Royal Arc Electrodes H2 FY26: Spending IPO Millions While the Core Engine Slows Down

Section 1 — At a Glance

Royal Arc Electrodes Limited’s full-year performance highlights a distinct shift in operational realities. For the financial year ended March 31, 2026, the company recorded total revenues from operations of ₹116.06 crore, reflecting a top-line expansion of 14% compared to ₹101.77 crore in the previous fiscal year. However, this volume-led push came at a steep cost to profitability. Total operating expenses jumped disproportionately to ₹104.39 crore , driven by rising raw material consumption. Consequently, standalone net profit for the full year stood at ₹10.05 crore, a minor 11.5% tick up from ₹9.01 crore in FY25.

While a surface-level look shows growth, a deeper inspection reveals structural friction. Operating profit margins contracted from 15% to 13% year-on-year , driven by elevated inventory adjustments and manufacturing input costs. Investor attention is currently split between the completion of their ₹21.60 crore IPO fund deployment and a sudden surge in debtor days, which climbed from 75 to 81 days. Earnings are expanding, but the quality of that cash generation is degrading. When working capital expands faster than the operating matrix, reported profits become an accounting mirage rather than spendable liquidity. Investors are left assessing whether the company’s recent capacity expansions will yield genuine scale or simply build an underutilized, capital-heavy infrastructure footprint.

Section 2 — Introduction

Royal Arc Electrodes entered the public markets with its listing on the NSE Emerge platform on February 24, 2025, raising ₹36.00 crore in gross proceeds. The industrial microcap, established in 1996, operates out of its primary manufacturing asset in Valsad, Gujarat. It occupies a niche corner of the capital goods sector, supplying fundamental consumables to heavily industrialized segments like shipbuilding, refineries, and infrastructure.

This review is triggered by the release of the audited financial results for the half-year and full-year ending March 31, 2026. This period represents the company’s first full financial year under public scrutiny, testing management’s ability to allocate capital without the typical governance lapses seen in small-cap listings. With a fresh corporate infrastructure, including an entirely re-shuffled auditing and compliance hierarchy enacted during the latest board meeting, the company is transitioning from a closely-held family shop to an institutionally monitored operation.

Section 3 — Business Model: WTF Do They Even Do?

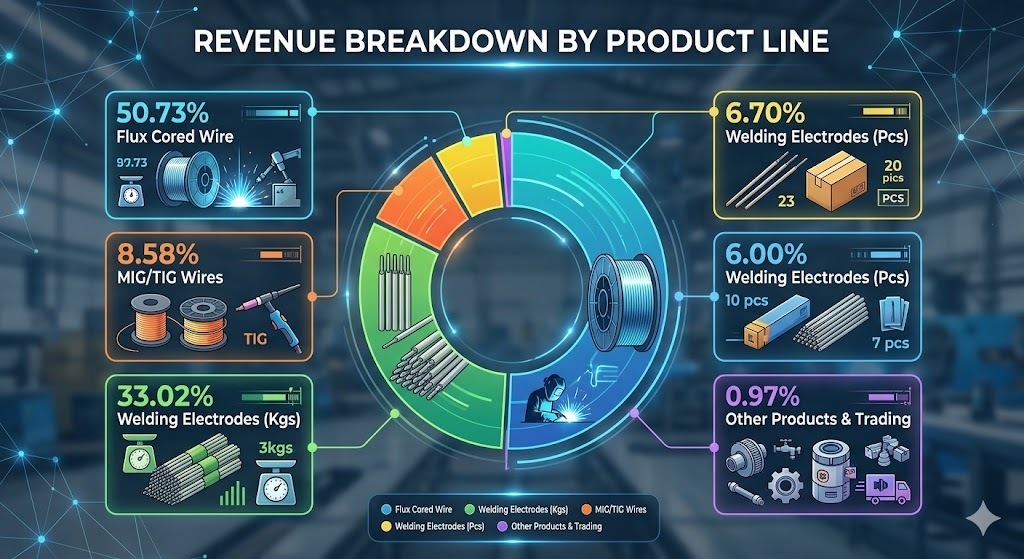

Royal Arc Electrodes is fundamentally a blacksmith to the industrial complex. They manufacture materials that melt to join two pieces of metal together. Their product catalog is led by flux-cored wires, which generate 50.73% of their top line, followed closely by traditional welding electrodes contributing 33.02%. The remaining revenue is sprinkled across MIG/TIG specialty wires and the trading of industrial abrasive wheels and sawing fluxes.

The underlying business relies on constant economic activity. Shipyards, refineries, and pre-engineered buildings cannot construct assets without eating through thousands of metric tons of these welding products daily. It is a high-volume, low-differentiation game where 90.46% of revenue is derived from internal manufacturing operations. The company is intensely localized, keeping 85.56% of its sales within domestic boundaries while maintaining a small 14.44% export footprint.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

Half-Yearly Performance Table

Metric

Latest Half (Mar 2026)

YoY (Same Half FY25)

Previous Half (Sep 2025)

Revenue

₹63.22

₹56.03

₹52.84

EBITDA / Operating Profit

₹6.58

₹8.01

₹5.10

PAT

₹5.73

₹5.87

₹4.31

EPS (₹)

₹5.16

₹6.12

₹3.89

(Note: Data compiled directly from standalone financial statements. EBITDA calculated as PBT + Interest + Depreciation ).

The sequential half-yearly numbers show a company running faster just to remain in the same spot. While revenues increased to ₹63.22 crore in the half-year ending March 31, 2026 , operating profits fell from ₹8.01 crore in the corresponding previous year period to ₹6.58 crore. This severe margin contraction shows that raw materials are eating management alive before their products even reach a distributor’s shelf.

A business cannot survive on revenue optics alone; if