Control Print Ltd March 2026: The 83% Quarterly Profit Melt That Exposed Italy’s Machine

Section 1 — At a Glance

Control Print Ltd’s final quarter of the fiscal year 2026 brought a stark reminder of the costs of rapid global expansion, as consolidated net profit plunged by 83.21% to ₹11.19 crore, down from ₹66.64 crore in the corresponding quarter of the previous year. While top-line momentum remained firmly intact with quarterly consolidated revenue rising 14.58% to ₹139.87 crore, the sharp divergence between volume growth and bottom-line delivery has severely tested investor expectations. The core domestic coding and marking segment continues to show exceptional resilience, but aggressive outlays in overseas technology acquisitions have created an expensive operational drag that is masking the underlying strength of the Indian business.

Investor attention is currently fixed on two opposing forces: the compounding stability of the domestic annuity model versus the execution bottlenecks in the newly absorbed packaging architectures. The company’s domestic installed base has steadily expanded to over 23,000 industrial printers, ensuring a highly profitable and captive stream of recurring consumables, spares, and service revenues. However, the ambitious operational overhaul at its Italian subsidiary, CP Italy S.r.l., has hit severe friction. Delayed machine dispatches, uncapitalized research and development expenses, and localized engineering field trials have collectively compressed consolidated operating margins. Diversification frequently demands a heavy near-term toll before yielding operational scale. The market is now aggressively factoring in these international deficits, presenting an intricate puzzle of a robust domestic engine paired with a fragile global expansion template.

Section 2 — Introduction

Control Print Ltd (CPL), incorporated in 1991, has spent over three decades evolving from a basic industrial hardware supplier into India’s premier integrated coding, marking, and localized tracking solutions provider. Operating out of its dedicated manufacturing hubs in Nalagarh and Guwahati, CPL stands out as the only domestic manufacturer of scale operating within an industrial ecosystem traditionally dominated by multinational corporations.

The company has entered a critical strategic pivot point. CPL has transformed its corporate structure by orchestrating a string of targeted international acquisitions—including Markprint BV in the Netherlands, Codeology Group in the UK, and the distressed asset purchase of V-Shapes packaging technology in Italy. These moves are explicitly designed to transition CPL from a pure equipment manufacturer into a high-value global supply chain data layer. This article evaluates whether management’s long-term infrastructure bets can successfully cross the financial finish line, or if the current operational leakages in Europe will permanently dilute the company’s historically superior domestic return profile.

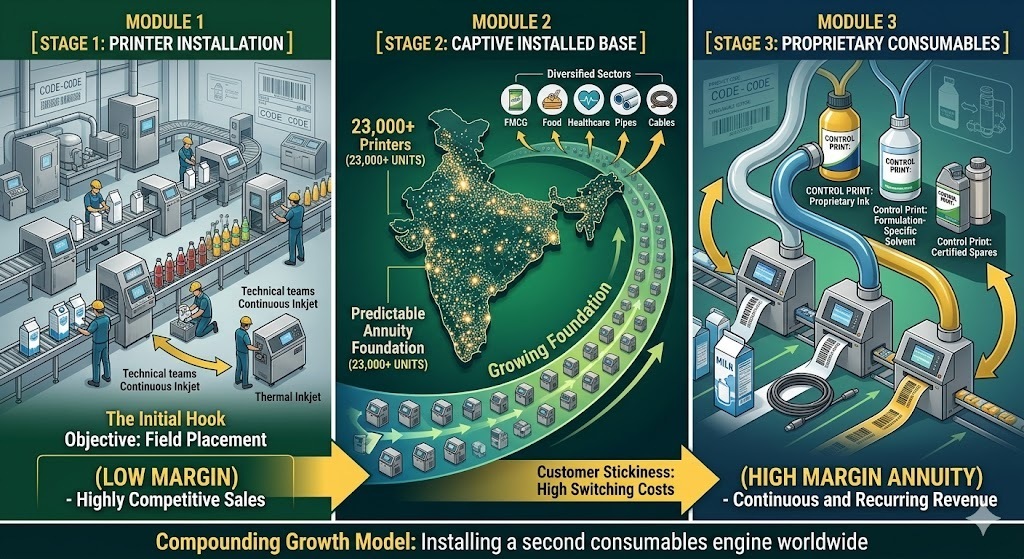

Section 3 — Business Model: WTF Do They Even Do?

To understand Control Print, you must look past the heavy industrial printers they build and focus on what flows out of them. CPL operates a classic razor-and-blade business model. The company designs, installs, and services complex industrial printing engines—including Continuous InkJet (CIJ), Thermal Inkjet (TIJ), and Laser Coders—across diverse manufacturing lines. However, the initial sale of these machines is merely a hook to achieve field placement.

Once a machine is embedded into a high-speed production line at a cement plant, a dairy cooperative, or a pharmaceutical packaging line, it becomes structurally locked. CPL’s printers are engineered to run exclusively on formulation-specific, proprietary consumables like specialized inks, solvents, and cartridges. Third-party alternatives are barred by technical constraints, creating a high-margin, sticky annuity stream that generates predictable cash flows across the entire 7-to-10-year operating lifecycle of the printer. With a growing domestic installed base exceeding 23,000 units, the company effectively operates an industrial print-on-demand utility network.

The headline financial numbers tell a tale of structural divergence. Top-line demand remains strong, with quarterly consolidated revenue growing 14.58% year-on-year to ₹139.87 crore. Consolidated operating efficiency also showed brief signs of life, as quarterly operating profit climbed 18.82% to ₹26.27 crore. However, net profitability suffered a severe hit. The dramatic 83.21% year-on-year plunge in quarterly PAT to ₹11.19 crore was heavily exacerbated by a sharp base distortion: in the prior-year quarter (March 2025), CPL recognized a massive, one-time Minimum Alternate Tax (MAT) credit entitlement of ₹45.36 crore, which artificially inflated past net profits. When a corporate bottom line becomes dependent on tax accounting anomalies rather than