At a Glance – The Intoxicating Mix of Growth and Risk

Sula Vineyards is currently at a critical intersection where brand dominance meets brutal operational reality. On one hand, the company is gaining significant investor attention by crossing the ₹100 crore milestone in Wine Tourism revenue for the first time in FY26. On the other hand, the core wine business is gasping for air as profitability metrics face a “sharp decline,” prompting top-tier credit rating agencies to slash their outlook to Negative.

The numbers tell a story of two different companies. While the hospitality segment is booming with record footfalls of 360,000+ visitors, the overall PAT has plummeted by 63% YoY to just ₹25.7 Cr for the full year. Investors are watching a massive tug-of-war: Sula is doubling down on its “premiumization” strategy with brands like The Source and RASA, yet it is being haunted by high working capital intensity and a massive ₹85 crore WIPS receivable stuck with the government.

The red flags are waving high. Inventory days have ballooned, and the operating margins that once sat comfortably at 31% have now evaporated to roughly 17.4% for FY26. Management is making a bold bet by acquiring Chandon’s 19-acre estate to fix their supply and tourism bottlenecks, but with a Debt-to-EBITDA ratio creeping toward 3x, the margin for error is razor-thin. Is this a temporary hangover or a structural shift in the Indian AlcoBev landscape?

Introduction

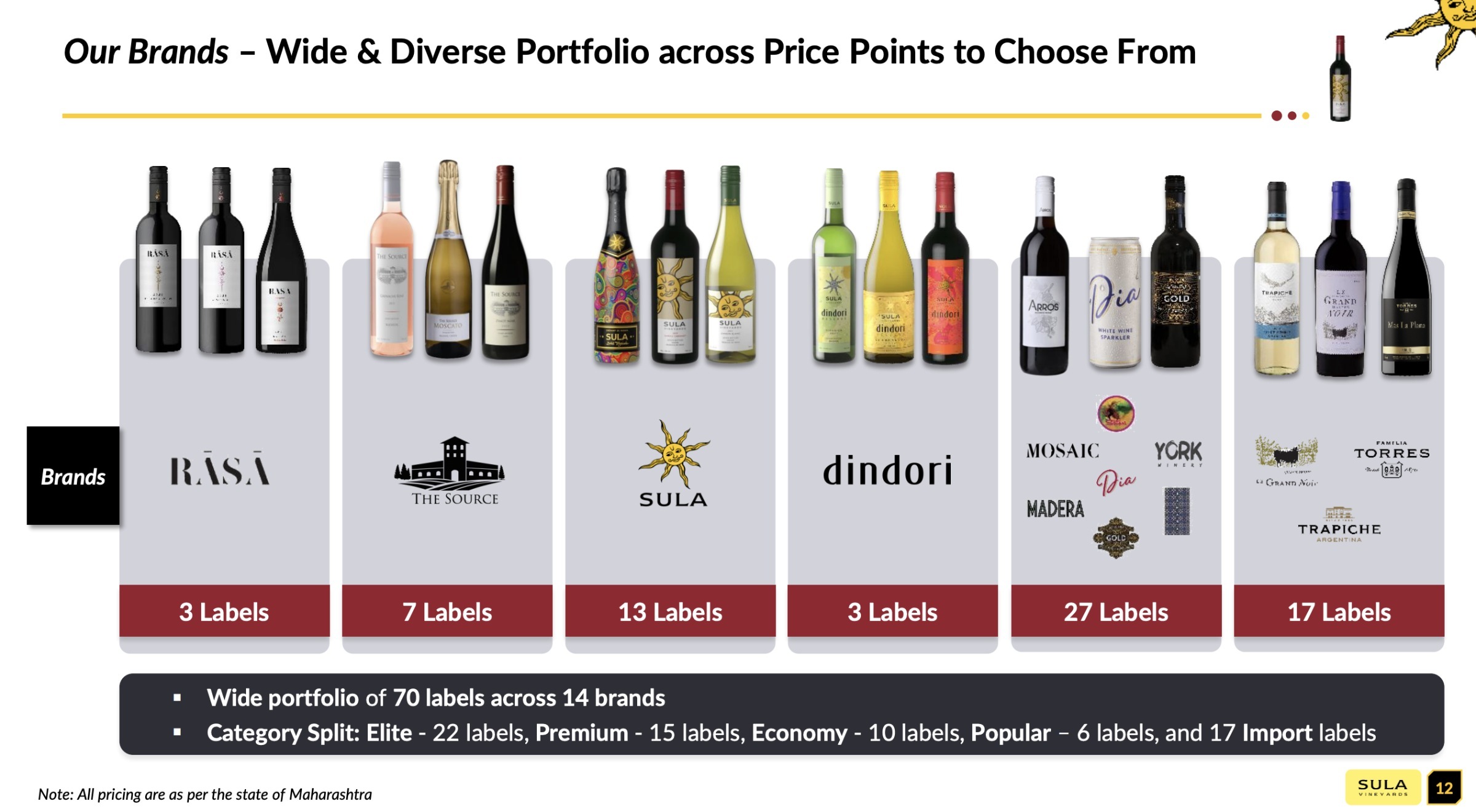

Sula Vineyards isn’t just a wine company; it’s a category creator that currently controls over 50% of the Indian wine market. Founded in 2003, it has scaled from a niche Nashik experiment into a powerhouse with a winery capacity of 19.2 million liters, placing it among the top five wineries in Asia.

However, the recent financial year has been a sobering experience. The company reported a total revenue of ₹596.2 Cr for FY26, a slight dip from the previous year. While the “Elite & Premium” labels now make up 79% of their portfolio mix, the “Economy & Popular” segments are being intentionally sacrificed due to unsustainable discounting by competitors.

The narrative for FY26 was dominated by two themes: De-stocking and Diversification. A massive tactical de-stocking in Karnataka wiped out ₹21 crores from the top line in a single quarter, intended to reset channel health. Meanwhile, the company’s shift toward becoming a hospitality major is accelerating, with room capacity jumping 50% to 154 keys.

For the general public, Sula represents the aspirational lifestyle of urban India. For the auditor, however, it represents a business with high debtor days (156 days) and a heavy reliance on state-specific excise policies that can change overnight.

Business Model – WTF Do They Even Do?

Sula operates a vertically integrated model that handles everything from the “soil to the sip.” They don’t just sell fermented grape juice; they sell an “experience” that masks the volatility of agriculture.

1. The Wine Factory

They produce 69 labels. They range from the “Elite” (₹1,000 – ₹2,100) to the “Popular” (under ₹400). They’ve realized that selling cheap wine is a race to the bottom, so they are pivoting hard toward the Elite & Premium segment, which now contributes roughly 76% to 79% of their own-brand revenue.

2. The Farmer Network

Sula doesn’t own most of the land. They have 2,800+ acres of contracted vineyards. They essentially act as the “Big Brother” to 2,800+ farmers, providing technical know-how and long-term contracts (up to 12 years) to ensure they get the best grapes without the headache of land ownership.

3. The “Disneyland” of Alcohol

This is where the real money is.