Bharat Petroleum Corporation Ltd (BPCL) Mar 2026: The ₹1,70,000 Crore Project Aspire Dilemma

Section 1 — At a Glance

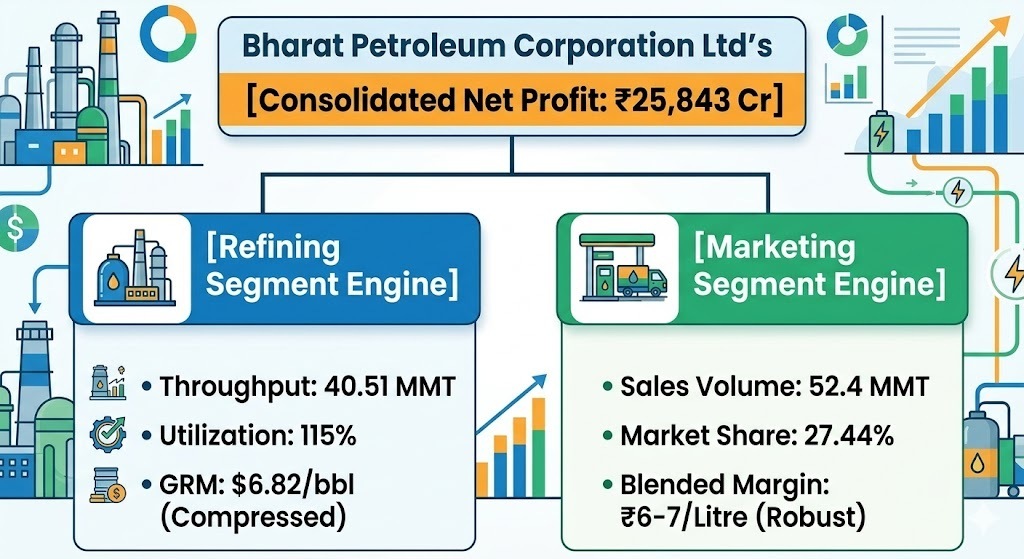

A massive ₹25,843 crore consolidated net profit sits at the apex of Bharat Petroleum Corporation Limited’s (BPCL) March 2026 full-year financial closure, marking a strong headline recovery in structural earning power. Yet, a closer examination reveals a starkly divergent operating reality. While consolidated revenue from operations remained steady at ₹4,55,228 crore, the internal mechanics of the enterprise have experienced a massive structural shift.

The primary engine of recent profitability has migrated entirely away from core refining operations and into downstream retail marketing distribution. Easing crude input values combined with unyielding retail pump prices created an exceptional margin architecture for motor spirit and high-speed diesel, successfully offsetting a global collapse in refining margins. Refinery crude throughput reached 40.51 MMT with an intensive 115% capacity utilization. However, the reported Gross Refining Margin (GRM) contracted sharply from its historical highs to settle at $6.82 per barrel.

Investor attention remains intensely focused on the multi-year implementation of “Project Aspire”—a massive ₹1,70,000 crore capital expenditure program aimed at expanding petrochemical footprints at Bina and Kochi. While this initiative promises long-term structural diversification into high-value polymers, it introduces significant balance sheet transition risks.

Short-term operational metrics are further complicated by an intentional, geopolitically driven accumulation of excess crude inventories, raising carrying costs and constraining near-term refinery returns. Corporate returns fluctuate on variables completely outside management control, such as international crude cycles and regulatory pricing structures. True capital efficiency is revealed only when an enterprise maintains high returns across volatile commodity cycles, rather than during temporary macro tailwinds. The critical variable moving forward is whether BPCL can execute this unprecedented asset expansion without diluting its historically resilient return profile.

Section 2 — Introduction

Bharat Petroleum Corporation Limited occupies an indispensable, sovereign-backed positioning at the absolute core of India’s downstream energy landscape. Holding a dominant 14% slice of domestic refining infrastructure and commanding a vast downstream distribution network, the Maharatna public sector undertaking operates as a primary execution arm for national energy security.

This deep analytical review comes at a vital corporate juncture. The Government of India formally discontinued its strategic disinvestment and privatization plans, cementing BPCL’s status as a state-anchored entity with 52.98% sovereign ownership. Simultaneously, the company has completed major internal corporate restructuring, fully absorbing Bharat Oman Refineries Limited (BORL) and Bharat Gas Resources Limited (BGRL) to consolidate its manufacturing footprint.

With a newly appointed executive leadership team executing a rapid pivot toward petrochemical integration, green hydrogen, and city gas networks, BPCL is actively transitioning from a traditional fossil-fuel refiner into a diversified energy conglomerate. This analysis dissects the structural profitability of its current marketing cash cow against the capital-intensive risks of its future production bets.

Section 3 — Business Model: WTF Do They Even Do?

At its core, BPCL functions as a high-velocity processing and distribution machine that converts volatile barrels of imported crude oil into everyday retail consumer invoices. The operational architecture is divided into two highly codependent segments: refining raw crude and marketing finished petroleum products.

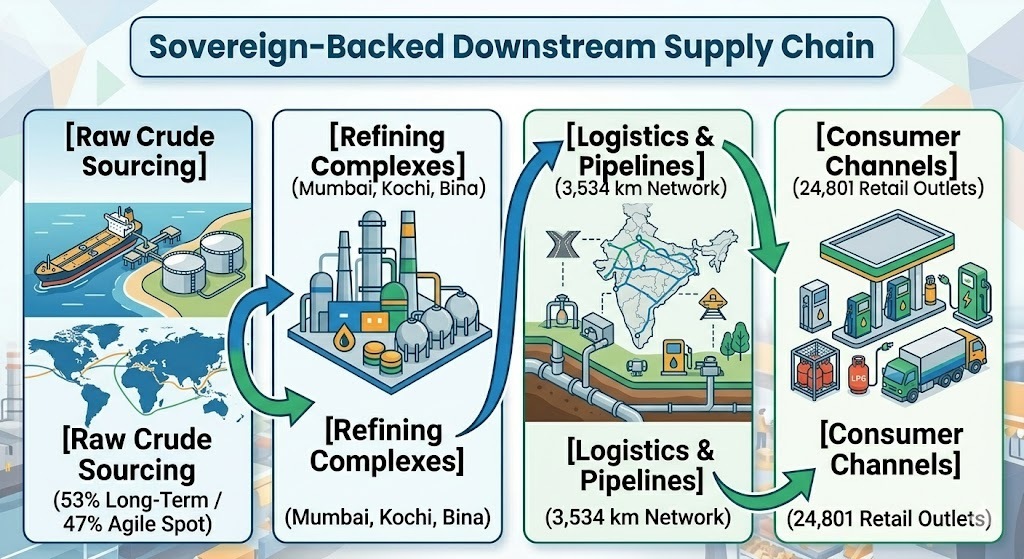

The company owns and operates three primary refining complexes located across Mumbai, Kochi, and Bina, controlling an aggregate processing capacity of 35.3 MMTPA. Once refined, the industrial output is fed into a massive, highly proprietary logistical apparatus. This includes 3,534 kilometers of specialized cross-country pipelines with a design transport capacity of 29 MMTPA, terminating across 80 retail depots and 57 highly automated LPG bottling plants.

The true value of this network lies in its extensive retail distribution access. BPCL operates 24,801 retail fuel outlets across India, capturing a dominant 27.44% domestic market share among public sector peers. This infrastructure achieves an industry-leading average throughput of 145 kilolitres per month per station, driven by key highway locations.

Beyond retail petrol and diesel, which comprise the vast majority of its volume, the business model captures highly defended market shares across specialized sub-segments:

Liquefied Petroleum Gas (LPG): Serving a massive base of 9 crore domestic customers via 6,273 specialized distributors (27% market share).

Aviation Turbine Fuel (ATF): Fuelling commercial aviation networks via 81 specialized airport service stations (24.8% market share).

Industrial & Commercial (I&C): Supplying over 8,000 industrial clients with heavy fuel oils and customized solvents.

Lubricants: Distributing over 400 specialized grades via its proprietary “MAK Lubricants” brand.

Upstream Exploration (BPRL): Holding working interests across 15 global extraction blocks, acting as a long-term supply hedge.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Latest Quarter (Mar 2026)

YoY (% Change)

QoQ (% Change)

Revenue

1,18,701

6.72%

-0.28%

EBITDA / Operating Profit

9,634

7.58%

-17.57%

PAT

5,625

17.43%

-21.74%

EPS (₹)

12.96

17.39%

-21.79%

The financial trajectory across the trailing quarters highlights a distinct compression in sequential operating momentum. While revenue expanded 6.72% on a year-on-year basis to hit ₹1,18,701 crore for the quarter, operating profit fell 17.57% sequentially against the December 2025 period. This compression stems from a rapid narrowing of refining economics, as international product cracks cooled while domestic retail fuel pricing remained entirely static.

Accounting profits frequently diverge from underlying economic performance when external price controls distort the direct pass-through of raw material inputs. A sharp seasonal increase in tax expense to 28% further softened the final quarterly PAT to ₹5,625 crore.

What is Management Promising in the Coming Quarters?

During the audited earnings conference call, management laid out an aggressive multi-year deployment path, while clarifying several key operational metrics:

“Our peak capital expenditure cycle is now firmly scheduled, with FY26 outlays finalized at ₹16,000 crore, rising to a range of ₹22,000–25,000 crore in FY27, before reaching a maximum intensity of ₹34,000 crore in FY28 and ₹35,000 crore in FY29.”

Addressing the compression in near-term refinery economics, the CEO noted that the underperformance was heavily driven by a strategic decision to build up crude inventories to 2.9–3.0 MMT—roughly 25% above normalized run-rates—to assure supply stability amidst severe geopolitical uncertainties. This temporary accumulation incurred substantial carrying costs that weighed heavily on the quarter’s reported GRM.

Regarding downstream pricing risks, management stated there are “absolutely no discussions” regarding a reduction in retail fuel pump prices, despite international oil trading below $70 per barrel. Furthermore, the company is actively awaiting the structural execution