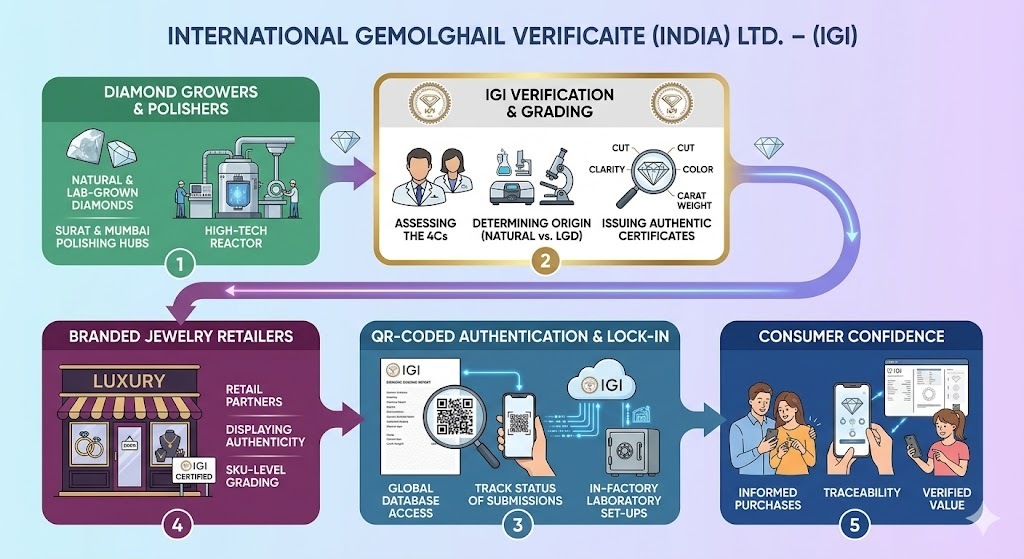

International Gemological Institute Limited (India)—formerly known as International Gemmological Institute (India) Limited—occupies an exceptionally lucrative position in the financial landscape. The company does not mine diamonds, grow diamonds, or retail jewelry. It sits in the middle as an asset-light, premium-priced border checkpost. It collects fees to confirm that a stone is shiny, properly cut, and structurally authentic.

Control of the equity resides with private equity giant Blackstone, which maintains a 76.55% controlling stake through Bcp Asia II Topco Pte Ltd. The business model transforms complex mineralogy into a scalable, high-volume production line.

The corporate financial architecture has recently been modified. The company transitioned its reporting calendar from a traditional January–December cycle to the standard Indian April–March fiscal format. This transition has generated a prolonged 15-month reporting framework ending March 2026. The structural numbers show that while global luxury consumption patterns experience persistent cyclical fluctuations, the institutionalization of the diamond verification value chain has created a resilient, non-discretionary recurring volume stream for the leading independent certification networks.

3. Business Model: WTF Do They Even Do?

To the uninitiated, diamond grading sounds like a boutique, artisanal craft practiced by elderly scholars looking through loupes in dimly lit backrooms. IGI has thoroughly exploded that myth. This is a high-throughput, factory-grade industrial operation that treats diamond certification with the automated velocity of a tech assembly line.

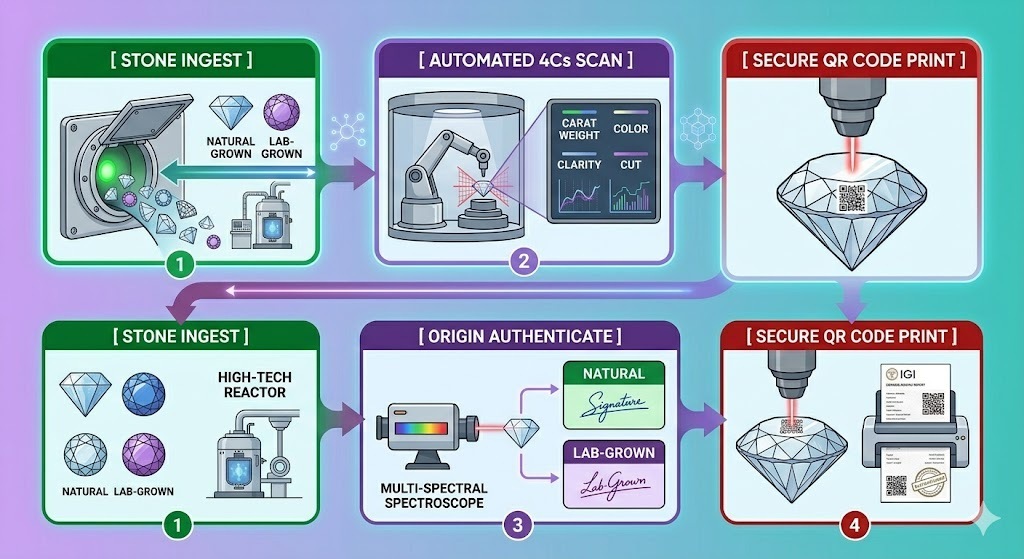

The corporate mechanism is beautifully straightforward. IGI takes a diamond or a piece of studded jewelry, subjects it to specialized spectrographic analysis to check the 4Cs (Carat, Color, Cut, Clarity), and appends a QR-coded certificate verifying its precise origin—explicitly distinguishing between natural stones and laboratory-grown variants. This origin check is where the entire economics of the sector now resides.

The global footprint spans 31 modern laboratory branches across 10 countries alongside 18 specialized educational centers. The core revenue engines are split across clear operational vectors:

Laboratory-Grown Diamonds (LGD): The undisputed volume monster, driving approximately 59% of structural revenues.

Natural Diamonds (ND): The traditional, high-realization segment contributing roughly 19%.

Education & Auxiliary: The remaining 2% from schools of gemology and related institutional income.

The fundamental genius of the model lies in its integration with modern manufacturing workflows. IGI sets up laboratory installations directly within the factory facilities of large lab-grown diamond producers in industrial hubs like Surat. By embedding its own graders inside the client’s physical ecosystem, IGI secures exclusive lock-in over structural logistics. The diamond comes out of the microwave reactor, gets polished, steps right into the IGI cubicle, and leaves with a birth certificate.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Headline Performance Metrics

Metric

Latest Quarter (Jan-Mar 2026)

YoY Change (%)

QoQ Change (%)

Revenue from Operations

₹368.60

21.0%

49.2%

EBITDA / Operating Profit

₹236.00

21.0%

37.4%

Net Profit (PAT)

₹179.60

27.7%

36.6%

Reported EPS (₹)

₹4.16

27.6%

36.4%

Note: For sequential comparison, the previous quarter refers to the Dec 2025 period extracted from the standalone trend data, while latest quarter reflects consolidated income statement actuals. Standalone March 2026 Operating Profit is ₹219.75 cr vs ₹171.73 cr in Dec 2025.

The sequential revenue jump of 49.2% over the previous quarter highlights an extraordinary operational sprint, comfortably outpacing long-term averages. Core operating margins remained remarkably steady at 64% for the quarter, showcasing strong pricing power and excellent cost control.

A structural mismatch between volume expansion and absolute top-line revenue trajectory is the first definitive signal of changing product mix configurations within a high-volume processing ecosystem.

What is Management Promising in the Coming Quarters?

During recent executive briefings, management detailed a highly expansionary operational outlook. A primary strategic pillar is the completion and full commissioning of the major 214,159 square foot laboratory complex in Surat. This massive infrastructure expansion significantly enhances IGI’s aggregate processing throughput.

Furthermore, the executive team emphasized that lab-grown diamond producers are systematically doubling their reactor footprint over