GTV Engineering FY26: The 26.3% ROE Smallcap Quietly Buying Out Its Ecosystem

Section 1 — At a Glance

GTV Engineering Limited concluded the fiscal year ending March 31, 2026, with an extraordinary surge in core operational efficiency. Net profit climbed to ₹14.22 crore, up from ₹11.05 crore in the prior year, despite standard operating revenues staying largely flat at ₹101.52 crore. The engineering firm’s bottom-line stability was anchored by a sharp drop in material consumption costs, which fell from ₹77.51 crore to ₹75.12 crore, expanding operating margins significantly.

Here is the FY26 At a Glance metrics converted into a clean markdown table format:

Financial Metric

Value

Revenue from Operations

₹101.52 Crore

Net Profit after Tax (PAT)

₹14.22 Crore

Return on Equity (ROE)

26.3%

Market Capitalization

₹325 Crore

Investor interest has been strongly captured by an aggressive corporate restructuring program. The company executed a 1:5 stock split, followed immediately by a massive 2:1 bonus share allotment, completely reshaping its equity architecture. Simultaneously, management moved to entirely discontinue its legacy agricultural commodities processing division (wheat products and pulses). By throwing away lower-margin baggage, the business has positioned itself purely as a high-margin heavy industrial engineering provider.

However, balance sheet risks are rapidly mounting. Trade receivables doubled to ₹28.18 crore during the year, highlighting aggressive billing cycles or delayed collections from heavy industry clients. When structural revenue growth stalls, a sudden build-up of uncollected customer bills indicates that reported profits are living on the balance sheet rather than inside the bank account. This working capital stretch represents a primary friction point for an otherwise highly profitable year.

Section 2 — Introduction

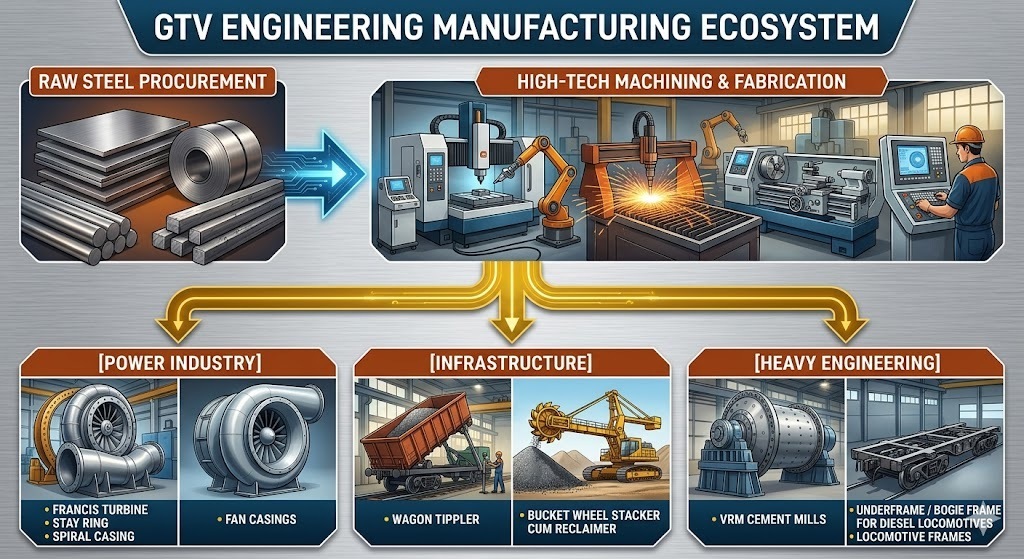

GTV Engineering operates in a niche corner of the capital goods sector, specializing in large-scale machining and high-tech steel fabrication. For over three decades, the company has worked primarily as a high-tier heavy engineering subcontractor. It builds critical custom infrastructure parts for mega-cap infrastructure and equipment conglomerates.

The company has arrived at a critical operational pivot point. After years of running a split business model—processing bulk agricultural commodities on one side while welding heavy turbines on the other—management has finally chosen a side. This strategic clarity comes exactly as the company attempts to break out from its micro-cap shell through an aggressive inorganic asset acquisition program and a series of corporate balance sheet adjustments.

Section 3 — Business Model: WTF Do They Even Do?

GTV Engineering is essentially a specialized industrial tailor. They do not manufacture off-the-shelf catalog products. Instead, they take complex blueprinted designs from infrastructure giants and turn raw steel blocks into massive, highly engineered mechanical systems.

Their workshops produce structural components including Francis hydro-turbines, mammoth fan casings for power plants, locomotive underframes, and massive vertical roller mills used in cement factories. Over 89% of operational revenues are derived from this heavy engineering segment, following the tactical phase-out of their legacy flour and pulse-milling business lines.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

Quarterly Performance Trend

Metric

Q4 FY26

YoY

QoQ

Revenue

₹31.96

42.7%

11.9%

EBITDA / Operating Profit

₹3.95

255.9%

-49.9%

PAT

₹3.11

33.5%

-43.6%

EPS (₹)

₹0.66

32.0%

-44.1%

Financial Commentary

The absolute numbers show a company running at two entirely different speeds. While the final quarter of the year generated solid top-line revenue of ₹31.96 crore (up 42.7% year-on-year), sequential operational