Fine Organic Industries Ltd Mar 2026 : Profitability Flattening Out at 17.6% Margin Amidst 83-Crore Cross-Border Bet

Section 1 — At a Glance

The era of explosive pricing tailwinds has officially wound down for the niche oleochemical kingpin. Fine Organic Industries Ltd closed the financial year ending March 31, 2026, with a consolidated revenue from operations of ₹2,365.80 crore, representing a modest top-line growth of 4.26% over the ₹2,269.15 crore recorded in the previous fiscal year. Consolidated net profit crawled slightly ahead, printing at ₹417.07 crore against ₹410.50 crore last year. This thin margin expansion marks a dramatic transition from the hyper-abnormal post-pandemic cycles, highlighting that structural run-rate normalization has firmly set in. Investors are closely eyeing the board’s recent greenlit proposal to acquire up to an 80% stake in Malaysia’s Oleofine Organics Sdn. Bhd. for approximately ₹83 crore, a deliberate footprint expansion right into the heart of the global palm oil raw material corridor.

However, beneath the steady headline profit, localized frictions are emerging. Operating profit margins (OPM) contracted to 20.29% for the full year, pressured by a sequential spike in freight rates due to the ongoing West Asia gridlock and escalating domestic raw material costs. Furthermore, the sudden structural shift in domestic labor regulations forced an incremental actuarial provision of ₹7.11 crore towards gratuity during the fiscal cycle, impacting near-term personnel costs. When a business runs a highly efficient capital engine, systemic regulatory shifts and shipping logjams act as sand in the gears rather than structural blocks. Investors must now weigh a bulletproof, net-debt-negative balance sheet carrying ₹1,448.83 crore in cash and bank balances against execution timelines for massive parallel capital expenditures stretching across Maharashtra, South Carolina, and Malaysia.

Section 2 — Introduction

Fine Organic Industries Ltd has evolved from its 1970 partnership roots into India’s undisputed heavyweight champion of oleochemical-based niche additives. Operating out of its corporate base in Maharashtra, the enterprise serves as a crucial intermediary link across global supply chains by transforming basic vegetable oils into high-performance, green chemistry alternatives.

This comprehensive review comes at a critical juncture. The stock is currently consolidating at a snapshot price of ₹4,604.10, assigning it a market capitalization of ₹14,116.16 crore. The market is no longer treating Fine Organic as a speculative post-pandemic chemical play, but rather as a mature specialty player whose earnings must back its premium valuation. With multi-continent expansion blueprints moving from spreadsheets to physical ground-breaking, this analysis deconstructs the operational reality behind the cash piles.

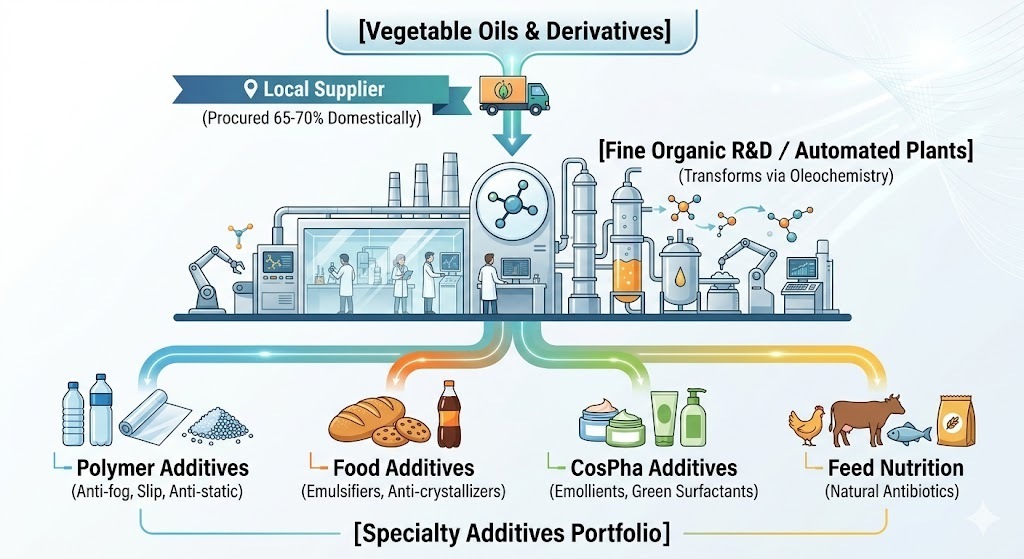

Section 3 — Business Model: WTF Do They Even Do?

If you enjoy eating branded biscuits that do not stick to your teeth, using packaging film that stays transparent under condensation, or applying skin creams that do not separate into oily layers overnight, you are consumer to Fine Organic’s chemistry. The company operates a highly specialized B2B model manufacturing over 600 proprietary green additives.

They process vegetable oils—primarily soy, palm, sunflower, and rapeseed—into performance-altering chemical molecules. Their product suite splits into polymer additives, food emulsifiers, cosmetic base ingredients, and animal feed stabilizers. Rather than being a primary component, they act as a “pinch of salt,” representing